|

Hawke's Bay Museums Trust Half Year Financial Report to 31 December 2023 (Doc Id 1745438) |

Item 1 - Attachment 1 |

Prosperous Napier Committee

Open Agenda

|

Meeting Date: |

Thursday 28 March 2024 |

|

Time: |

Following Napier People and Places Committee |

|

Venue: |

Large Exhibition Hall |

|

|

Livestreamed via Council’s Facebook page |

|

Committee Members |

Chair: Councillor Crown Members: Mayor Wise, Deputy Mayor Brosnan, Councillors Boag, Browne, Chrystal, Greig, Mawson, McGrath, Price, Simpson, Tareha and Taylor (Deputy Chair) Ngā Mānukanuka o te Iwi representatives – Joe Tareha and Evelyn Ratima |

|

Officer Responsible |

Deputy Chief Executive / Executive Director Corporate Services |

|

Administration |

Governance Team |

|

|

Next Prosperous Napier Committee Meeting Thursday 2 May 2024 |

2022-2025 - TERMS OF REFERENCE - PROSPEROUS NAPIER COMMITTEE

|

Chairperson |

Councillor Crown |

|

Deputy Chairperson |

Councillor Tayor |

|

Membership |

Mayor and Councillors (13) Ngā Mānukanuka o te Iwi representatives (2) |

|

Quorum |

8 |

|

Meeting frequency |

At least 6 weekly (or as required) |

|

Officer Responsible |

Deputy Chief Executive / Executive Director Corporate Services |

Purpose

To provide governance oversight to the corporate business of the Council, monitor the Council’s financial position and financial performance against the Long Term Plan and Annual Plan, and to guide and monitor Council’s interests in any Council Controlled Organisations (CCOs), Council Organisations (COs) and subsidiaries.

Delegated Powers to Act

To exercise and perform Council’s functions, powers and duties within its area of responsibility, excluding those matters reserved to Council by law or by resolution of Council, specifically including the following:

1. To monitor the overall financial position of Council and its monthly performance against the Annual Plan and Long Term Plan.

2. To adopt or amend policies or strategies related to the Committee's area of responsibility, provided the new or amended policy does not conflict with an existing policy or strategy.

3. To consider all matters relating to CCOs and COs, not reserved to Council, including to monitoring the overall performance of CCO’s.

4. Provide governance to Council’s property operations and consider related policy.

5. Consider applications for the sale of properties within the Leasehold Land Portfolio.

6. To resolve any other matters which fall outside the area of responsibility of all Standing Committees, but where the Mayor in consultation with the Chief Executive considers it desirable that the matter is considered by a Standing Committee in the first instance.

Power to Recommend

The Committee may recommend to Council and/or any standing committee as it deems appropriate.

The Committee may recommend to Council and/or the Chief Executive any changes to the funding or rating system for the City, any variation to budgets that are outside the delegated powers of officers and the approval of Statements of Intent for CCOs and COs each year.

To bring to the attention of Council and/or the Chief Executive any matters that the Committee believes are of relevance to the consideration of the financial performance or the delivery of strategic outcomes of Council.

The Committee must make a recommendation to Council or the Chief Executive if the decision considered appropriate is not consistent with, or is contrary to any policy (including the Annual Plan or Long Term Plan) established by the Council.

ORDER OF BUSINESS

Karakia

Apologies

Nil

Conflicts of interest

Public forum

Nil

Announcements by the Mayor

Announcements by the Chairperson including notification of minor matters not on the agenda

Note: re minor matters only - refer LGOIMA s46A(7A) and Standing Orders s9.13

A meeting may discuss an item that is not on the agenda only if it is a minor matter relating to the general business of the meeting and the Chairperson explains at the beginning of the public part of the meeting that the item will be discussed. However, the meeting may not make a resolution, decision or recommendation about the item, except to refer it to a subsequent meeting for further discussion.

Announcements by the management

Confirmation of minutes

That the Minutes of the Prosperous Napier Committee meeting held on Thursday, 8 February 2024 be taken as a true and accurate record of the meeting............................................................................... 74

Agenda items

1 Hawke's Bay Museums Trust Draft Statement of Intent and Financial Reporting............. 4

2 Cyclone Gabrielle Category 3 Voluntary Buy-Out Progress Update............................... 34

3 Street Naming - Mission Hills........................................................................................ 52

4 Procurement planning reporting.................................................................................... 57

5 Treasury Activity and Funding Update........................................................................... 59

6 Financial Forecast to 30 June 2024.............................................................................. 62

Minor matters not on the agenda – discussion (if any)

Recommendation to Exclude the Public................................................................. 73

