Extraordinary Meeting of Council

Open Agenda

|

Meeting Date:

|

Thursday 11 June 2020

|

|

Time:

|

10.00am

|

|

Venue:

|

Large Exhibition Hall

Napier War Memorial Centre

Marine Parade

Napier

|

|

Council Members

|

Mayor Wise, Deputy Mayor Brosnan, Councillors Boag,

Browne, Chrystal, Crown, Mawson, McGrath, Price, Simpson, Tapine, Taylor,

Wright

|

|

Officer Responsible

|

Interim Chief Executive

|

|

Administrator

|

Governance Team

|

|

|

Next Ordinary Council Meeting

Thursday 23 July 2020

|

Extraordinary

Meeting of Council - 11 June 2020 - Open Agenda

ORDER OF BUSINESS

Apologies

Nil

Conflicts of interest

Public forum

Nil

Announcements by the Mayor including notification of minor

matters not on the agenda

Note: re minor matters only - refer LGOIMA s46A(7A) and

Standing Orders s9.13

A meeting may discuss

an item that is not on the agenda only if it is a minor matter relating to the

general business of the meeting and the Chairperson explains at the beginning

of the public part of the meeting that the item will be discussed. However, the

meeting may not make a resolution, decision or recommendation about the item,

except to refer it to a subsequent meeting for further discussion.

Announcements by

the management

Agenda items

1 Consultation

- Rates Postponement Policy.......................................... 3

2 Consultation

- Rates Remisson Policy............................................... 14

3 Consultation

Document and Draft Annual Plan 2020/21.................... 24

4 Statement

of Proposal to join the Local Government Funding Agency............................................................................................ 223

Public excluded ............................................................................... 242

Extraordinary

Meeting of Council - 11 June 2020

- Open Agenda Item

1

Agenda Items

1. Consultation

- Rates Postponement Policy

|

Type of Report:

|

Legal and Operational

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

935149

|

|

Reporting Officer/s & Unit:

|

Garry Hrustinsky, Investment and Funding Manager

|

1.1 Purpose of Report

To review and update the policy to include a clearer

definition around financial hardship. To introduce rates postponement resulting

from Significant Extraordinary Circumstances. Some minor clarification of

Criteria wording.

|

Officer’s

Recommendation

That

Council:

a. Approve

the

proposed amendments to the Rates Postponement Policy to include Significant

Extraordinary Circumstances.

b. Approve

wording change from “Elderly” to “Older Persons”

c. Approve

other minor changes detailed in this report

d. Approval

to go to consultation on the revised Rates Postponement Policy to run

parallel but separately to the Annual Plan 20/21.

e. Approve

the consultation plan for the Rates Postponement Policy

|

1.2 Background

Summary

The COVID-19 pandemic and a subsequent response

planning has highlighted the need to better define rates postponements for Significant

Extraordinary Circumstances.

1.3 Issues

In its current form, the Rates

Postponement Policy is structured to review postponements on a very small

(individual) scale. Significant time (including that of Prosperous Napier

Committee) and resources are required to process each application. The proposed

amendment allows the Council to apply broad postponements in situations where Significant Extraordinary

Circumstances are identified.

The proposed amendment is as

follows:

Postponement for Significant Extraordinary Circumstances

Objective

To provide a rates

postponement to ratepayers experiencing financial hardship directly resulting

from Significant Extraordinary Circumstances that affects their ability to pay

rates.

For the purpose of this policy

the following definitions will apply:

· Significant

Extraordinary Circumstances: as defined by Council resolution.

Significant Extraordinary Circumstances may be natural or economic in nature,

and will identify the type and location of properties affected.

· Financial

Hardship: for the purpose of this provision is defined as the inability

of a person, after seeking recourse from Government benefits or applicable

relief packages, to reasonably meet the cost of goods, services and financial

obligations that are considered necessary according to New Zealand standards.

In the case of a ratepayer who is not a natural person, it is the inability,

after seeking recourse from Government benefits or applicable relief packages,

to reasonably meet the cost of goods, services and financial obligations that

are considered essential to the functioning of that entity according to New

Zealand standards.

· Small

Business: a business operated by a small business person, small

partnership or close company as defined in section YA 1 of the Income Tax Act

2007.

Conditions and Criteria

This part of the policy will

only apply to Rating Units used for residential purposes or by Small

Businesses.

Once Significant Extraordinary

Circumstances have been identified by Council, the criteria and application

process (including an application form, if applicable), will be made available.

Council may set a timeframe for the event. Council may review the criteria

and/or timeframe of Significant Extraordinary Circumstances through subsequent

resolutions.

Council resolution will

include:

a. that

the resolution applies under the Rates Postponement Policy; and

b. the

Significant Extraordinary Circumstances triggering the policy (e.g. including,

but not limited to, flood, pandemic, earthquake); and

c. how

the Significant Extraordinary Circumstances are expected to impact the community

(e.g. hardship); and

d. the

types or location of properties effected by the Significant Extraordinary

Circumstances; and

e. timeframe

for postponement in relation to the Significant Extraordinary Circumstances.

No application for

postponement can be made under this policy unless Significant Extraordinary

Circumstances have been identified by Council.

Any requests for rates

postponement for Rating Units with a land value greater than $1.5m will be

decided upon at the discretion of Council and requests for rate postponement

for Rating Units with a land value less than $1.5m will be delegated to Council

officers.

The ratepayer must

demonstrate, to the Council’s satisfaction that paying the rates would

result in Financial Hardship.

The applicant must demonstrate

to Council’s satisfaction that the ratepayer has taken all necessary

steps to claim any central government benefits or allowances the

ratepayer is properly entitled to receive that would assist the ratepayer to

meet their financial commitments. Evidence such as official correspondence must

be provided with the application.

Council will consider

applications where the same ratepayer is liable for rates for multiple Rating

Units. In such instances, Council will look at the collective impact to the ratepayer.

Only the person/s entered as

the ratepayer (in the case of a close company every director must sign the

application form), or their authorised agent, may make an application for rates

postponement for Significant Extraordinary Circumstances that resulted in

Financial Hardship. However, where the ratepayer is not the owner of the Rating

Unit, the owner must also provide written approval of the application.

The ratepayer must be the

current ratepayer for the Rating Unit at the time Significant Extraordinary

Circumstances are identified by Council.

Where the Council decides to

postpone rates the ratepayer must make acceptable arrangements for payment of

rates, for example by setting up a system for regular payments. Such

arrangements will be based on the circumstances of each case.

Council may charge a fee on

postponed rates for the period between the due date and the date they are paid.

This fee is designed to cover Council’s administrative and financial

costs. The fees will be set as part of the Council resolution identifying

Significant Extraordinary Circumstances.

Postponed rates will remain

postponed until the earlier of:

a. The

ratepayer/s ceases to be the owner or occupier of the Rating Unit; or

b. A

date specified by Council in the Council resolution identifying Significant

Extraordinary Circumstances.

Further minor amendments include:

· Postponement

for the elderly has been changed to Postponement for Older Persons with policy

text amended to reflect the wording change.

· Removal of

the 5 year ownership rule for applications under Postponement for Older

Persons.

· Removal of

the provision “At the end of five years any postponed rates will be

written off if the rating unit has not been subdivided.” From

Postponement for Farmland. This will encourage development in areas identified

for growth.

· Delegation

to approve rates postponements for Postponement for Farmland and Postponement

for Older Persons extended to Chief Financial Officer and Investment &

Funding Manager.

· Additional

legislative and Council document references have been included in the policy.

· Applications

under Postponement for Special Circumstances can now be made by the

“…ratepayer or their authorised agent…” instead of

solely by the “applicant”.

1.4 Significance and Engagement

There has been no external

consultation on the proposed changes.

The proposed amendments are

similar to those already in place, or proposed, for other Councils.

Significance of the proposed

amendments are high as they could potentially impact proportion of residents or

ratepayers.

If approved, public consultation

will be required and undertaken as a separate consultation in parallel with the

Annual Plan 20/21.

1.5 Implications

Financial

N/A

Social & Policy

The proposed amendment will allow

Napier City Council to be more responsive by events that have a material

negative impact on the wider city.

Risk

Taking the Postponement Policy in

its current form, the Council is not well placed to provide timely

postponement, and may be overwhelmed due to administrative burden should

another extraordinary or emergency event occur.

1.6 Options

The options available to Council

are as follows:

a. Adopt all of the proposed

changes.

b. Adopt selected proposed changes.

c. Adopt none of the proposed

changes.

1.7 Development of Preferred Option

The proposed changes to the Rates

Postponement Policy allow Council to be more responsive in times of Significant

Extraordinary Circumstances impacting the community.

1.8 Attachments

a Rates

Postponement Policy ⇩

b Consultation

Plan - Rates Postponement Policy ⇩

|

Extraordinary Meeting of

Council - 11 June 2020 - Attachments

|

Item 1

Attachments a

|

|

Rates Postponement Policy

|

|

Approved By

|

Pending Approval by Council

|

|

Department

|

Finance

|

|

Original Approval Date

|

29 June 2018

|

Review Approval Date

|

Pending

|

|

Next Review Deadline

|

June 2023

|

Document ID

|

346038

|

|

Relevant Legislation

|

Local Government (Rating) Act 2002

Local Government Act 2002

Income Tax Act 2007

|

|

NCC Documents Referenced

|

Published in the Long Term Plan

2018-2028 which was reviewed between March/April 2018 and adopted on 29-06-18

Reviewed and amended in response to

COVID-19

Rating – Delegations under

Local Government (Rating) Act 2002

|

Purpose

To enable Council to postpone the requirement to pay all or part of the

rates on a Rating Unit under Section 87 of the Local Government (Rating) Act

2002 where a rates postponement policy has been adopted and the conditions and

criteria in the policy are met.

Policy

Postponement

for Farmland

Objective

To support the District Plan by encouraging owners of farmland around

urban areas to refrain from subdividing their land for residential purposes.

Conditions

and Criteria

To initially qualify, or continue qualifying, for postponement of rates

under this policy the Rating Unit must be classified, or continue to be

classified, as farmland for differential purposes (ratepayers wishing to

ascertain their classification are welcome to inspect the Council’s

rating information database at the Council office).

Rates postponement will continue to apply on those properties that were

subject at 30 June 2003 to postponement under Section 22 of the Rating

Valuations Act 1998. Other rural ratepayers wishing to take advantage of this

part of the policy must make application in writing, addressed to the Director

Corporate Services. The application for postponement must be made to the

Council prior to the commencement of the rating year. Applications received

during a rating year will be applicable from the commencement of the following

rating year. Applications will not be backdated.

For properties currently subject to rates postponement and for new

applications approved, Council will postpone the difference between rates

payable on the equivalent Rates Postponement Value advised by its Valuation

Service Provider and rates payable on the Rateable Value of the land each year.

The Council may charge an annual fee on postponed rates for the period

between the due date and the date they are paid. This fee is designed to cover

the Council’s administrative and financial costs and may vary from year

to year. The amount of the fee is included in Council’s Schedule of Fees

and Charges.

If the Rating Unit is subdivided then postponed rates and any

accumulated fees will be payable. The ratepayer will be required to sign an

agreement acknowledging this. Postponed rates will be registered as a charge

against the land (i.e. in the event that the property is sold the Council has

first call against any of the proceeds of that sale). Again, the ratepayer will

be required to sign an agreement acknowledging this.

Authority to approve applications will be delegated by Council to the

Director of Corporate Services, Chief Financial Officer and Investment and

Funding Manager.

Postponement

for Older Persons

Objective

The objective of this part of the policy is to assist ratepayers who

are Older Persons with a fixed level of income to meet rates particularly, but

not exclusively, resulting from increasing levels of rates.

Definition

Older Persons are those who are old enough to qualify to receive NZ

Superannuation.

For the purpose of this provision, Financial Hardship is defined as the

inability of a person, to reasonably meet the cost of goods, services and

financial obligations that are considered necessary according to New Zealand

standards.

Conditions

and Criteria

Postponement will only apply to Older Persons on a fixed income.

Only Rating Units used solely for residential purposes will be eligible

for consideration for rates postponement under this policy.

Only the person entered as the ratepayer, or their authorised agent,

may make an application for rates postponement for Financial Hardship. The

ratepayer must be the occupant and current owner of the Rating Unit which is

the subject of the application. The person entered on the Council’s

rating information database as the ‘ratepayer’ must not own any

other Rating Units or investment properties (whether in the district or

elsewhere).

The ratepayer (or authorised agent) must make an application to Council

on the prescribed form (copies can be obtained from the Council Office).

The Council will consider, on a case by case basis, all applications

received that meet the criteria outlined under this section. The following

factors will be considered – age, income source and level, annual rates

payable, period of postponement, equity in the property owned, and the amount

of rates postponed.

Authority to approve applications will be delegated by Council to the

Director of Corporate Services, Chief Financial Officer and Investment and

Funding Manager.

Applicants seeking rates postponement will be encouraged to seek

independent advice before formally accepting any offer for postponement made by

the Council.

As a general rule postponement will not apply to the first $500 per

annum of the rate account after any rates rebate has been deducted.

Where the Council decides to postpone rates the ratepayer must first

make acceptable arrangements (e.g. by setting up a system to meet agreed

minimum regular payments) for payments required under the terms of the

postponement approval for the current rating year, and future payment years.

Postponement will only apply on properties on which houses have been

insured. Annual proof may be required that insurance has been maintained.

Where rates postponement is approved for a property with an outstanding

mortgage, the mortgagee will be advised by Council that rates postponement has

been granted by the Council.

Any postponed rates will be postponed until:

The death of the ratepayer(s); or

· Until the

ratepayer(s) ceases to be either the owner or occupier of the Rating Unit; or

· Until a date

specified by the Council.

The Council will charge an annual postponement fee. The annual

postponement fee will cover Council’s administrative costs including

finance costs. The finance cost will be charged at the average return on

investments rate for Council for that year.

All postponement fees payable (including finance costs) will be added

to the amount of postponed rates annually and be paid at the time postponed

rates are paid.

The policy will apply from the beginning of the rating year in which

the application is made although the Council may consider backdating past the

rating year in which the application is made depending on the circumstances.

The postponed rates, inclusive of any accumulated postponement fees, or

any part thereof may be paid at any time. The applicant may elect to postpone

the payment of a lesser sum than that which they would be entitled to have

postponed pursuant to this policy.

Postponed rates will be registered as a statutory land charge on the

Rating Unit title. This means that the Council will have first call on the

proceeds of any revenue from the sale or lease of the Rating Unit. In addition

to the annual fee and interest, Council will charge any other costs or one-off

fees incurred in relation to registration of the postponement as part of the

postponement.

This policy will not affect any rates postponement provisions approved

prior to 1 July 2009, which will continue to apply in accordance with the

conditions related to each case.

This policy does not apply to non-Older Person ratepayers experiencing

financial hardship.

Council will assist in the referral of any other ratepayer on a fixed

income facing long term financial hardship to the appropriate agency.

Postponement

for Significant Extraordinary Circumstances

Objective

To provide a rates postponement to ratepayers experiencing financial

hardship directly resulting from Significant Extraordinary Circumstances that

affects their ability to pay rates.

For the purpose of this policy the following definitions will apply:

· Significant

Extraordinary Circumstances: as defined by Council resolution. Significant

Extraordinary Circumstances may be natural or economic in nature, and will

identify the type and location of properties affected.

· Financial

Hardship: for the purpose of this provision is defined as the inability of

a person, after seeking recourse from Government benefits or applicable relief

packages, to reasonably meet the cost of goods, services and financial

obligations that are considered necessary according to New Zealand standards.

In the case of a ratepayer who is not a natural person, it is the inability,

after seeking recourse from Government benefits or applicable relief packages,

to reasonably meet the cost of goods, services and financial obligations that

are considered essential to the functioning of that entity according to New

Zealand standards.

· Small

Business: a business operated by a small business person, small partnership

or close company as defined in section YA 1 of the Income Tax Act 2007.

Conditions

and Criteria

This part of the policy will only apply to Rating Units used for

residential purposes or by Small Businesses.

Once Significant Extraordinary Circumstances have been identified by

Council, the criteria and application process (including an application form,

if applicable), will be made available. Council may set a timeframe for the

event. Council may review the criteria and/or timeframe of Significant

Extraordinary Circumstances through subsequent resolutions.

Council resolution will include:

a. that

the resolution applies under the Rates Postponement Policy; and

b. the

Significant Extraordinary Circumstances triggering the policy (e.g. including,

but not limited to, flood, pandemic, earthquake); and

c. how

the Significant Extraordinary Circumstances are expected to impact the

community (e.g. hardship); and

d. the

types or location of properties effected by the Significant Extraordinary

Circumstances; and

e. timeframe

for postponement in relation to the Significant Extraordinary Circumstances.

No application for postponement can be made under this policy unless

Significant Extraordinary Circumstances have been identified by Council.

Any requests for rates postponement for Rating Units with a land value

greater than $1.5m will be decided upon at the discretion of Council and

requests for rate postponement for Rating Units with a land value less than

$1.5m will be delegated to Council officers.

The ratepayer must demonstrate, to the Council’s satisfaction

that paying the rates would result in Financial Hardship.

The applicant must demonstrate to Council’s satisfaction that the

ratepayer has taken all necessary steps to claim any central government

benefits or allowances the ratepayer is properly entitled to receive that

would assist the ratepayer to meet their financial commitments. Evidence such

as official correspondence must be provided with the application.

Council will consider applications where the same ratepayer is liable

for rates for multiple Rating Units. In such instances, Council will look at

the collective impact to the ratepayer.

Only the person/s entered as the ratepayer (in the case of a close

company every director must sign the application form), or their authorised

agent, may make an application for rates postponement for Significant

Extraordinary Circumstances that resulted in Financial Hardship. However, where

the ratepayer is not the owner of the Rating Unit, the owner must also provide

written approval of the application.

The ratepayer must be the current ratepayer for the Rating Unit at the

time Significant Extraordinary Circumstances are identified by Council.

Where the Council decides to postpone rates the ratepayer must make

acceptable arrangements for payment of rates, for example by setting up a

system for regular payments. Such arrangements will be based on the

circumstances of each case.

Council may charge a fee on postponed rates for the period between the

due date and the date they are paid. This fee is designed to cover

Council’s administrative and financial costs. The fees will be set as

part of the Council resolution identifying Significant Extraordinary

Circumstances.

Postponed rates will remain postponed until the earlier of:

a. The

ratepayer/s ceases to be the owner or occupier of the Rating Unit; or

b. A

date specified by Council in the Council resolution identifying Significant

Extraordinary Circumstances.

Postponement

for Special Circumstances

Objective

To enable Council to provide rates postponement for special and

unforeseen circumstances, where it considers relief by way of rates

postponement is justified in the circumstances.

Conditions

and Criteria

Application for rates postponement must be made in writing by the

ratepayer or their authorised agent.

Each circumstance will be considered by Council on a case by case

basis. Where necessary, Council consideration and decision will be made in the

Public Excluded part of a Council meeting.

The terms and conditions of postponement including any application of

an annual fee will be decided by Council on a case by case basis.

The applicant will be advised in writing of the outcome of the

application.

Policy

Review

This policy will be reviewed at least once every three years.

Document

History

|

Version

|

Reviewer

|

Change Detail

|

Date

|

|

2.0.0

|

Caroline Thompson

|

Updated and approved by Council

|

29 June 2018

|

|

3.0.0

|

|

Updated and approved by Council

|

|

|

Extraordinary Meeting of Council - 11 June 2020 - Attachments

|

Item 1

Attachments b

|

Consultation Plan – Rates Postponement

Policy

Consultation Plan – Rates Postponement

Policy

Introduction

Some changes

to the Rates Postponement Policy are proposed that will provide some

flexibility in times of hardship that affect a large number of our community.

The key change would allow rates to be paid late. While this policy

doesn’t ‘discount’ rates, it does affect the amount of

funding available to the Council in a given timeframe. It is expected the

policy would be applied across the community affected rather than at an

individual ratepayer level, which is already catered for in the current policy.

The current policy allows for delayed payment, and subsequent write off, for

rates applied to farmland, which is believed to discourage residential

development in such areas. It is proposed that this is changed so that rates

are no longer written off after five years, but payment still able to be

delayed, for land in areas identified for residential development.

These policy

changes are aligned with policy changes to the Rates Remission policy, which is

being consulted on at the same time. Both matters will be promoted together

given their strong association.

Significance

and Engagement Policy

It is

anticipated this policy change would be implemented in times when a significant

proportion of the community is affected by an event or hardship, not on a day

to day basis. A large proportion of the community may be affected but as it is

only in place for these one off situations it does not have an ongoing affect.

The matter will be of interest to Napier ratepayers and the wider community and

therefore the consultation will be promoted to the general public. The change

to the rates postponement facility for farmland may be of special interest to

the farming sector.

Purpose

The objective

of the consultation is to provide the community with the opportunity to provide

their feedback on whether or not they support the proposed changes to the Rates

Postponement Policy.

Approach

This

consultation process will be run concurrently with the consultation on the

Annual Plan 2020/21, from 18 June to 15 July and promoted to ratepayers and the

general public. The farming sector has been identified as potentially having a

special interest in the changes to how rates postponement for farmland is

applied. As such, the consultation process will be advised directly to:

· Three property owners who

currently use the postponement facility for farmland

· Federated Farmers

· Hawke’s Bay Regional

Council

· Ministry of Primary

Industries

The policy,

identifying the changes, will be available on www.sayitnapier.nz, along with a short summary and a

submission form. Hard copies of the material will be available at the

Council’s Customer Service Centre, the libraries and by request.

Communication

& Engagement Tools

The

consultation process will be promoted through digital and print channels with a

section also included in the Annual Plan 2020/21 Consultation Document.

|

Digital

|

· Facebook posts

· Digital screens

· Website (www.sayitnapier.nz)

· Email to special interest parties

|

|

Print

|

· Included in the Annual Plan

Consultation Document

· Referenced in the Annual Plan

Summary Brochure

· Informing Napier (advertised with

other consultations)

· The Napier Courier (advertised with

other consultations)

|

Extraordinary Meeting of Council - 11 June

2020 - Open Agenda Item

2

2. Consultation -

Rates Remisson Policy

|

Type of Report:

|

Legal and Operational

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

935164

|

|

Reporting Officer/s & Unit:

|

Garry Hrustinsky, Investment and Funding Manager

|

2.1 Purpose

of Report

To

review and update the policy to include a clearer definition around financial

hardship. To introduce rates remission resulting from Significant

Extraordinary Circumstances. Some minor

clarification of Criteria wording.

|

Officer’s

Recommendation

That Council:

a. Approve the proposed amendments to the Rates

Remission Policy to include Significant Extraordinary Circumstances.

b. Approve

other minor changes detailed in this report.

c. Approval

for consultation on the revised Rates Remission Policy to run parallel but

separately to the Annual Plan 20/21.

d. Approve

the consultation plan for the Rates Remission policy

|

2.2 Background Summary

The COVID-19 pandemic and a

subsequent response planning has highlighted the need to better define rates

remissions for Significant Extraordinary Circumstances.