Agenda Items

1. Hawke's Bay Museums Trust Draft Statement of Intent and Financial Reporting

|

Type of Report: |

Operational |

|

Legal Reference: |

Local Government Act 2002 |

|

Document ID: |

1744727 |

|

Reporting Officer/s & Unit: |

Caroline Thomson, Chief Financial Officer |

1.1 Purpose of Report

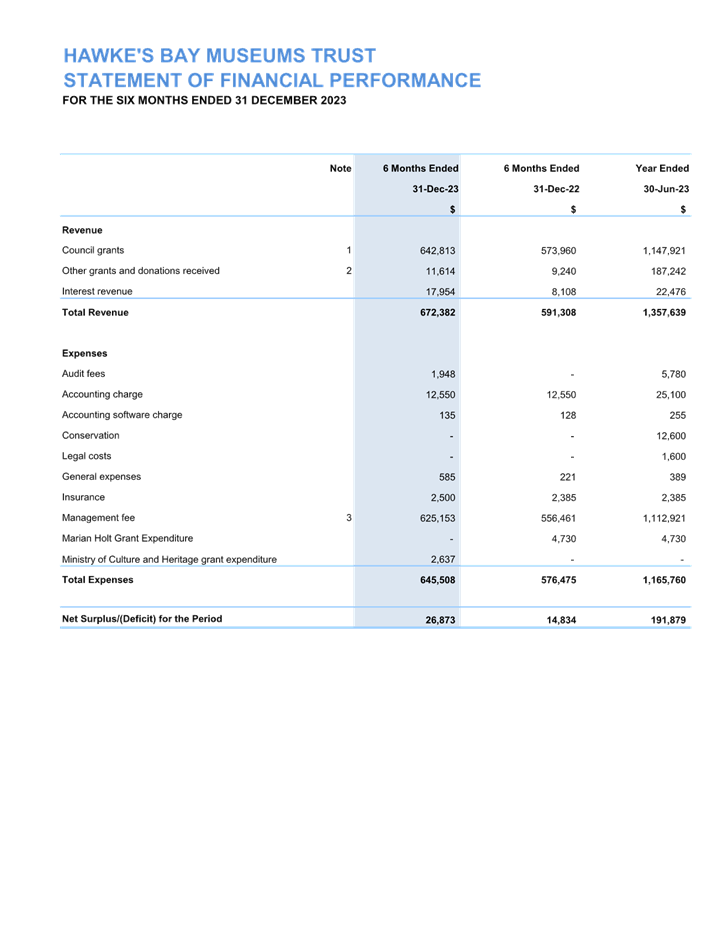

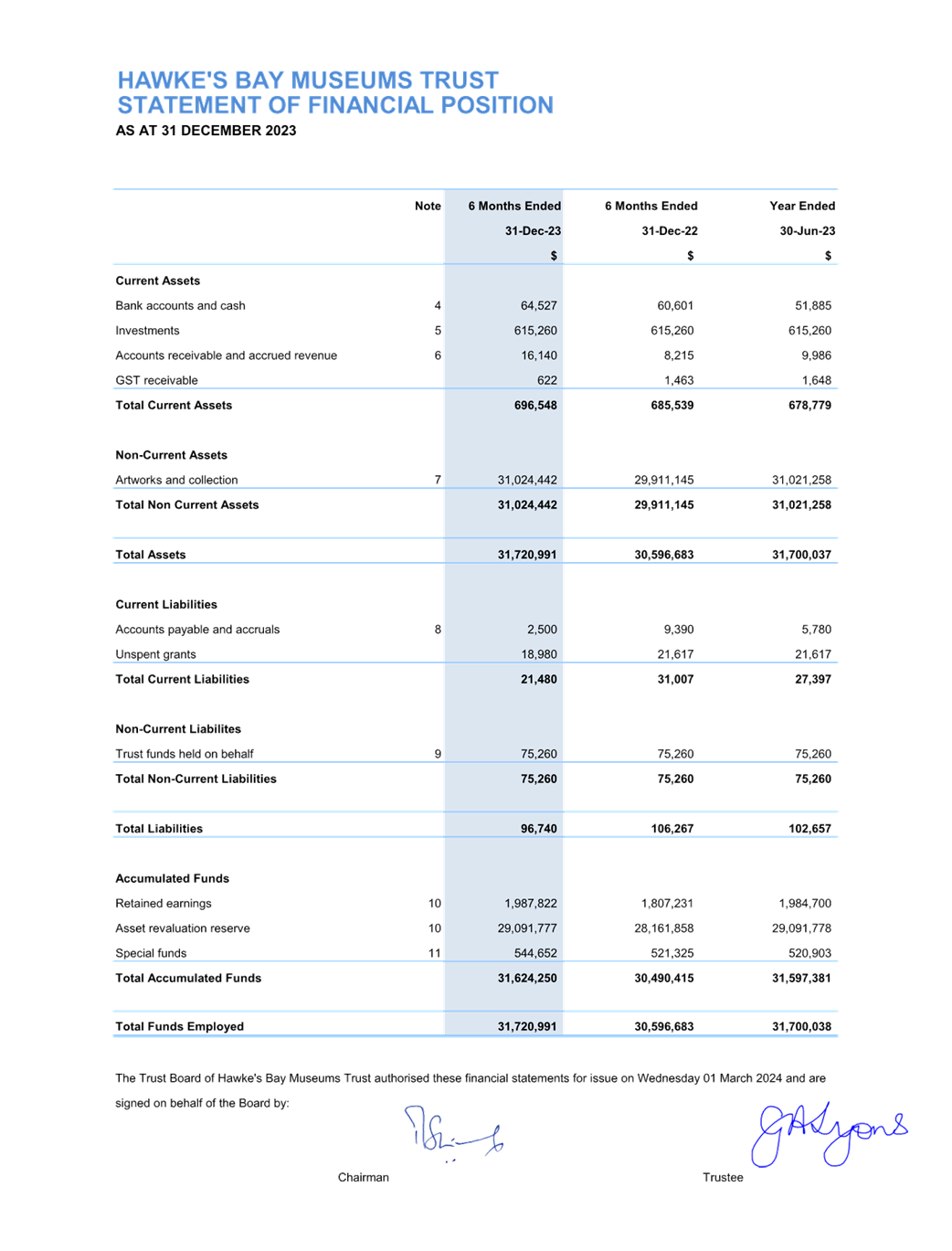

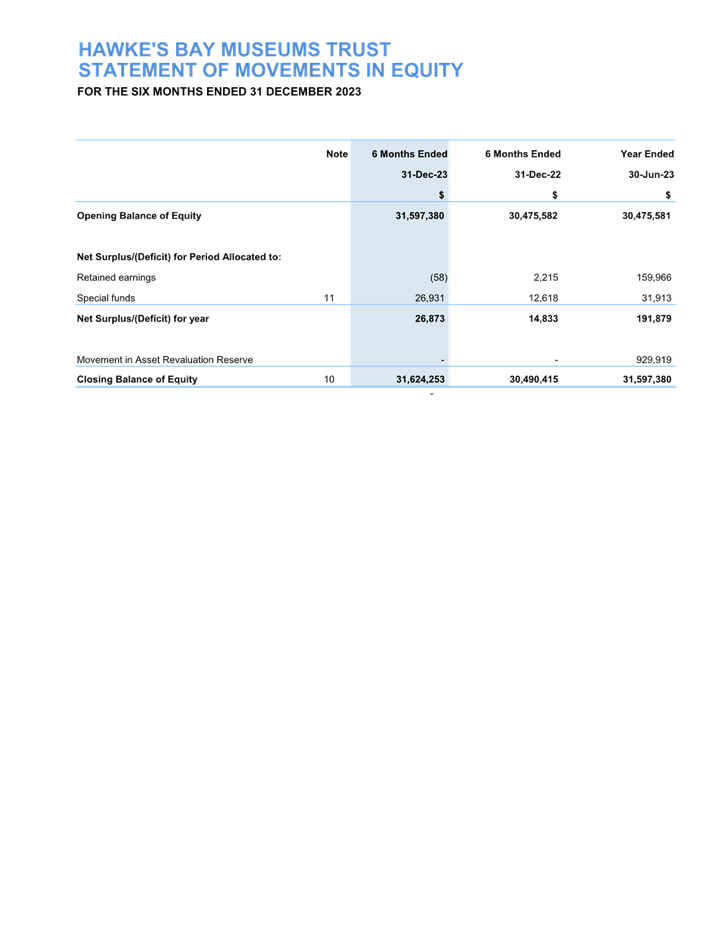

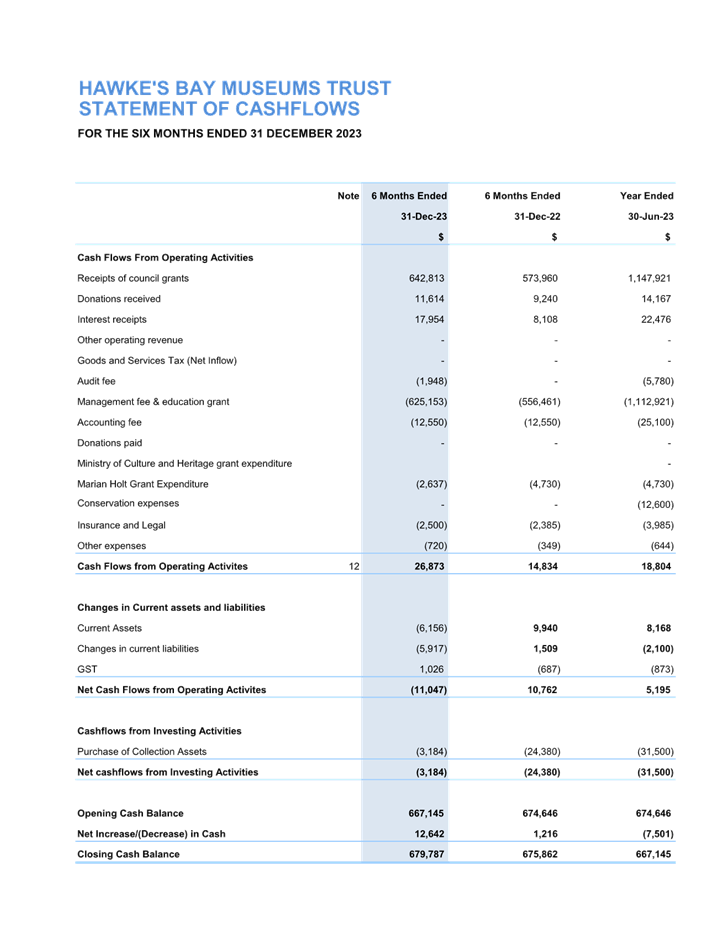

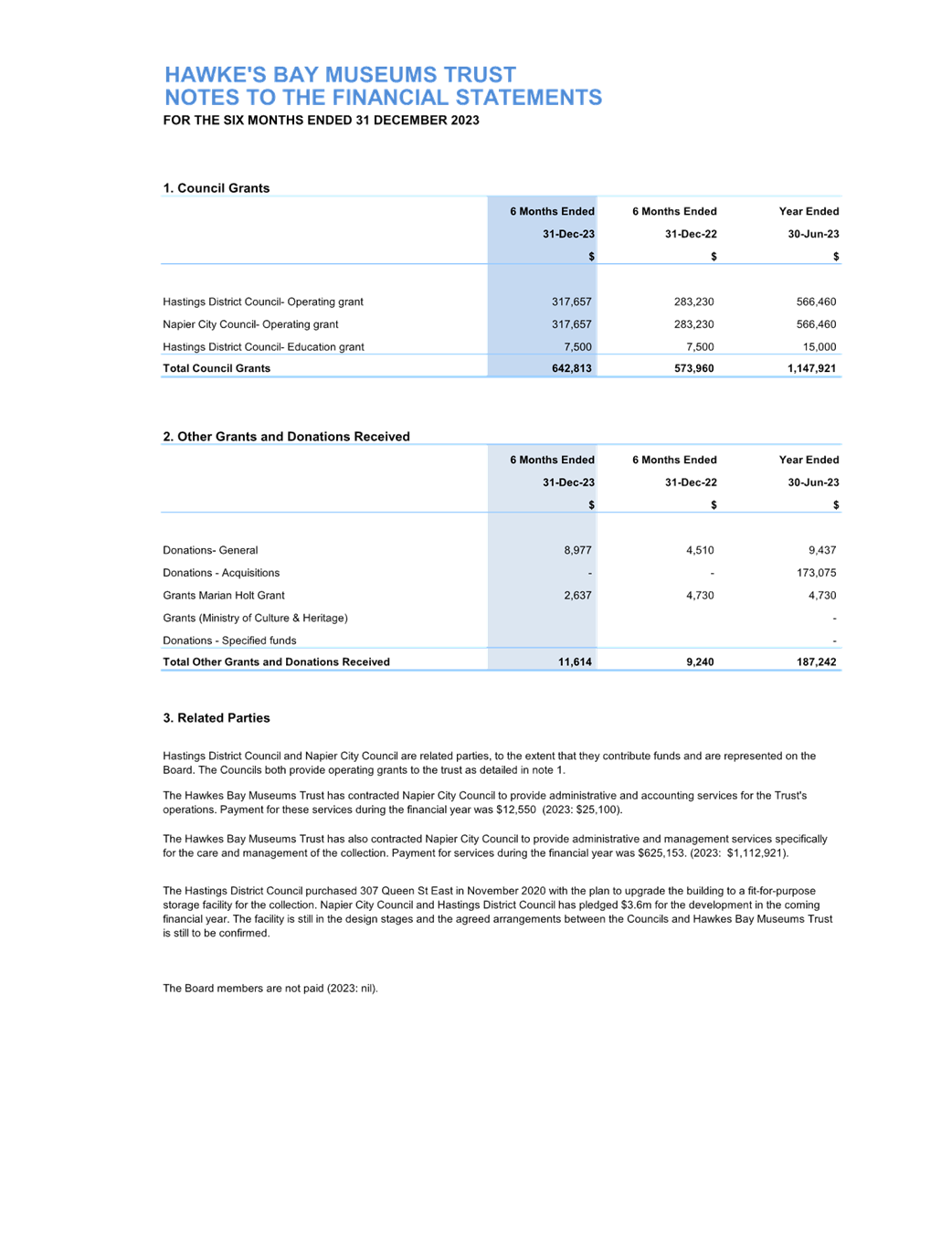

To receive the Hawke’s Bay Museums Trust Financial Report for the six months ended 31 December 2023 and draft Statement of Intent 2025-2027.