2.3 Issues

In its current form, the Rates

Remission Policy is structured to review remissions on a very small

(individual) scale. Significant time (including that of Prosperous Napier

Committee) and resources are required to process each application. The proposed

amendment allows the Council to be proactive, and apply broad remissions in

situations where Significant Extraordinary Circumstances are identified.

The proposed amendment is as

follows:

Remission of Rates in

Response to Significant Extraordinary Circumstances being identified by

Council.

Objective

To enable Council to provide

rates remission to assist ratepayers in response to Significant Extraordinary

Circumstances impacting Napier’s ratepayers.

Definitions

Financial Hardship: for the

purpose of this provision is defined as the inability of a person, after

seeking recourse from Government benefits or applicable relief packages, to

reasonably meet the cost of goods, services and financial obligations that are

considered necessary according to New Zealand standards. In the case of a

ratepayer who is not a natural person, it is the inability, after seeking

recourse from Government benefits or applicable relief packages, to reasonably

meet the cost of goods, services and financial obligations that are considered

essential to the functioning of that entity according to New Zealand standards.

Conditions

and Criteria

For this policy to apply

Council must first have identified that there have been Significant Extraordinary

Circumstances affecting the ratepayers of Napier, that Council wishes to

respond to.

Once Significant Extraordinary

Circumstances have been identified by Council, the criteria and application

process (including an application form, if applicable), will be made available.

For a Rating Unit to receive a

remission under this policy it needs to be an “Affected Rating

Unit” based on an assessment performed by officers, following guidance

provided through a resolution of Council.

Council resolution will include:

1. That the resolution applies under the Rates

Remission Policy; and

2. Identification of the Significant

Extraordinary Circumstances triggering the policy (including both natural and

man-made events); and

3. How the Significant Extraordinary Circumstances

are expected to impact the community (e.g. financial hardship); and

4. The type of Rating Unit the remission will

apply to; and

5. Whether individual applications are required

or a broad based remission will be applied to all affected Rating Units or

large groups of affected Rating Units; and

6. What rates instalment/s the remission will

apply to; and

7. Whether the remission amount is either a

fixed amount, percentage, and/or maximum amount to be remitted for each

qualifying Rating Unit.

Explanation

The specific response and

criteria will be set out by Council resolution linking the response to specific

Significant Extraordinary Circumstances. The criteria may apply a

remission broadly to all Rating Units or to specific groups or to Rating Units that

meet specific criteria such as proven Financial Hardship, a percentage of

income lost or some other criteria as determined by council and incorporated in

a council resolution.

Council will indicate a budget

to cover the value of remissions to be granted under this policy in any

specific financial year.

The types of remission that

may be applied under this policy include:

· The

remission of a fixed amount per Rating Unit either across the board or targeted

to specific groups such as:

§ A fixed amount per

residential Rating Unit

§ A fixed amount per

commercial Rating Unit

Further minor amendments include:

Provision for the remission of

penalties through identification of Significant Extraordinary Circumstances.

Applications under Remission for

Special Circumstances can now be made by the “…ratepayer or their

authorised agent...” instead of solely by the “ratepayer”.

2.4 Significance

and Engagement

There has been no external

consultation on the proposed changes.

The proposed amendments are

similar to those already in place, or proposed, for other Councils.

Significance of the proposed

amendments are high as they could potentially impact proportion of residents or

ratepayers.

If approved, public consultation

will be required and will be run in parallel to the Annual Plan 20/21.

2.5 Implications

Financial

N/A

Social &

Policy

The proposed amendment will allow

Napier City Council to be more responsive, by way of financial relief, to any

events that have a material negative impact on the wider city.

Risk

Taking the Rates Remission Policy in its current form, the

Council is not well placed to provide timely relief via remission, and may be

overwhelmed due to administrative burden should further Significant

Extraordinary Circumstances occur.

2.6 Options

The options available to Council

are as follows:

a. Adopt

all of the proposed changes.

b. Adopt

selected proposed changes.

c. Adopt

none of the proposed changes.

2.7 Development

of Preferred Option

The proposed changes to the Rates

Remission Policy allow Council to be more responsive in times of Significant

Extraordinary Circumstances impacting the community.

2.8 Attachments

a Rates

Remission Policy ⇩

b Consultation

Plan - Rates Remission Policy ⇩

|

Extraordinary Meeting of

Council - 11 June 2020 - Attachments

|

Item 2

Attachments a

|

|

Rates

Remission Policy

|

|

Approved

by

|

Pending

Approval by Council

|

|

Department

|

Finance

|

|

Original

Approval Date

|

30

June 2019

|

Review

Approval Date

|

June

2020

|

|

Next

Review Deadline

|

June

2023

|

Document

ID

|

|

|

Relevant

Legislation

|

Local

Government Act 2002, Local Government (Rating) Act 2002

|

|

NCC

Documents Referenced

|

Published

in the Long Term Plan 2018-2028 which was reviewed between March/Apr 2018 and

adopted on 29-06-18

Reviewed

and amended as part of 2019/20 Annual Plan

Reviewed

and amended as part of 2020/21 Annual Plan

|

Purpose

To enable Council to remit all or part of

the rates on a rating unit under Section 85 of the Local Government (Rating)

Act 2002 where a Rates Remission Policy has been adopted and the conditions and

criteria in the policy are met.

Policy

1. Remission of Penalties

Objective

The objective of this part of the Rates

Remission Policy is to enable Council to act fairly and reasonably in its

consideration of rates which have not been received by the Council by the

penalty date due to circumstances outside the ratepayer’s control.

Conditions and Criteria

Penalties incurred will be automatically

remitted where Council has made an error which results in a penalty being

applied.

Remission of one penalty will be

considered in any one rating year where payment has been late due to

significant family disruption. This will apply in the case of death, illness,

or accident of a family member, at about the times rates are due.

Remission of the penalty will be

considered if the ratepayer forgets to make payment, claims a rates invoice was

not received, is able to provide evidence that their payment has gone astray in

the post, or the late payment has otherwise resulted from matters outside their

control. Each application will be considered on its merits and remission will

be granted where it is considered just and equitable to do so

Remission of a penalty will be considered

where sale has taken place very close to due date, resulting in confusion over

liability, and the notice of sale has been promptly filed, or where the

solicitor who acted in the sale for the owner acted promptly but made a mistake

(e.g. inadvertently provided the wrong name and address) and the owner cannot

be contacted. Each case shall be treated on its merits.

Penalties will also be remitted based on

the application, by officers, of Council criteria established after Council has

identified that Significant Extraordinary Circumstances have occurred that

warrants further leniency in relation to the enforcement of penalties that

would otherwise have been payable. The criteria to be applied will be set out

in a council resolution that will be linked to the specific Significant

Extraordinary Circumstances that have been identified by Council.

Penalties will also be remitted where

Council’s Chief Financial Officer considers a remission of the penalty,

on the most recent instalment, is appropriate as part of an arrangement to

collect outstanding rates from a ratepayer.

2. Remission for Residential Land in

Commercial or Industrial Areas

Objective

To ensure that owners of rating

units situated in commercial or industrial areas are not unduly penalised by

the zoning decisions of this Council and previous local authorities.

Conditions and Criteria

To qualify for remission under

this part of the policy the rating unit must:

· Be situated within an area of land that has

been zoned for commercial or industrial use. Ratepayers can determine where

their property has been zoned by inspecting the City of Napier District Plan,

copies of which are available from the Council office.

· Be listed as a ‘residential’

property for differential rating purposes. Ratepayers wishing to ascertain

whether their property is treated as a residential property may inspect the

Council’s rating information database at the Council office.

Rates will be automatically

remitted annually for those properties which had Special Rateable Values

applied under Section 24 of the Rating Valuations Act 1998 up to 30 June 2003,

and for which evidence from Council’s Valuation Service Provider

indicates that, with effect from the 2002 revaluation of Napier City, the land

value has been penalised by its zoning. The amount remitted will be the

difference between the rates calculated on the equivalent special rateable

value provided by the Valuation Service Provider and the rates payable on the

Rateable Value.

Other ratepayers wishing to

claim remission under this part of the policy must make an application in

writing addressed to the Chief Financial Officer.

The application for rates

remission must be made to the Council prior to the commencement of the rating

year. Applications received during a rating year will be applicable from the

commencement of the following rating year. Applications will not be backdated.

Where an application is

approved, the Council will direct its Valuation Service Provider to inspect the

rating unit and prepare a valuation that will treat the rating unit as if it

were a comparable rating unit elsewhere in the district. The ratepayer may be

asked to contribute to the cost of this valuation. Ratepayers should note that

the Valuation Service Provider’s decision is final as there are no

statutory right of objection or appeal for values done in this way.

3. Remission for Land Subject to Special Preservation Conditions

Objective

To preserve and encourage the

protection of land and improvements which are the subject of special

preservation conditions.

Conditions and Criteria

Rates remission under this Section of the

policy relates to land that is subject to:

· A heritage covenant under the Historic

Places Act 1993; or

· A heritage order under the Resource

Management Act 1991; or

· An open space covenant under the Queen

Elizabeth the Second National Trust Act 1977; or

· A protected private land agreement or

conservation covenant under the Reserves Act 1977; or

· Any other covenant or agreement entered

into by the owner of the land with a public body for the preservation of

existing features of land, or of buildings, where the conditions of the

covenant or agreement are registered against the title to the land and are

binding on subsequent owners of land.

Ratepayers who own Rating Units meeting

this criteria may qualify for remission under this part of the policy.

Rates will automatically be remitted

annually for those properties which had Special Rateable Values applied under

Section 27 of the Rating Valuations Act up to 30 June 2003, and which meet the

above criteria. The amount remitted will be the difference between the rates

calculated on the equivalent special rateable value provided by the Valuation Service

Provider and the rates payable on the Rateable Value.

Other ratepayers wishing to claim

remission under this part of the policy must apply in writing to the Council

office, and must provide supporting documentary evidence of the special

preservation conditions, e.g. copy of the Covenant, Order or other legal

mechanism.

The application for rates remission must

be made to the Council prior to the commencement of the rating year.

Applications received during a rating year will be applicable from the commencement

of the following rating year.

Applications for remission under this part

of the policy will be approved by the Council. The Council may specify certain

conditions before remission will be granted. Applicants will be required to

agree in writing to these conditions and to pay any remitted rates if the

conditions are violated.

Where an application is approved, the

Council will direct its Valuation Service Provider to inspect the Rating Unit

and provide a special valuation. The ratepayer may be asked to contribute to

the cost of this valuation. Ratepayers should note that the Valuation Service

Provider’s decision is final as there is no statutory right of objection

or appeal for values done in this way.

The equivalent special rateable value will

be determined by the Valuation Service Provider on the assumption that:

· The actual use to which the land is being

put at the date of valuation will be continued; and

· Any improvements on the land will be

continued and maintained or replaced in order to enable the land to continue to

be so used.

It will be assessed taking into account

any restriction on the use that may be made of the land imposed by the

mandatory preservation of any existing tenements, hereditaments, trees,

buildings, other improvements, and features.

4. Remission of Uniform Annual General Charges (UAGC) and Targeted Rates of

a Fixed Amount on Rating Units Owned by the Same Owner

Objective

To provide for relief from UAGC and

Targeted Rates of a fixed amount per Rating Unit or Separately Used or

Inhabited Parts of a Rating Unit, where two or more Rating Units are owned by

the same person or persons, and are:

· part of a subdivision plan which has been

deposited for separate lots, or separate legal titles exist; or

· but the Rating Units may not necessarily be

used jointly as a single unit, and each Rating Unit does not benefit separately

from the services related to the UAGC and Targeted Rates.

Conditions and Criteria

Remission of UAGC and Targeted Rates of a

fixed amount applies in the following situations:

· Unsold subdivided land, where as a result

of the High Court decision of 20 November 2000 ‘Neil Construction and

others vs. North Shore City Council and others’, each separate lot or

title is treated as a separate Rating Unit, and such land is implied to be not

used as a single unit.