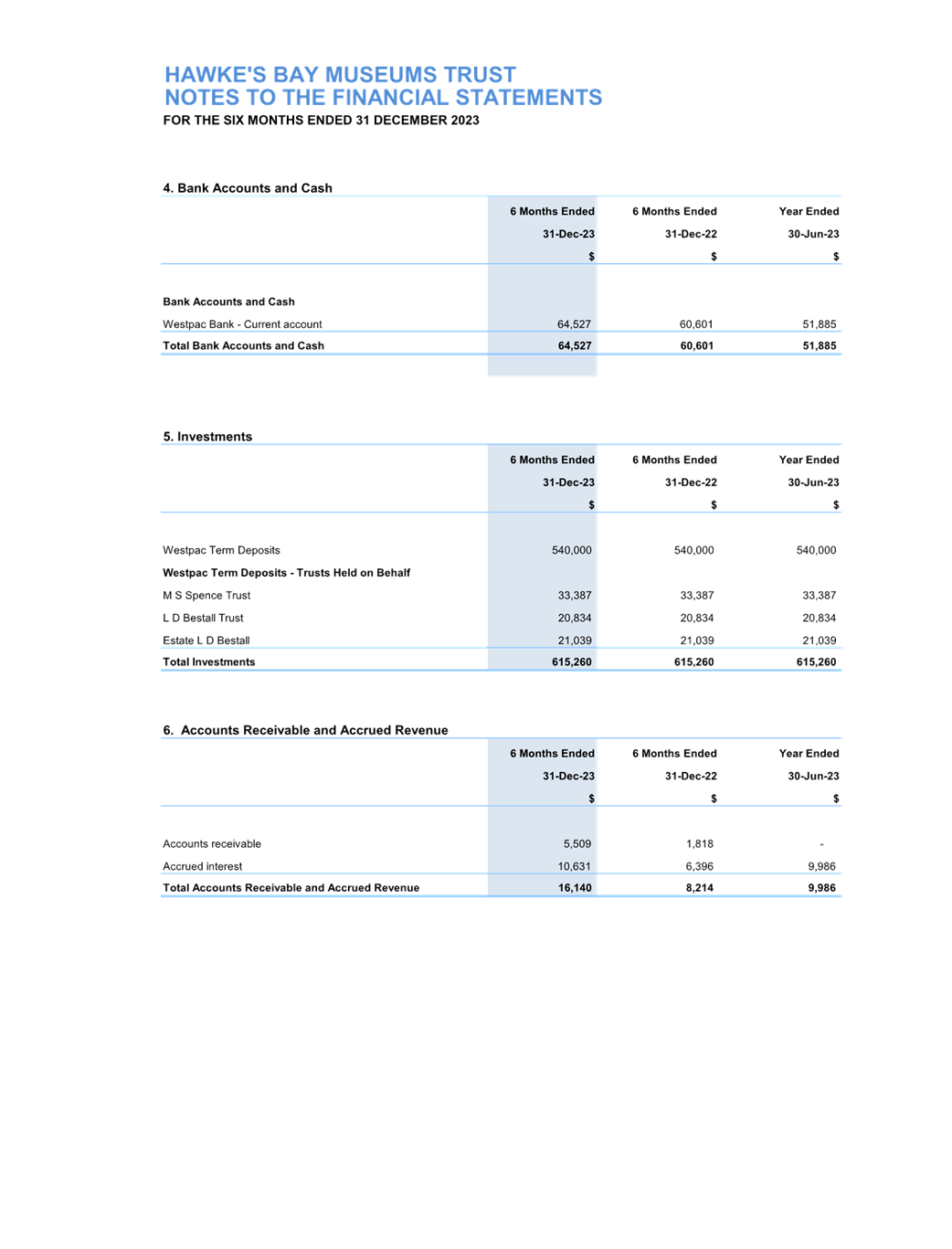

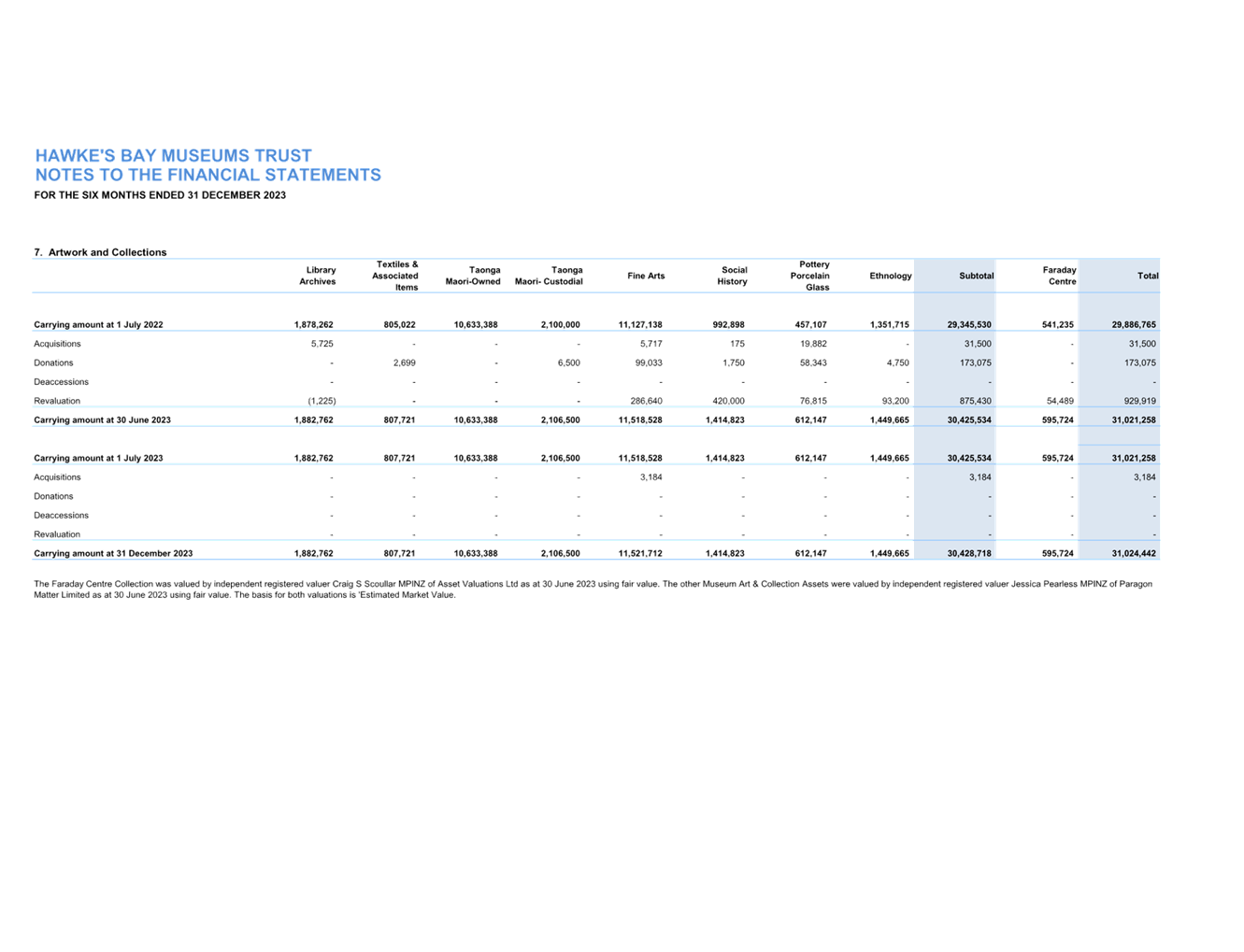

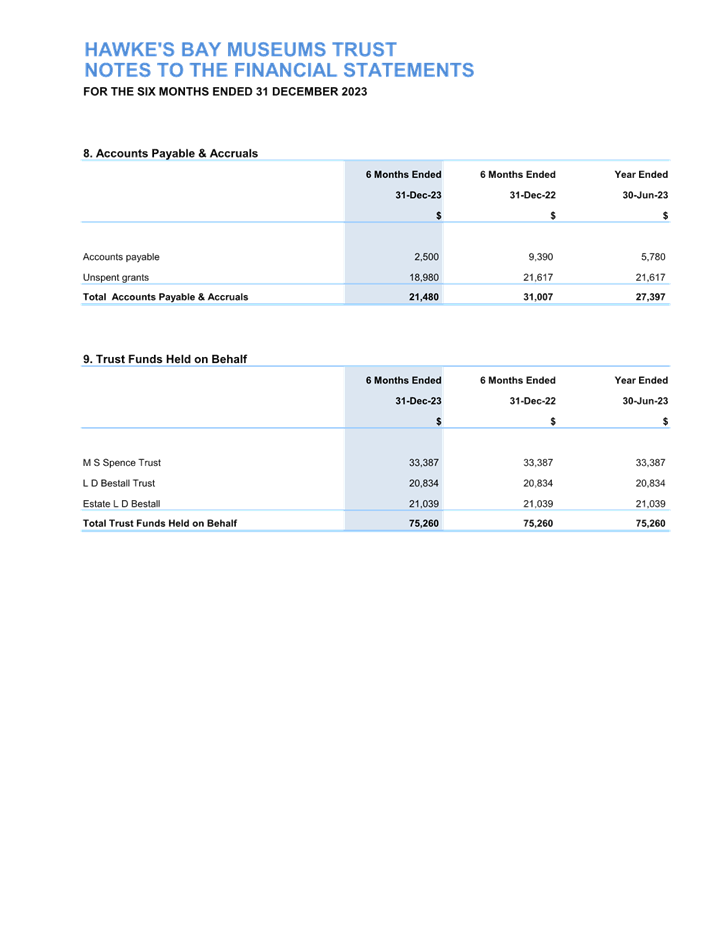

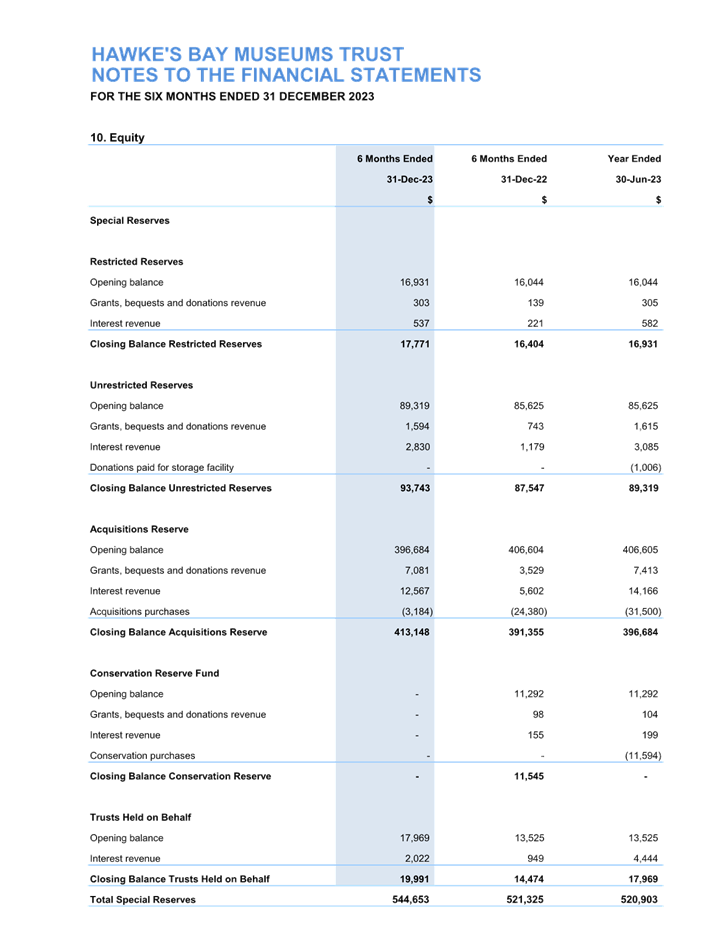

At the meeting of the Hawke’s Bay Museums Trust held on 1 March 2024, the Trustees adopted their Financial Report for the six months ended 31 December 2023. A copy is attached to this report for Council’s information.

The Trustees also accepted the attached draft Statement of Intent 2025-2027 at their meeting on 1 March 2024. This has been provided to Council for review and feedback to the Trust.

1.3 Issues

Draft Statement of Intent

The draft 2023/24 Statement of Intent contains the following performance indicators and targets for the key result areas:

· Protection – including storage, security and records management

· Quality – including conservation, accessioning and de-accessioning.

· Access – including ensuring the collection is available for exhibitions, research and archives; and

· Development – including fundraising, reserves management, and stakeholder relations

Joint Working Group