All remissions under this part of the

policy will be approved by the Chief Financial Officer.

5. Remission for Water Rates (by meter)

Objective

To provide ratepayers with a measure of

relief by way of partial rates remission where, as a result of the existence of

a water leak on the Rating Unit which they occupy the payment of fuller rates

is inequitable, or where officers are convinced that there are errors in the

data relating to water usage.

Conditions

and Criteria

· The existence of a significant leak on the occupied

Rating Unit has been established and there is evidence that steps have been

taken to repair the leak as soon as possible after the detection, or officers

have reviewed the usage data and are convinced that the usage readings are so

abnormal as to require adjustment.

· The Council or its delegated officer(s) as determined

from time to time and set out in the Council’s delegations register shall

determine the extent of any remission based on the merits of each situation.

6. Remission to smooth the effects of change in rates on individual or

groups of properties

Objective

To enable Council to provide rates

remission where, as a result of a change in Council policy or other change that

results in a significant increase in rates, Council decides it is equitable to

smooth or temporarily reduce the impacts of the change by reducing the amount

payable.

Conditions and Criteria

· Remission of part of the value based rates to enable

the impact of a change in rates to be phased in over a period of no more than 3

years.

To continue with any existing rates

adjustment where, due to change in process, policy or legislation Council

considers it equitable to do so subject to a maximum limit of 3 years to a

remission made under this clause in the policy.

7. Remission for Special Circumstances

Objective

To enable Council to provide rates

remission for special and unforeseen circumstances, where it considers relief

by way of rates remission is justified in the circumstances.

Conditions and Criteria

Applications for rates remission must be

made in writing by the ratepayer or their authorised agent.

Each circumstance will be considered by

Council on a case by case basis. Where necessary, Council consideration and

decision will be made in the Public Excluded part of a Council meeting.

The terms and conditions of remission will

be decided by Council on a case by case basis. The applicant will be advised in

writing of the outcome of the application.

8. Remission of Rates in Response to Significant Extraordinary Circumstances

being identified by Council.

Objective

To enable Council to provide rates

remission to assist ratepayers in response to Significant Extraordinary

Circumstances impacting Napier’s ratepayers.

Definitions

Financial Hardship: for the purpose of

this provision is defined as the inability of a person, after seeking recourse

from Government benefits or applicable relief packages, to reasonably meet the

cost of goods, services and financial obligations that are considered necessary

according to New Zealand standards. In the case of a ratepayer who is not a

natural person, it is the inability, after seeking recourse from Government

benefits or applicable relief packages, to reasonably meet the cost of goods,

services and financial obligations that are considered essential to the

functioning of that entity according to New Zealand standards.

Conditions and Criteria

For this policy to apply Council must

first have identified that there have been Significant Extraordinary

Circumstances affecting the ratepayers of Napier, that Council wishes to

respond to.

Once Significant Extraordinary

Circumstances have been identified by Council, the criteria and application

process (including an application form, if applicable), will be made available.

For a Rating Unit to receive a remission

under this policy it needs to be an “Affected Rating Unit” based on

an assessment performed by officers, following guidance provided through a

resolution of Council.

Council resolution will include:

1. That the resolution applies under the

Rates Remission Policy; and

2. Identification of the Significant

Extraordinary Circumstances triggering the policy (including both natural and

man-made events); and

3. How the Significant Extraordinary Circumstances

are expected to impact the community (e.g. financial hardship); and

4. The type of Rating Unit the remission

will apply to; and

5. Whether individual applications are

required or a broad based remission will be applied to all affected Rating Units

or large groups of affected Rating Units; and

6. What rates instalment/s the remission

will apply to; and

7. Whether the remission amount is either a

fixed amount, percentage, and/or maximum amount to be remitted for each

qualifying Rating Unit.

Explanation

The specific response and criteria will be

set out by Council resolution linking the response to specific Significant Extraordinary Circumstances. The criteria may apply a remission broadly to all

Rating Units or to specific groups or to Rating Units that meet specific

criteria such as proven Financial Hardship, a percentage of income lost or some

other criteria as determined by council and incorporated in a council

resolution.

Council will indicate a budget to cover

the value of remissions to be granted under this policy in any specific

financial year.

The types of remission that may be applied

under this policy include:

· The remission of a fixed amount per Rating Unit either

across the board or targeted to specific groups such as:

o A fixed amount per residential Rating Unit

o A fixed amount per commercial Rating Unit

Policy Review

This policy will be reviewed at least once

every three years.

Document History

|

Version

|

Reviewer

|

Change Detail

|

Date

|

|

2.0.0

|

Caroline Thomson

|

Updated and approved by Council

with LTP

|

29 June 2018

|

|

3.0.0

|

Caroline Thomson

|

Updated in conjunction with

2019-20 Annual Plan

|

4 June 2019

|

|

4.0.0

|

|

Updated in conjunction with

2020-21 Annual Plan

|

|

|

Extraordinary Meeting of Council - 11 June 2020 - Attachments

|

Item 2

Attachments b

|

Consultation Plan – Rates Remission

Policy

Consultation Plan – Rates Remission

Policy

Introduction

Some changes

to the Rates Remission Policy are proposed that will provide some flexibility

in times of hardship that affect a large number of our community. The key

change would allow a Council to refund or discount rates and rates-relation

penalties (e.g. late fees). It is expected the policy would be applied across

the community affected rather than at an individual ratepayer level, which is already

catered for in the current policy. This policy change, when applied, will

reduce the income Council receives from rates at that time.

These policy

changes are aligned with policy changes to the Rates Postponement Policy, which

is being consulted on at the same time. Both matters will be promoted together

given their strong association.

Significance

and Engagement Policy

It is

anticipated this policy change would be implemented in times when a significant

proportion of the community is affected by an event or hardship, not on a day

to day basis. A large proportion of the community may be affected at a given

time. The matter will be of interest to Napier ratepayers and the wider

community and therefore the consultation will be promoted to the general

public. There are no other parties identified as having a special interest in

this matter, so no targeted consultation will be undertaken.

Purpose

The objective

of the consultation is to provide the community with the opportunity to provide

their feedback on whether or not they support the proposed changes to the Rates

Remission Policy.

Approach

This

consultation process will be run concurrently with the consultation on the

Annual Plan 2020/21, from 18 June to 15 July and promoted to ratepayers and the

general public.

The policy,

identifying the changes, will be available on www.sayitnapier.nz, along with a short summary and a

submission form. Hard copies of the material will be available at the

Council’s Customer Service Centre, the libraries and by request.

Communication

& Engagement Tools

The

consultation process will be promoted through digital and print channels with a

section also included in the Annual Plan 2020/21 Consultation Document.

|

Digital

|

· Facebook posts

· Digital screens

· Website (www.sayitnapier.nz)

|

|

Print

|

· Included in the Annual Plan

Consultation Document

· Referenced in the Annual Plan

Summary Brochure

· Informing Napier (advertised with

other consultations)

· The Napier Courier (advertised with

other consultations)

|

Extraordinary Meeting of Council - 11 June

2020 - Open Agenda Item

3

3. Consultation Document and

Draft Annual Plan 2020/21

|

Type of Report:

|

Legal

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

935370

|

|

Reporting Officer/s & Unit:

|

Adele Henderson, Director Corporate Services

|

3.1 Purpose of Report

To present the consultation document

and supporting information for the Annual Plan 2020/21 for Council adoption.

|

Officer’s Recommendation

That

Council:

a. Note that the

Annual Plan 2020/21 does not meet the section 100 (i) balanced budget

provision of the Local Government Act 2002, and Council will work towards a

balanced budget for the Long Term Plan 2021-31.

b. Adopt the following

documents as supporting information for the Annual Plan 2020/21:

i. Draft

Annual Plan financials for 2020/21

ii. FAQs

– Water

iii. FAQs

– Waste

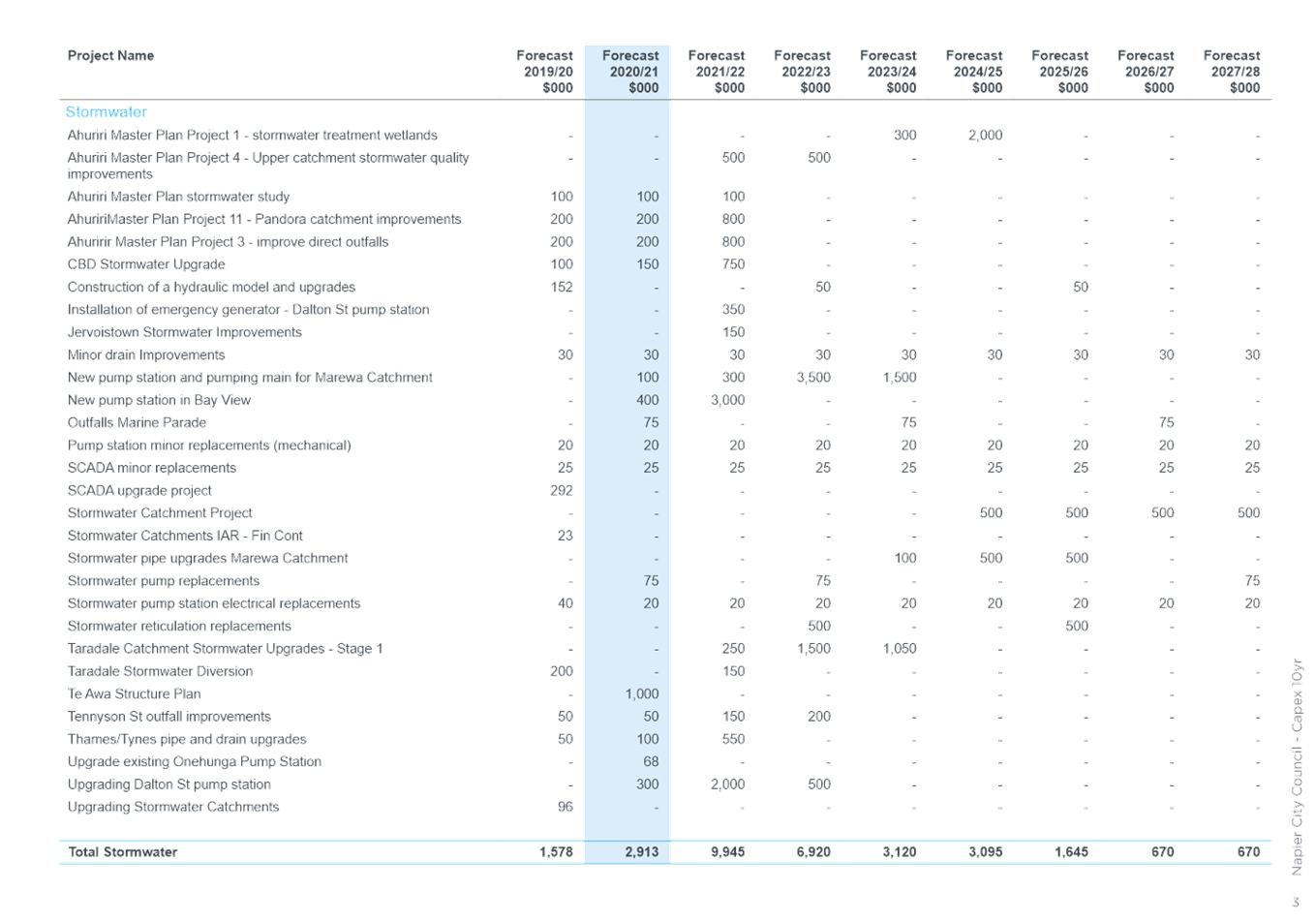

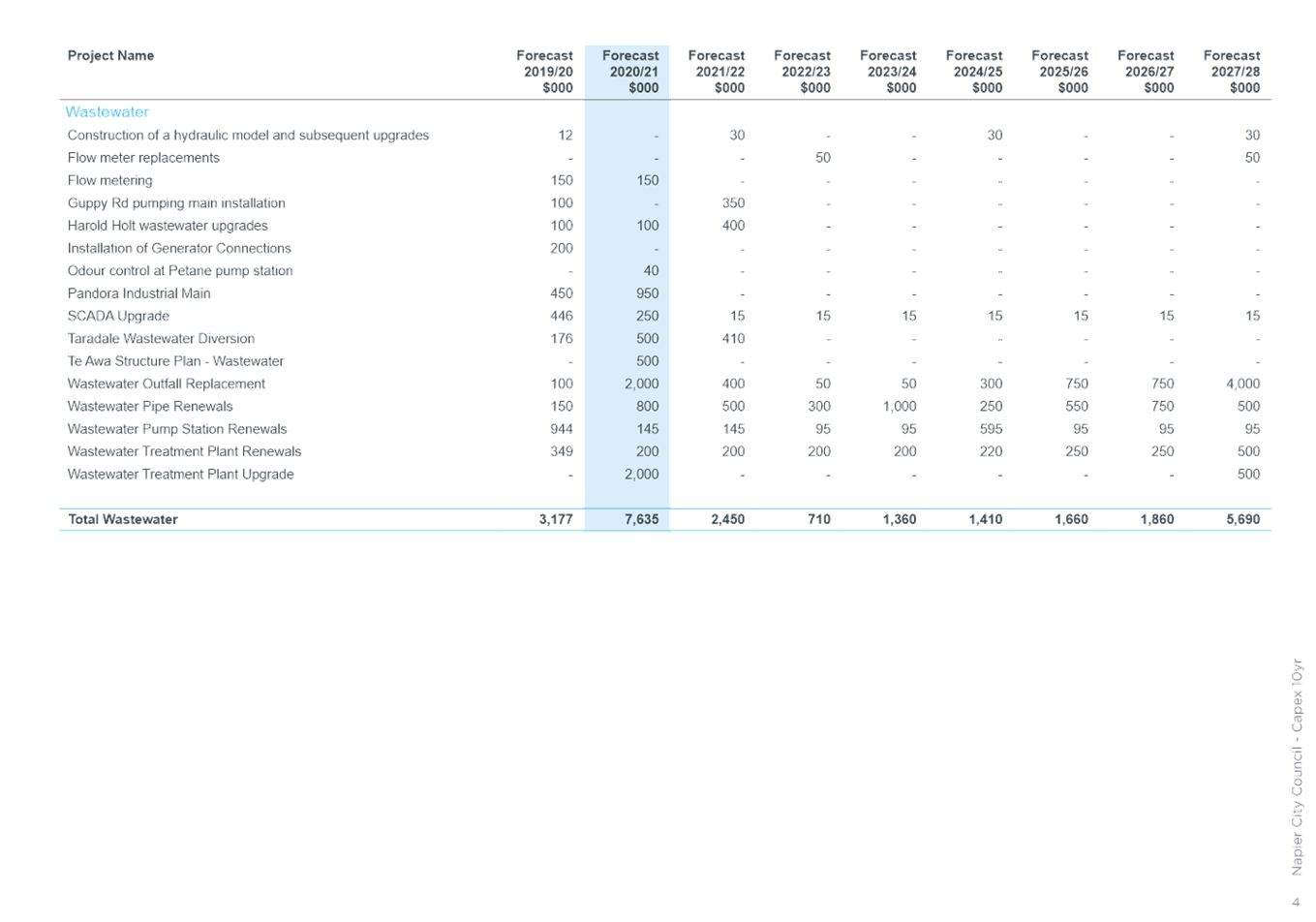

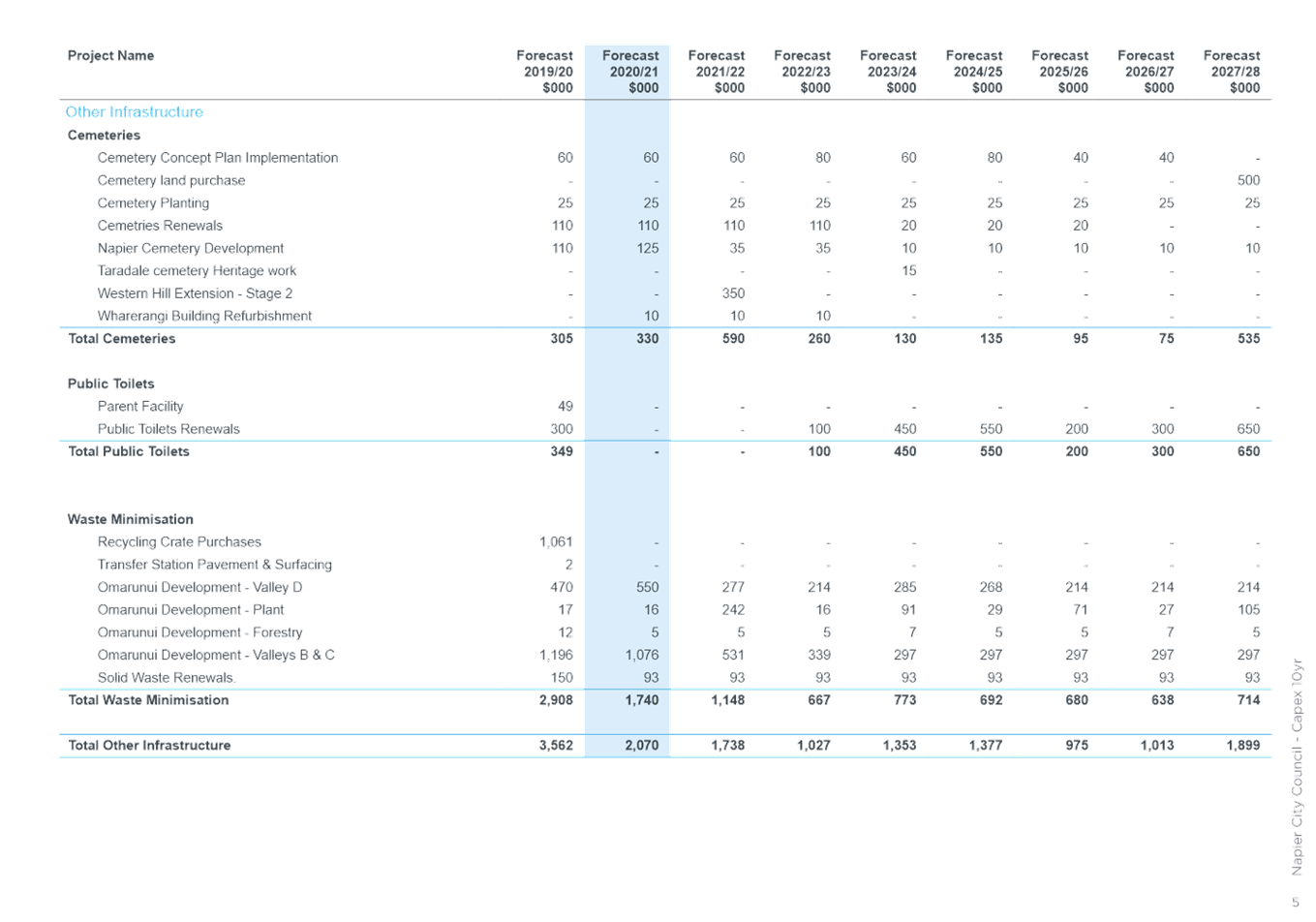

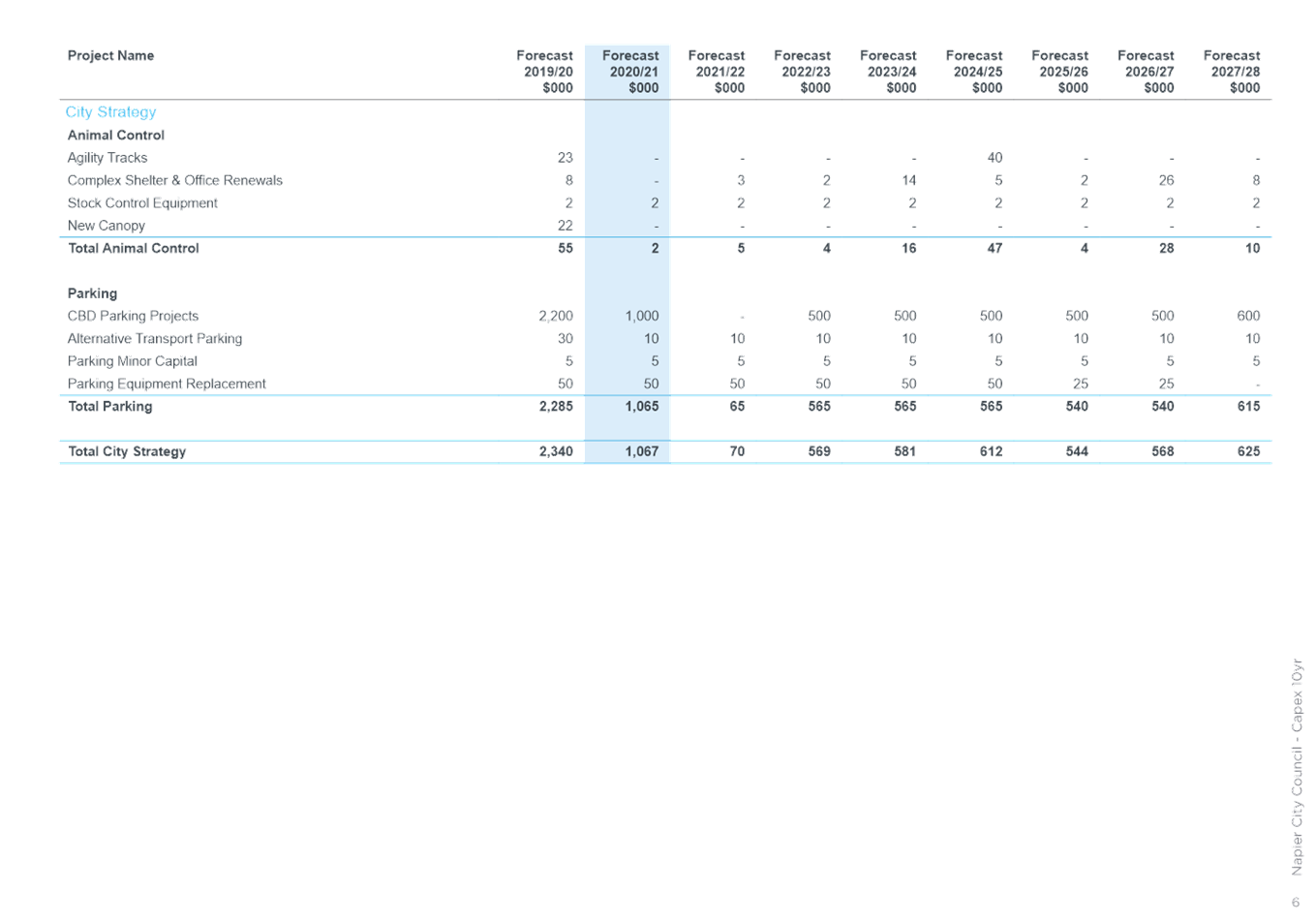

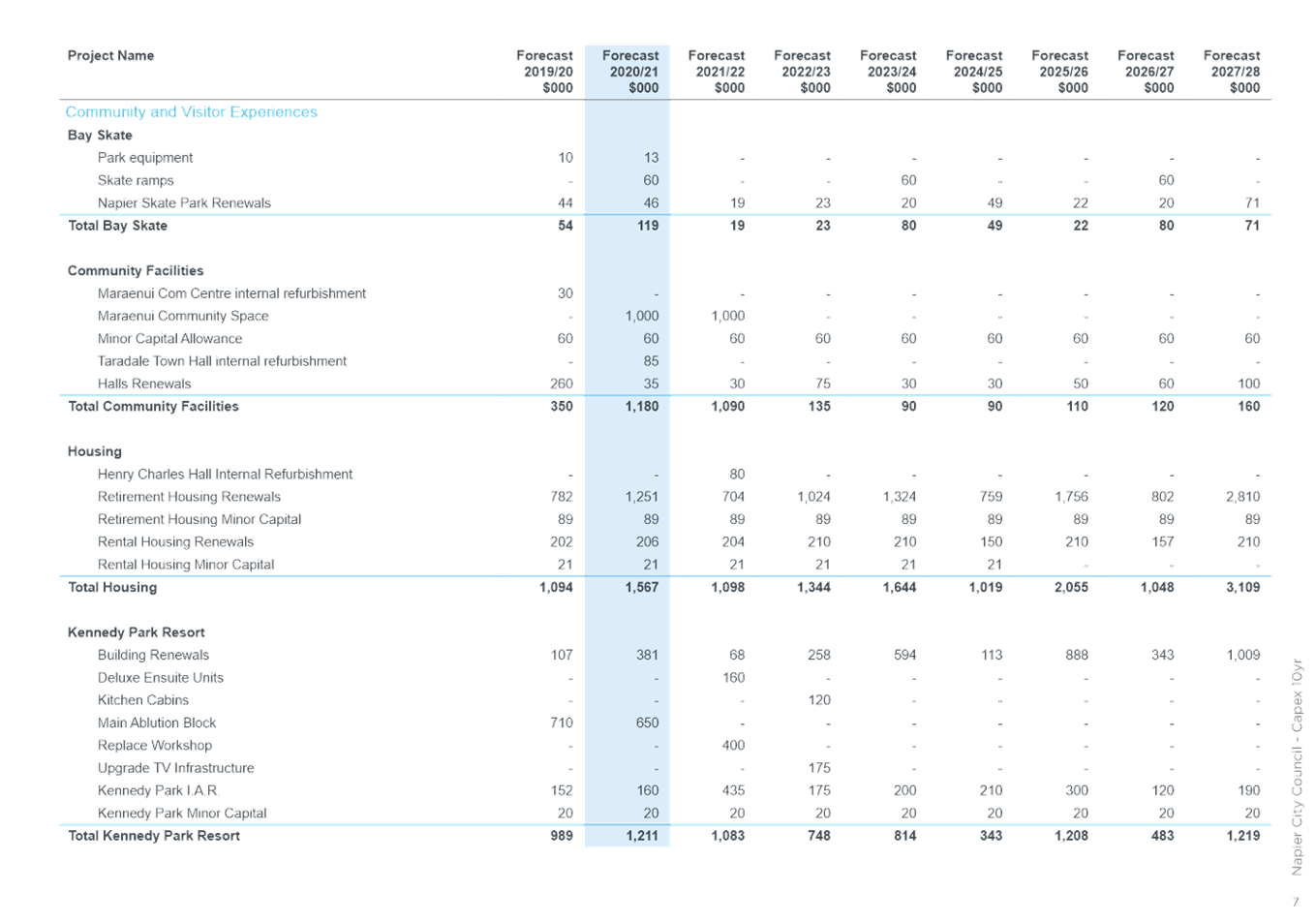

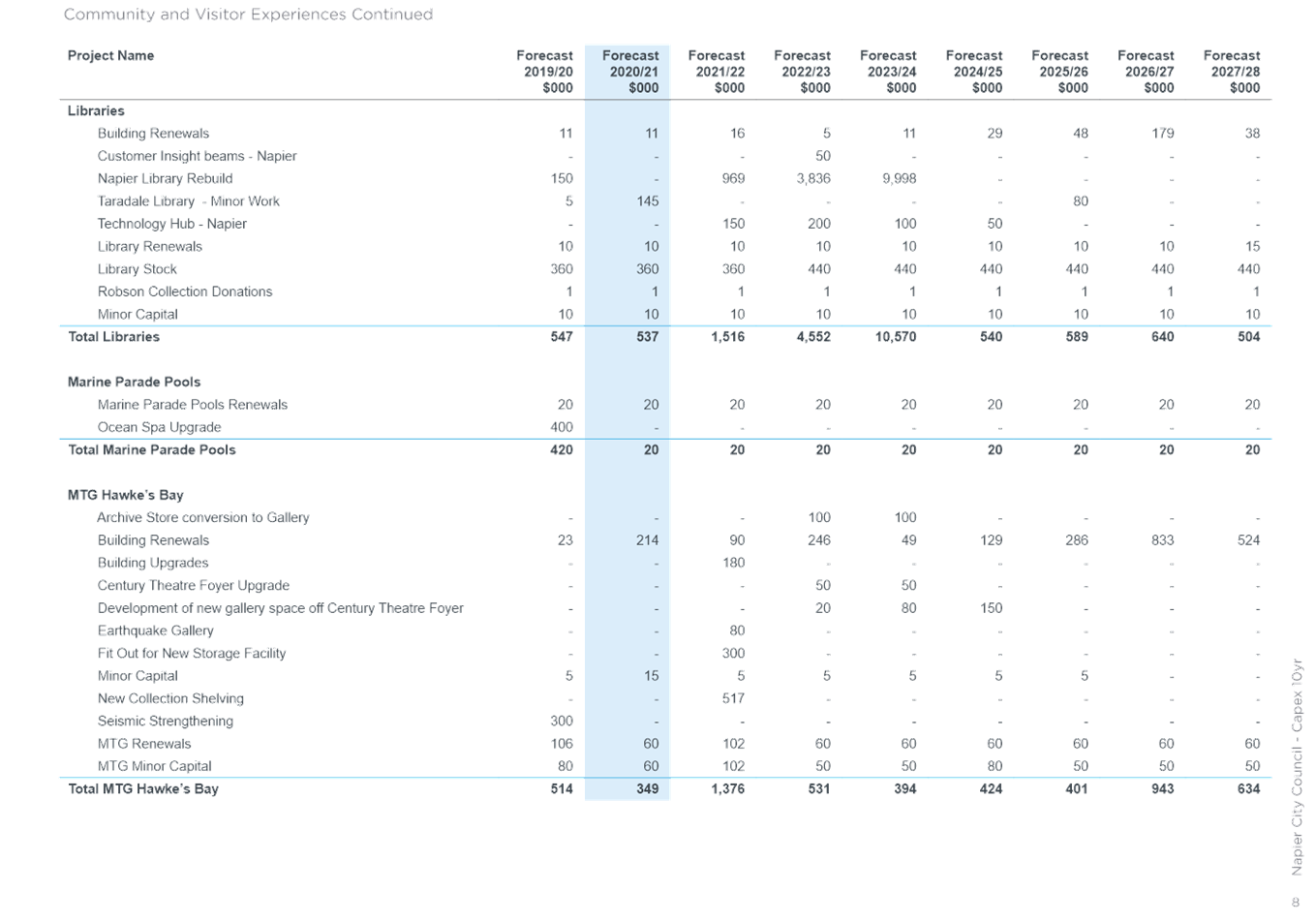

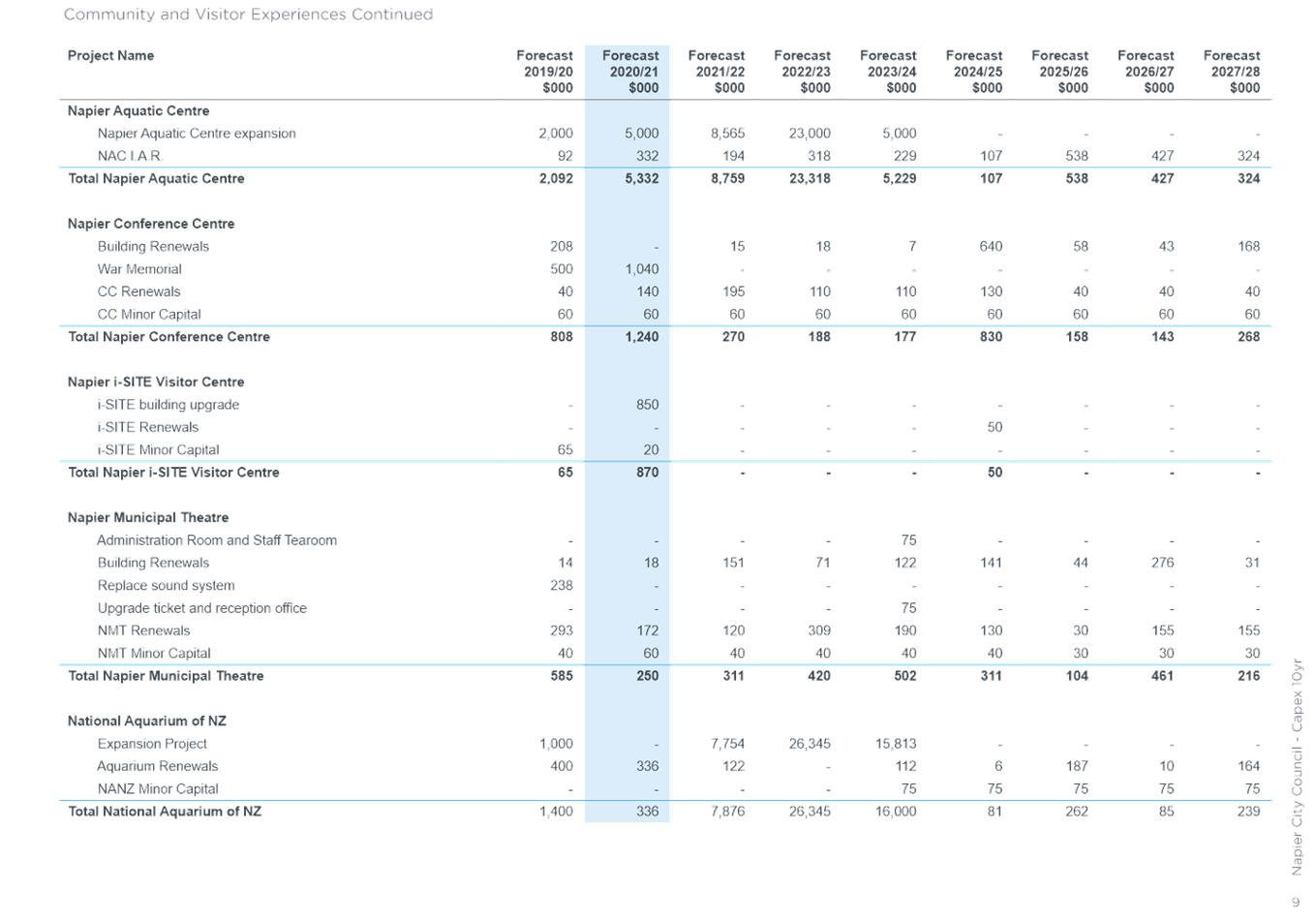

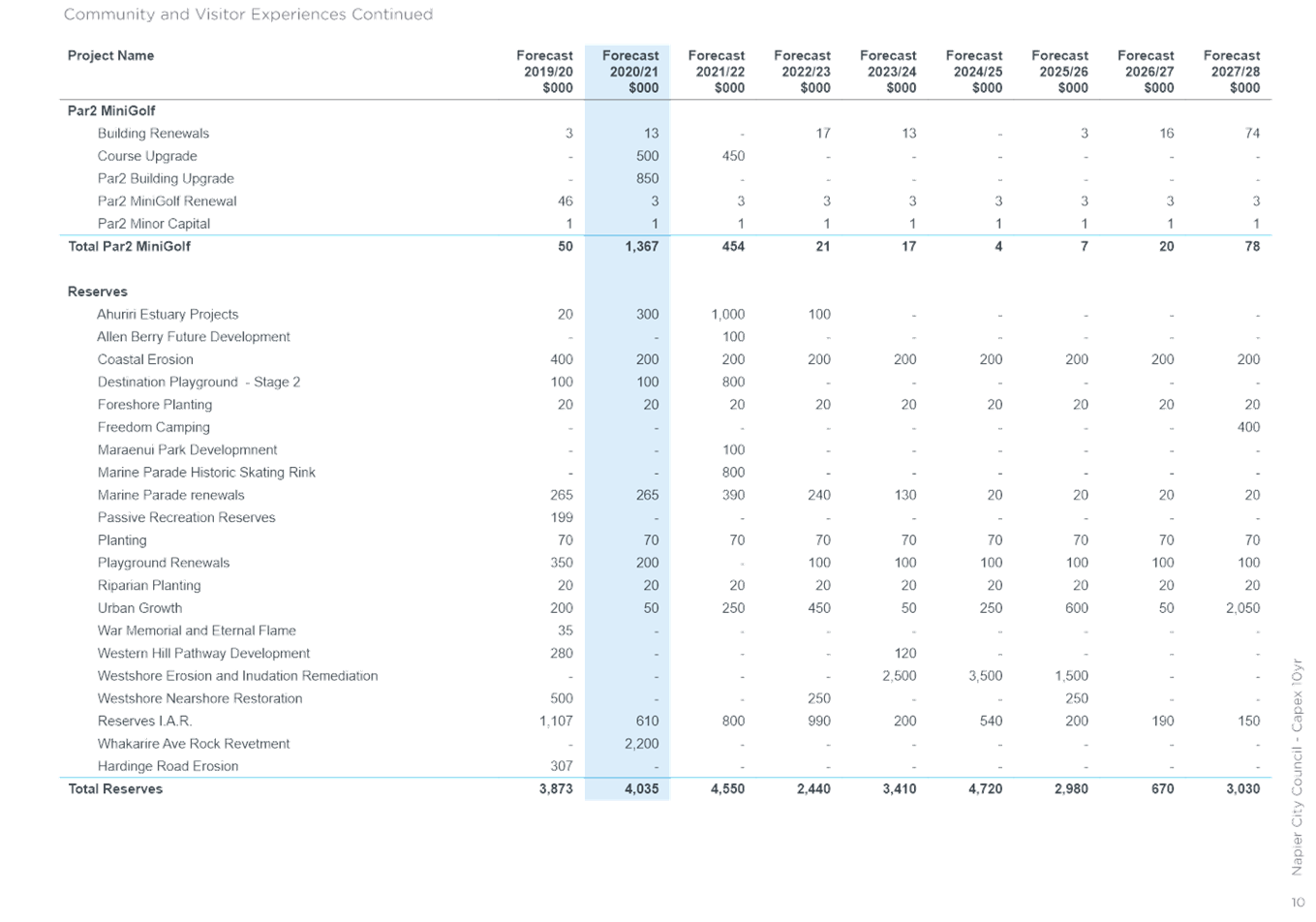

iv. Capital

Programme Changes

v. Remaining

capital programme projection for Long Term Plan 2018-28

vi. Long

Term Plan 2018-28 Major Projects Update

vii. Where

your rates dollar goes

viii. Water

Supply Network Master Plan, Council report and minutes

ix. Civic

Precinct Report (Library) Council report and minutes

x. Whakarire

Revetment – Funding Decision, Council report and minutes and Consultation

Summary

xi. Project

Shapeshifter business case

xii. Napier

Aquatic Development Update, Council report and minutes

xiii. Napier

Recovery Plan, Napier Recovery Budget, Council report and minutes

xiv. Schedule

of Fees and Charges 2020/21

xv. Annual

Plan proposed rate increase options.

c. Adopt the Consultation Document to form

the basis of Council’s consultation with the community on the Annual

Plan 2020/21.

d. Note that separate consultation will

occur on the proposed Rates Remissions Policy; Local Government Funding

Agency; and Rates Postponement Policy.

e. Delegate responsibility to the Chief

Financial Officer to approve any final edits required to the Consultation

Document, financial information and supporting information in order to

finalise the documents for uploading online and physical distribution.

f. Adopt the high level consultation plan

and note that it includes options for engagement under different alert levels

should Alert Levels for Covid-19 change during the consultation period.

|

3.2 Background

Summary

Process to develop annual budget

The process to develop council’s annual budget for the

financial year commencing 1 July 2020 ending on 30 June 2021, began in November