The Napier City Council continues to participate in a Joint Working Group with Hastings District Council that is considering the future structure of the Hawke’s Bay Museums Trust, its funding, the storage of the collection, and the role of the MTG Hawke’s Bay in the display of the collection.

1.4 Significance and Engagement

The draft Statement of Intent has been assessed under the Council’s Significance and Engagement Policy as being of low significance.

1.5 Implications

Financial

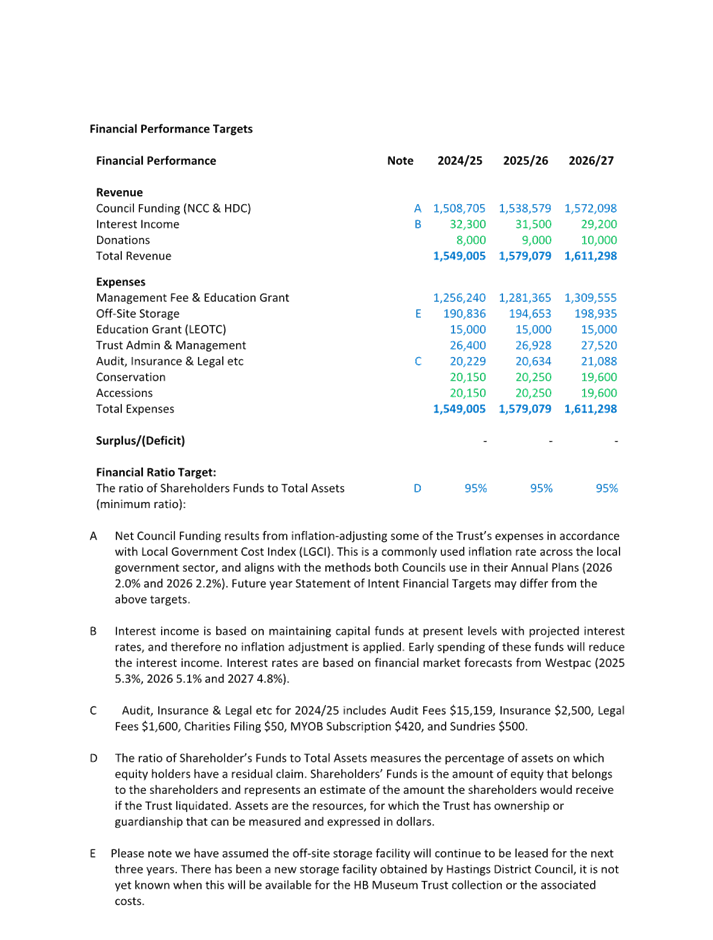

Council makes a financial contribution to the Trust which is detailed in the attached draft Statement of Intent.

Social & Policy

The Hawke’s Bay Museum collection includes significant taonga and in acknowledging the significance of that collection, one of the Trustees to the Trust is appointed by Ngāti Kahungunu Iwi.

Risk

This report is to receive the Hawke’s Bay Museums Trust draft Statement of Intent 2025-2027 and therefore poses little risk to Council.

1.6 Preferred Options

The options available to Council are as follows:

a. Receive the Financial Report for the six months ended 31 December 2023.

b. Receive the Hawke’s Bay Museums Trust draft Statement of Intent 2025-2027 and provide any feedback to the Trust prior to the Statement of Intent being brought back to Council for adoption.