2019, with a series of workshops with Councillors to set direction on the

budget. These seminars occurred on 27 November, 4 December, 12 December, 23

January, 5 February, 10 February, and 20 February. Councillors were provided

with cost pressures and efficiencies that could be made, and set direction to

stay within the financial limits as outlined in the Financial Strategy. On 10

March 2020, Council approved the underlying material, assumptions and key

decisions for the development of the draft Annual Plan 2020/21 and Consultation

Document including a proposed average rates increase of 6.5% for existing

ratepayers. The 6.5% was due to increases relating to waste, recycling

and water-related projects.

Officers

then prepared the Annual Plan 2020/21 Consultation Document and supporting

information for community consultation based on the decisions of the 10 March

2020 meeting to present to Council on 31 March 2020.

On

20 March 2020, at the Audit and Risk Committee meeting, the Annual Plan 2020/21

was discussed, and Council’s Auditor and Audit and Risk Committee

directed Council to review the Annual Plan 2020/21 in light of Covid-19

impacts, particularly as Napier City Council receives only 51% of its total

income from rates. It is a legislative requirement under the Local Government

Act 2002 to have a balanced budget. The impact of Covid-19 on revenue would

result in an unbalanced budget, and therefore Council had to review its 2020/21

budget.

On

25 March 2020, central government moved New Zealand to Alert Level 4, and then

moved into Alert Level 3 on 27 April, then to Alert Level 2 on 13 May. At

the time of this report, New Zealand remains in Alert Level 2. The

impacts of the Alert Levels and the global response to the pandemic have caused

significant implications for our community, and changes the context within

which the Council can deliver its services and within which it must assess the

corresponding budgetary implications.

In

April 2020, Officers developed a project plan to develop a revised Annual Plan

2020/21 that allowed for revision of content and impact on timelines for

consulting and hearings. The revised adoption date is set for 27 August.

Adoption no later than this date will ensure that rates notices are delivered

within quarter one to mitigate cashflow issues; and allow commencement of

capital projects planned for 2020/21 as soon as possible.

|

Description

|

Indicative Date(s)

|

|

Consultation

|

18 June – 15

July 2020

|

|

Extraordinary Council

meeting - Annual Plan 2020/21 & Special Consultative Process Hearing

|

12/13 August 2020

|

|

Extraordinary Council

meeting - Annual Plan 2020/21 Adoption & Rates Setting

|

27 August 2020

|

|

Issue rates

notices

|

10 September 2020

|

On

23 April, Council agreed to the deferral of the release of the Annual Plan

2020/21 until the most appropriate plan for the changed context of Covid-19 was

developed and agreed by Council. Council noted that by deferring the

release of the plan, Council will be in breach of the legislative timelines

under the Local Government Act 2002 to adopt the Annual Plan 2020/21 by 30 June

the year prior to the plan commencing.

Advice

provided by LGNZ, SOLGM and supported by Simpson Grierson confirms that an

Annual Plan 2020/21 adopted after 30 June is lawful and if challenged is

unlikely to be declared invalid provided the delay can be explained and the

plan is not acted on until it is adopted. Audit NZ and the Department of

Internal Affairs (DIA) have been advised of the late adoption date for the

Annual Plan 2020/21.

Elected

Members attended weekly workshops throughout April and May covering budget

impacts, revised significant forecasting assumptions, rates (including funding

options to reduce 2020/21 rates increase), options analysis and impact on

future year’s rates and loans, proposed recovery package budget, risks,

financial policies, and consultation. The Audit and Risk Committee was

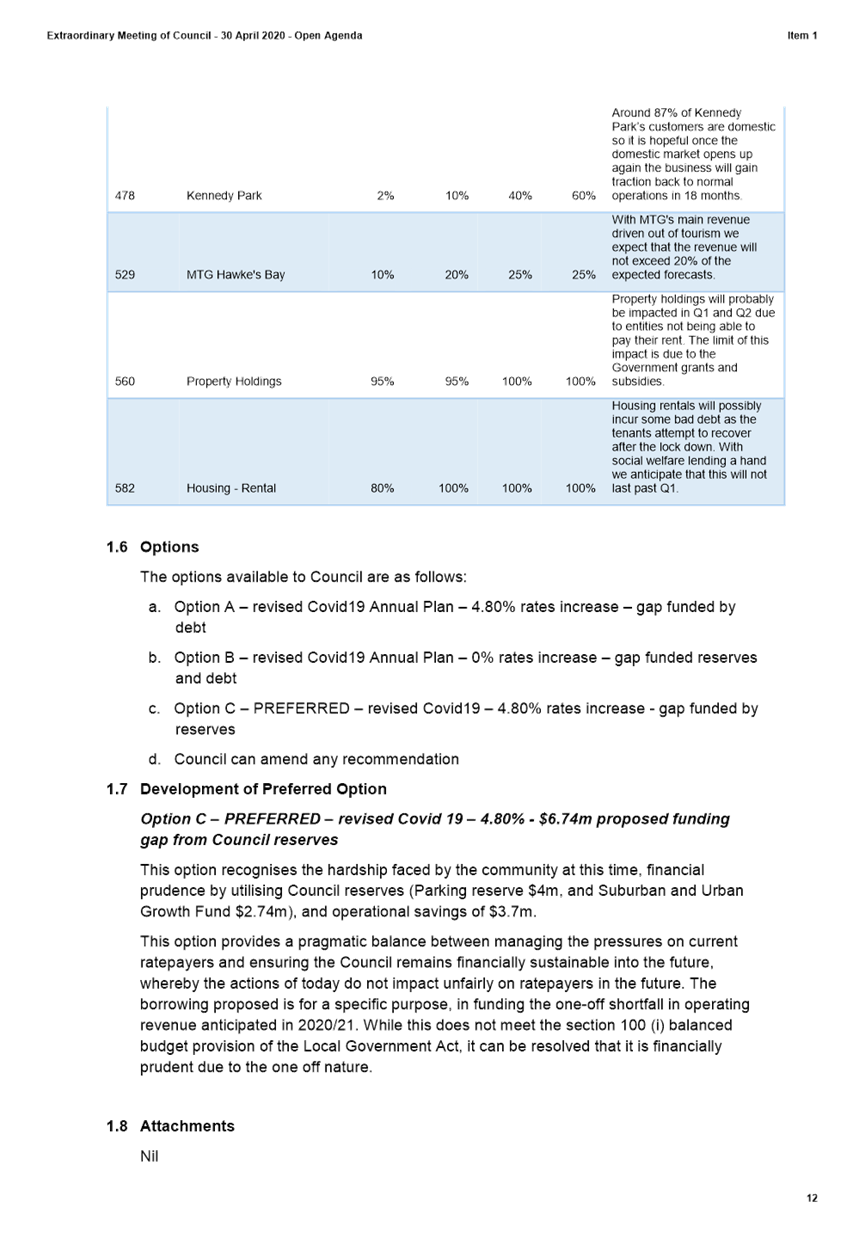

updated fortnightly. Council set direction on a 4.8% rates increase.