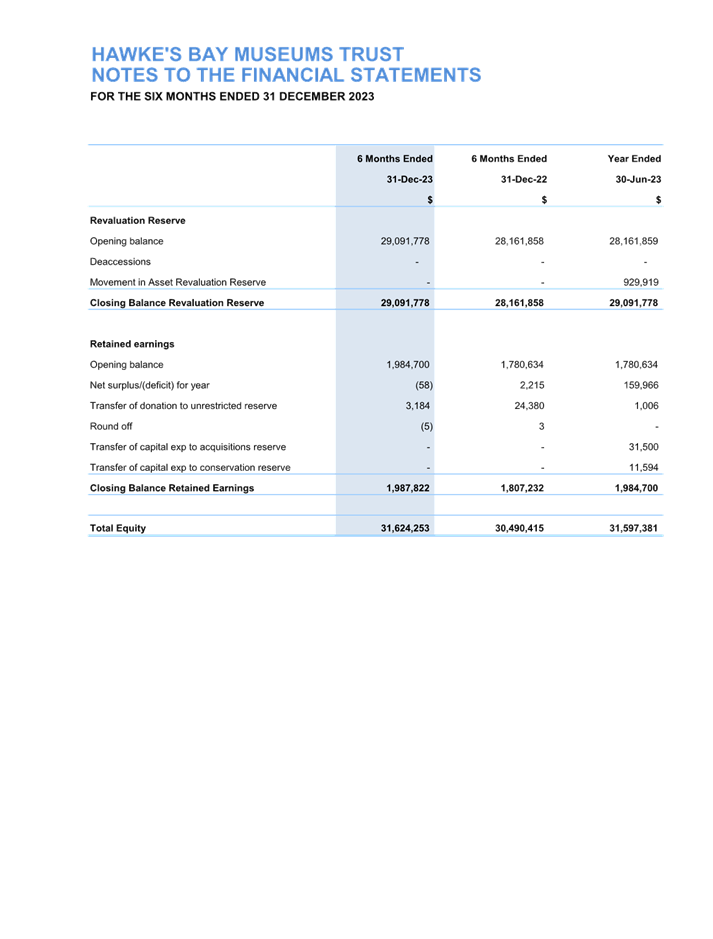

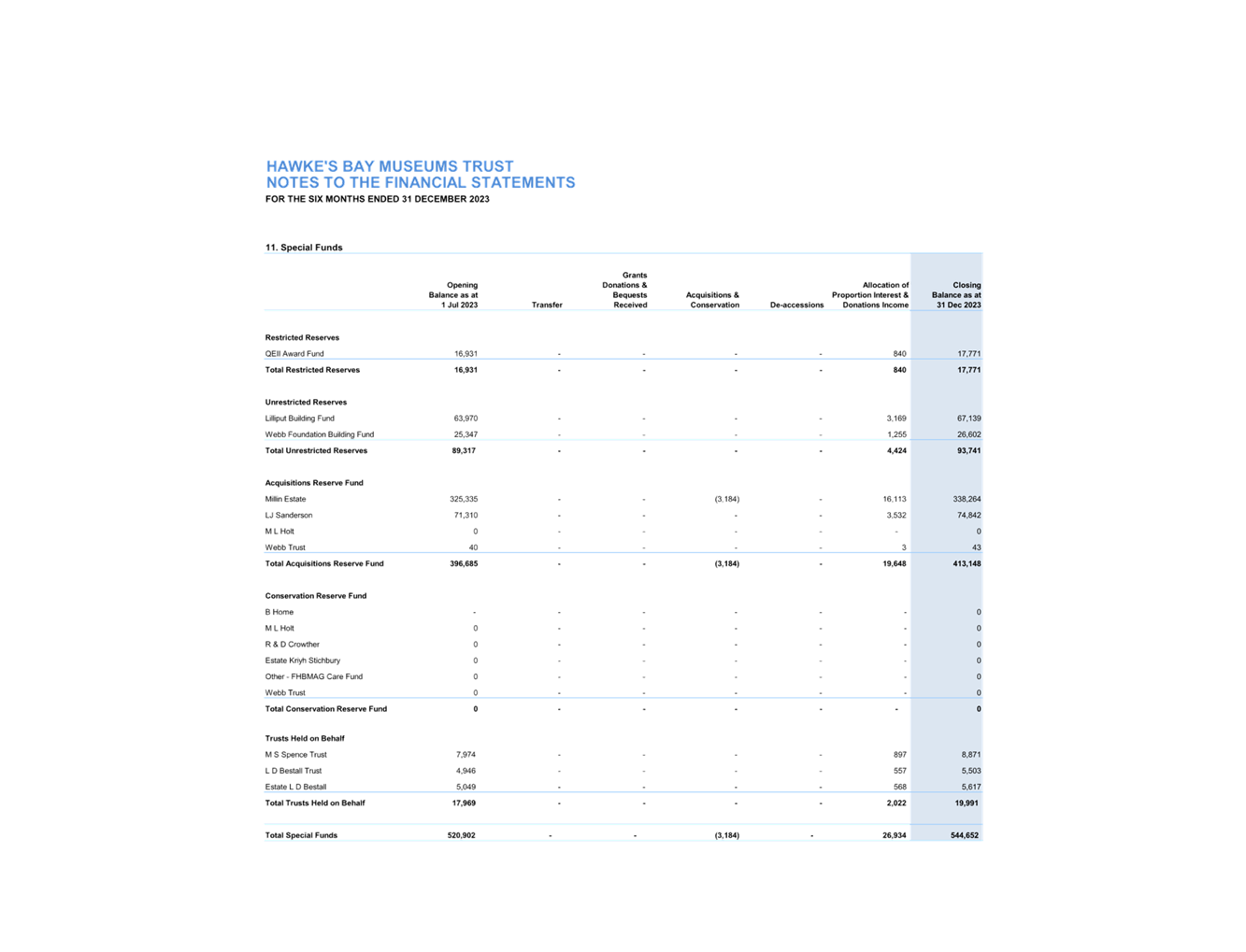

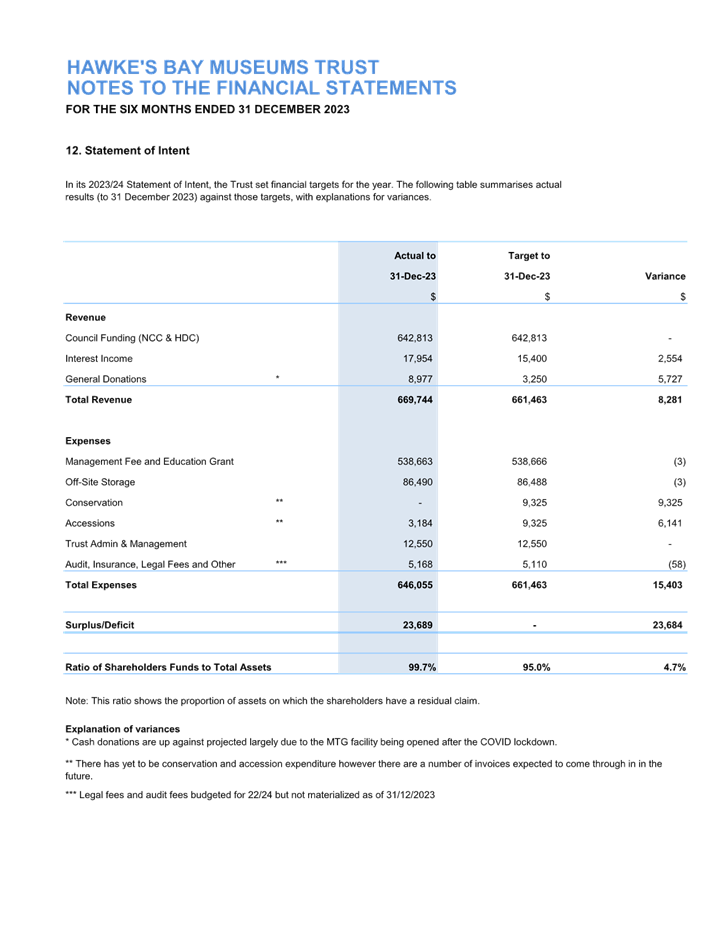

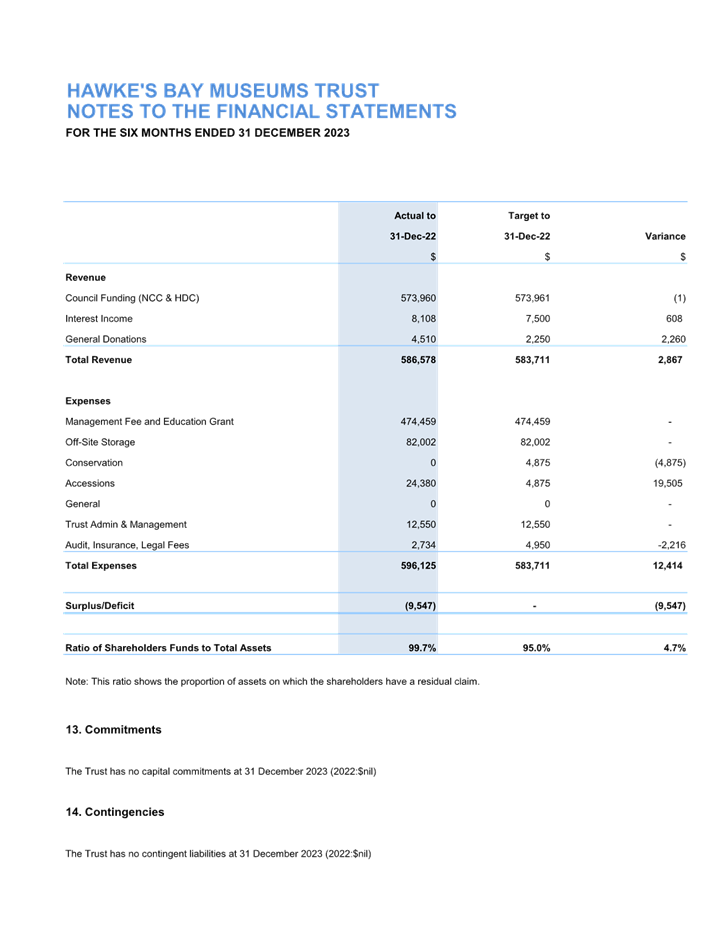

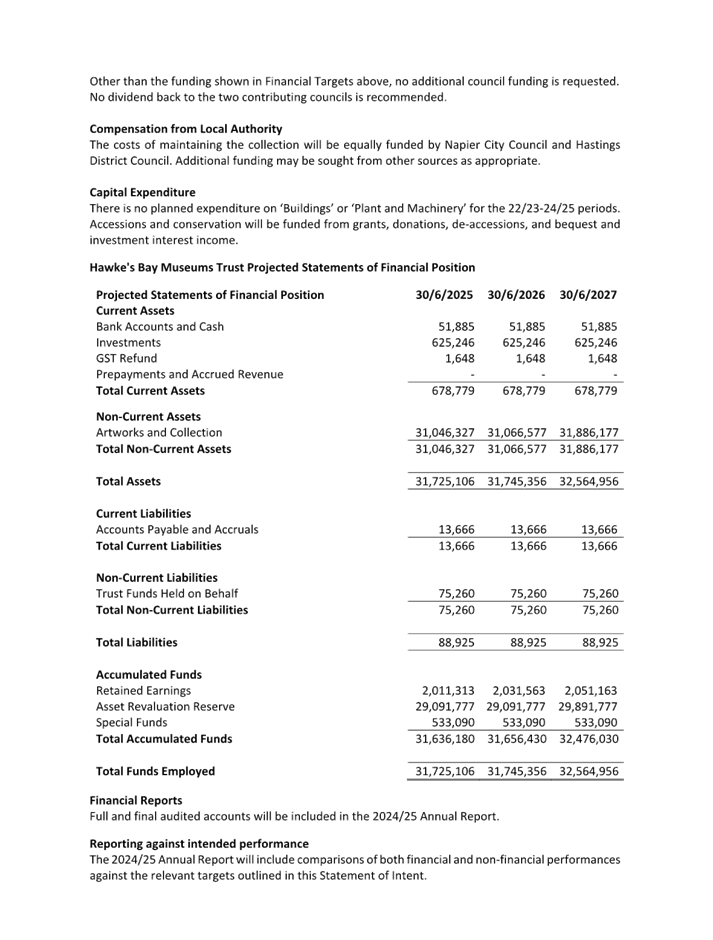

1 Hawke's Bay Museums Trust Half Year Financial Report to 31 December 2023 (Doc Id 1745438)

2 Hawke's Bay Museums Trust Draft Statement of Intent 2025-2027 (Doc Id 1745437)

|

Hawke's Bay Museums Trust Half Year Financial Report to 31 December 2023 (Doc Id 1745438) |

Item 1 - Attachment 1 |

|

Hawke's Bay Museums Trust Draft Statement of Intent 2025-2027 (Doc Id 1745437) |

Item 1 - Attachment 2 |

2. Cyclone Gabrielle Category 3 Voluntary Buy-Out Progress Update

|

Type of Report: |

Operational |

|

Legal Reference: |

Local Government Act 2002 |

|

Document ID: |

1738388 |

|

Reporting Officer/s & Unit: |

Richard Munneke, Commercial Director Anne Bradbury, Manager Community Strategies |