Budget review

Proposed rates increase

Officers

reviewed the budget in light of Covid-19 impacts to achieve a 4.8% rates

increase and $3.7M of savings were identified across the board which are not

expected to unduly impact levels of service. Officers also revised

planning assumptions, and provided Council with a shortlist of options to fund

the operating deficit $6.74M for 20/21 with a preferred option of utilising

Council reserves.

Capital programme

The

capital programme has not changed significantly as projects have already been

programmed. Any changes to the programme of work will be addressed through

officer’s submissions to the Annual Plan 2020/21. The currently known

proposed changes to the capital programme and remaining years of the capital programme

for the current LTP are listed as supporting documents to the Annual Plan

2020/21. Delivery of the capital plan is an important aspect of economic

recovery. Council will consider any final changes required for the capital plan

as part of its final deliberation.

Central government funding

Officers

have also applied for central government funding for a number funding streams

available through Covid-19 recovery and at the time of this report are awaiting

feedback.

Napier recovery plan

In

parallel to the development of the revised Annual Plan 2020/21, officers

revised the Rates Postponement Policy and Rates Remissions Policy to enable

Council to provide relief for hardship to the community; and developed the

Napier City Recovery Plan which includes:

· 543K for rates and

rental relief for residents, businesses and community groups. Up to 350K

available for residential reductions of up to $200; up to $500 for commercial

reductions; and up to 193K for rental relief for organisations that are charged

to rent, lease or for a license to occupy any Council land or premises.

· $1M to support recovery

including continued support for We are Team Napier; Jump Start Innovation fund

to support great ideas that help accelerate recovery for our community and or

economy; Using the rest of the funding to support emerging ideas and longer

term strategies.

External borrowing

Despite

not requiring external borrowing in the past, the financial forecast taking

into consideration Covid-19 impacts identified that Napier City Council may

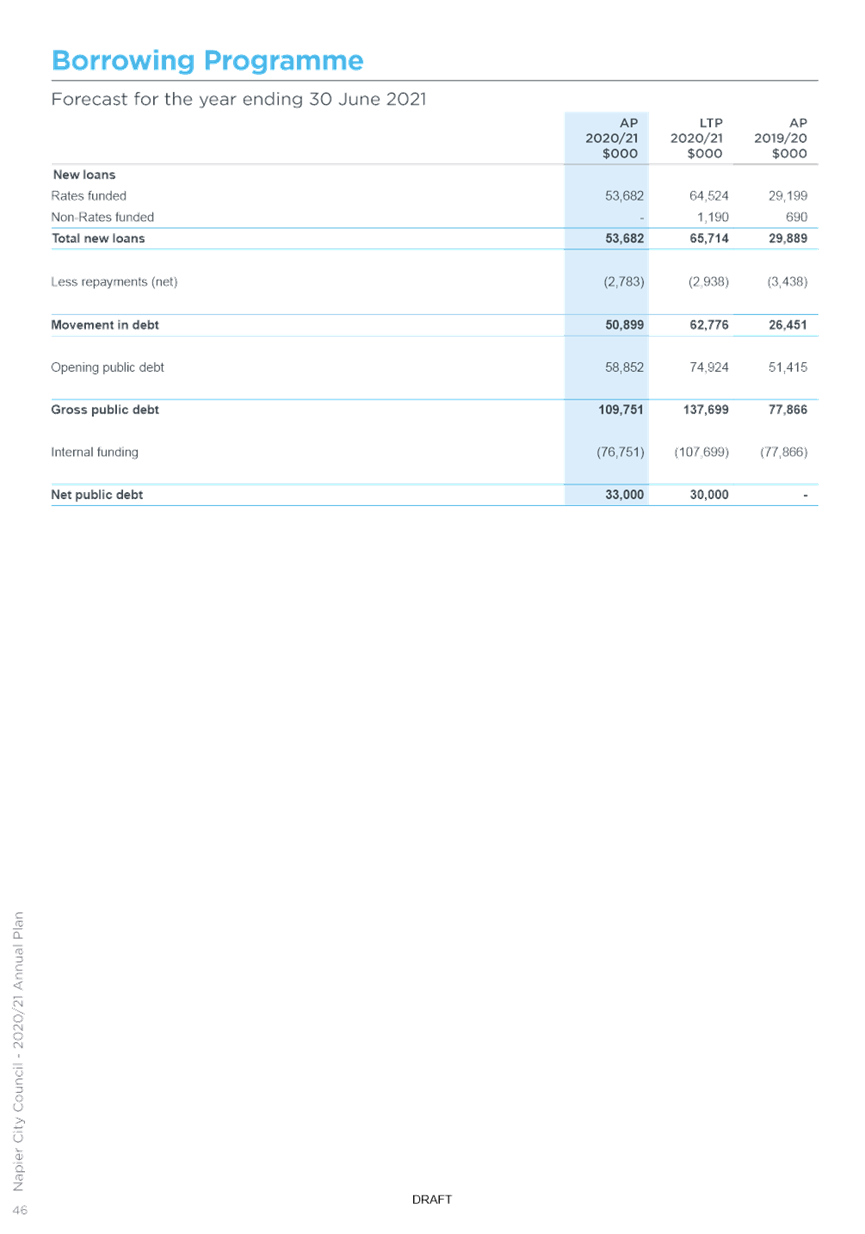

have a loan funding requirement of approximately $33 million for 20/21.

Officers explored options for external borrowing and Council set direction to

join the Local Government Funding Agency. To ensure that Council would be

able to meet the criteria of the Local Government Funding Agency if membership

was decided on, the Investment Policy and Liability Management Policy were

reviewed for compliance.

Council decisions to inform Annual Plan 2020/21

Since

the 10 March Council meeting where Council adopted the underlying material,

assumptions and key decisions to form the basis of the Annual Plan 2020/21,

Council has made several decisions related to the revised Annual Plan 2020/21.

Council reports and decisions include:

|

Meeting

|

Topic

|

Council report and decision

|

|

9

April Council meeting

|

Whakarire

Ave Revetment

|

Council received a report on Whakarire Ave including an update

on residents’ feedback and made the following decisions relevant to Annual

Plan 2020/21:

Ø to

proceed with the project,

Ø approve

the updated project cost estimate that now includes additional items,

including landscaping, stormwater conveyance and third party supervision and

to fund the additional cost from loans;

Ø approve

the private contribution to be held at the same amount as per the 2019/20

consultation, resulting in a change to the public/private split to 2.5%

private/95.5% public.

Whakaire Ave Revetment is an update in the Annual Plan 2020/21

Consultation Document. The Revenue and Financing Policy will be updated

prior to the targeted rate commencing.

|

|

9

April Council meeting

|

Library

Site Selection

|

Council received a report as an update on the Civic precinct

project including library site selection process and made the following

decisions relevant to Annual Plan 2020/21:

Ø accepted

in principle, the recommendation from the Library site project steering group

to pursue the development of the library on the Station Street Site.

Ø Noted

the Annual Plan 2020/21 will include the preferred site for the library and

any feedback received on this will be forward to the Civic Precinct Steering

Group for consideration in the masterplan development.

Napier Library Civic Precinct is an inform piece in the Annual

Plan 2020/21 Consultation Document.

|

|

20

April Audit and Risk Committee meeting

|

External

Accountability – investment and debt

Annual

Plan 20/21 underlying documents

|

The Committee received a report on External Accountability

– investment and debt which outlined that although Council is still in

a current cash position, Council will likely need to move into an external

debt position through the Annual Plan 2020/21, depending on timing of

projects. The Committee received the snapshot report on Council’s

Investment and Debt.

The Committee received a report on the underlying financial

information to the Annual Plan 2020/21. The Committee made the

following recommendations to Council relevant to the Annual Plan:

Ø Received

the underlying information including capital plan changes; 10 year revised

capital plan; financial information.

Ø Noted

that further review should be undertaken in light of Covid-19 impacts and the

full Council to be advised immediately of this review.

|

|

23

April Extraordinary Council meeting

|

Annual

Plan 2020/21 update

|

Council received a report on the suggested revised timelines for

the Annual Plan 2020/21 and made the following decisions:

Ø Note

that by deferring the release of the 2020/21 Annual Plan, Council will be in

breach of its legislative timelines under the Local Extraordinary Meeting of

Council - 23 April 2020 - Open Minutes 4 Government Act 2002 to adopt the

Annual Plan by 30 June in the year prior to the plan.

Ø Approve

the deferral of the release of the 2020/21 Annual Plan for community

consultation, and amendments to Financial Policies, until such time as the

most appropriate plan for the changed context of Covid-19 is developed and

agreed by Council.

Ø Note

Officers are working towards the draft Annual Plan 20/21 and consultation

document being brought to Council in June with community consultation to

occur after this.

Ø The

Hearing and adoption of the Annual Plan will be most likely in August.

|

|

30

April Extraordinary Council meeting

|

Annual

Plan proposed rate increase options

Rates

and debtors relief packages

Fees

and charges for 20/21

|

Annual Plan proposed rates increase options

Council received a report on the details of the financial

impacts of Covid-19 on the 2020/21 budget, with planning assumptions to guide

budgeting for 2021, and a shortlist of options to fund the operating

deficit. The report also sought Council approve for proposed rates

increase and to prepare the 2020/21 draft Annual Plan and consultation

document on the basis of the decisions made at the meeting. Council

made the following decisions:

Ø Note that a

number of briefing sessions/workshops have been held with elected members and

seek Councillor input and direction setting in relation to preparing the

final material required for the revised Annual Plan and consultation document

for the community.

Ø Note the

revised timeline that was provided to Council on 23 April, will see the

adoption of the Annual Plan later than the statutory deadline due to the

additional changes required for the revised plan and impact on the timeline

for consulting and hearings. The revised adoption date is currently set for

27 August.

Ø Note that

Covid-19 has had a material impact on Council’s budget for the current

year (2019/20), and is likely to put Council into a net operating rates

deficit when the final position is known in August (currently estimated at

$3m).

Ø Agree that

the 2020/21 Annual Plan and consultation document be prepared for

consideration by the Council, based on Option C, which recommends

i. A

4.80% average rates,

ii. Funding

of a planned operating gap of $6.74 million is allocated from Council

reserves, ($4 million from the Parking Reserve, and $2.74 million from the

Suburban and Urban Growth Fund.). Council will consult on the use of these

funds as part of the Annual Plan 2020/21.

iii. Note

that under section 80 of the Local Government Act 2002 Council could consider

internal borrowing for any rates or debtors relief applications received

prior to community consultation and adoption of the 2020/21 Annual Plan. If

community consultation confirms that it is appropriate to use the parking and

urban/suburban growth funds to fund the operating gap of $6.74m the internal

loan would be repaid from these reserves.

iv. Note

Council officers have identified operational savings of $3.7 million in the

development of the revised Covid-19 Annual Plan 20/21.

There are two options provided regarding how to pay for the

funding shortfall and achieve an average rates increase of 4.8% per

household. The proposed option is to use reserves to fund the operating gap

of $6.74m and the other option presented is to borrow to cover the operating

gap.

Rates

and debtors relief packages

Council

received a report on financial relief options for Council to consider in

response to financial stress in the community caused by Covid-19.

Council made the following decisions:

Ø Note that a

separate paper be bought back to Council with proposed changes to the Rates

Postponement Policy for consideration and community consultation alongside

the Annual Plan 20/21.

Ø Note that

Rates Postponement for 20/21 be considered under “Special Circumstances”

in the existing policy until such time the revised Rates Postponement Policy

is adopted by Council.

Ø Approve

funding of up to $525k to be funded from Reserves to support Rates

Postponement Policy requirements for 2020/21 (being up to 50% of rates being

deferred up to 6 months).

Ø Note

delegation to the Director Corporate Services, Chief Financial Officer, and