2.1 Purpose of Report

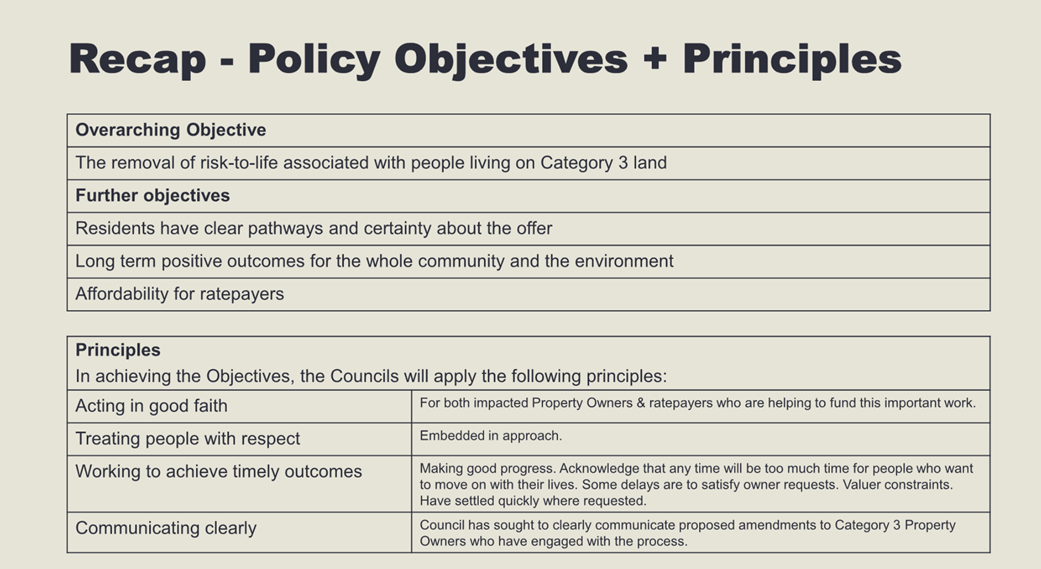

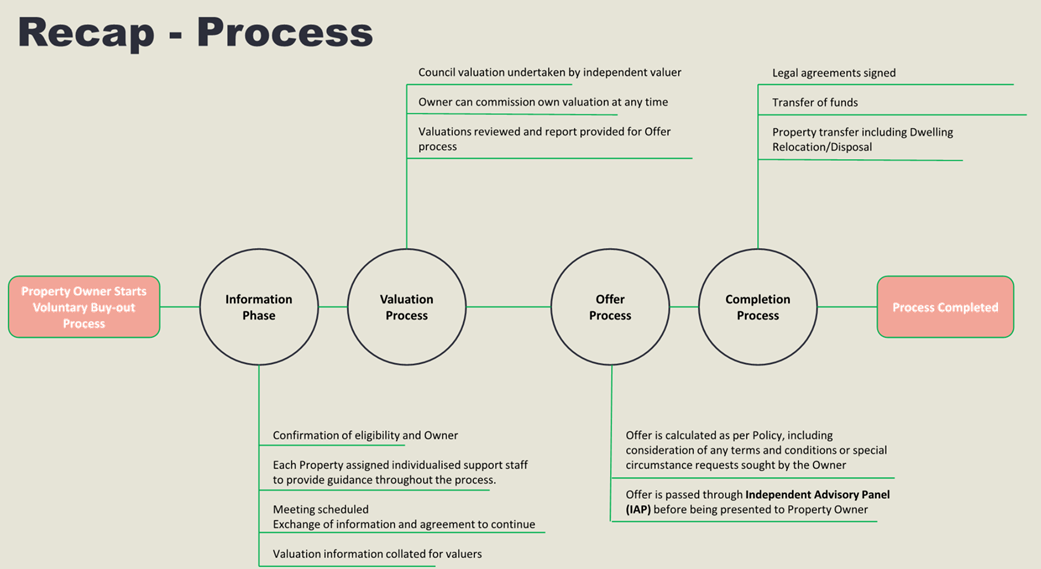

The purpose of this report is to update Council on the progress made by Napier City Council (NCC) and Hastings District Council (HDC) with the category 3 voluntary buyout activity and report the current financial status of the buyout within the crown funding cap.

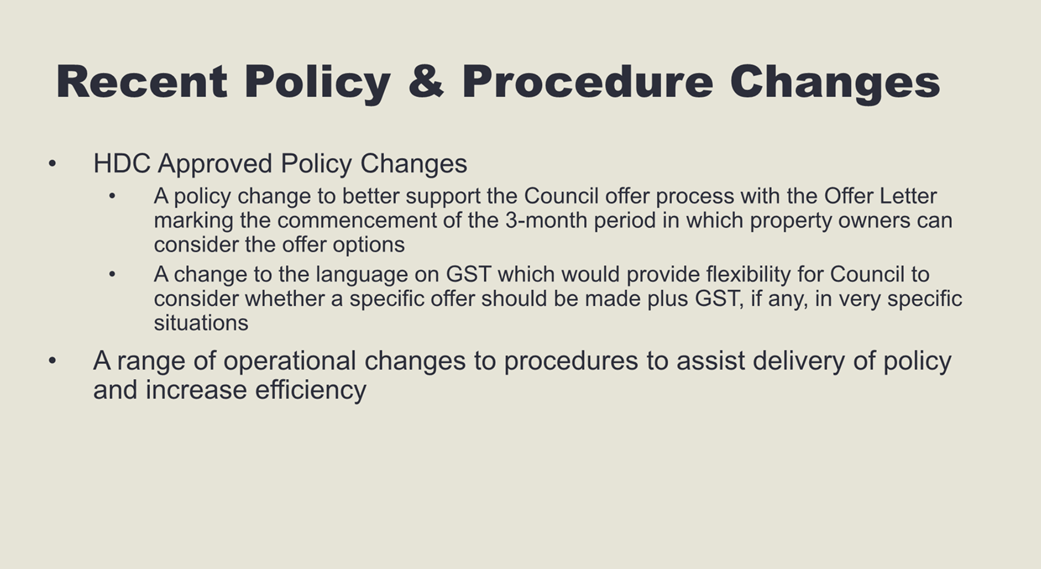

The report also seeks to obtain Council approval to make minor policy changes to the Category 3 Voluntary Buyout Policy being:

1) a change to better support the Council offer process with the Offer letter marking the commencement of the 3-month period in which property owners can consider the offer options; and

2) a change to the language on GST which would provide flexibility for Council to consider whether a specific offer should be made plus GST, if any, in very specific situations.

Note: These changes have already been adopted by Hastings District Council

After the Region’s Councils entered into a formal agreement with the Crown for Cyclone Gabrielle recovery, HDC and NCC have been progressing the Category 3 Voluntary Residential Buyout

Joint Approach

The Councils have geared their implementation of the Voluntary Buyout programme through a joint policy framework and a single Voluntary Buyout Office (VBO) which is located and run by HDC. NCC contract to HDC for delivery through the VBO because proportionally Napier has far less Category 3 properties than HDC.

In addition, the affected community (Esk Valley) traverses both Councils boundaries which mean a consistent approach to delivery is imperative. The result has been an efficient and uniform delivery of the policy allowing the Councils to progress offers to affected residents through a single VBO.

Funding Implications

As stated above prior to the roll out of the Category 3 Residential Buyout Programme a funding agreement was reached with the government. A budget and funding cap was set by the Government based on assumptions such as the overall insurance level being 70% of the pre-cyclone overall value for example.

Now that actual costs are available both Councils are able to establish how they are tracking against the budget and can forecast with more accuracy. At this stage NCC is within the cap set, however because it has a small number of properties affected (14) it may only take one property to be under-insured to tip the scales.

Changes to the joint Category 3 Buy Out Policy

After implementing the policy for some months, two minor policy changes are also proposed to improve the process:

1) A change to better support the Council offer process. Once the valuation part of the process is complete an offer letter is constructed that includes:

· the outcome of the valuation/s;

· any considerations worth noting from the initial meeting with property owners; and

· the calculated offer options that are available to the property owner. This letter, rather than a full sale and purchase agreement (as noted in the Policy), is presented to the owners at this point and we are recommending that this mark the commencement of the 3-month period in which property owners can consider the offer options. This minor policy change would facilitate a more efficient offer process.

2) A change to the language on GST. This would provide flexibility for Council to consider whether a specific offer should be made plus GST, if any, in very specific situations, while considering the policy objective of affordability for ratepayers

2.3 Issues

Category 3 Buy-out Policy amendments

A) Improving the clarity of the 3 month period

There will be no real impact for property owners if the Policy is amended to reflect that the Offer letter, rather than provision of the full sale and purchase agreement, marks the commencement of the 3-month period in which property owners can consider the offer options. This minor policy change would facilitate a more efficient offer process.

B) GST

In terms of the proposed change to the language relating to GST, we sought GST advice from PWC. This followed questions raised around GST practice for valuations. The PWC advice noted the following:

“We are satisfied with the Policy stating that the offer will include GST. This reflects that Council will be wanting to cap the price being paid. It will not alter the approach taken for the valuations, nor does it determine or have any bearing on the final GST treatment.”

4.6 The PWC advice, however, noted that they would anticipate that the current clause 4.12 of the Policy could create challenges in the situations outlined below. The proposed amendment to the GST language in the Policy would provide the VBO the flexibility to deal with these specific situations:

“Where the property owner was GST registered and used the property for making taxable supplies. In this case, the property is likely to have been valued as “$ plus GST if any” and it would be up to Council to consider uplifting this or using the valuation provided, i.e. whether it is, say, $100k or $115k inclusive of GST, as the transaction will be subject to Compulsory Zero-rating (CZR). - Where the property is mixed use or requires the deemed separate supply rule to apply. In these cases, we recommend that specific advice is sought.”

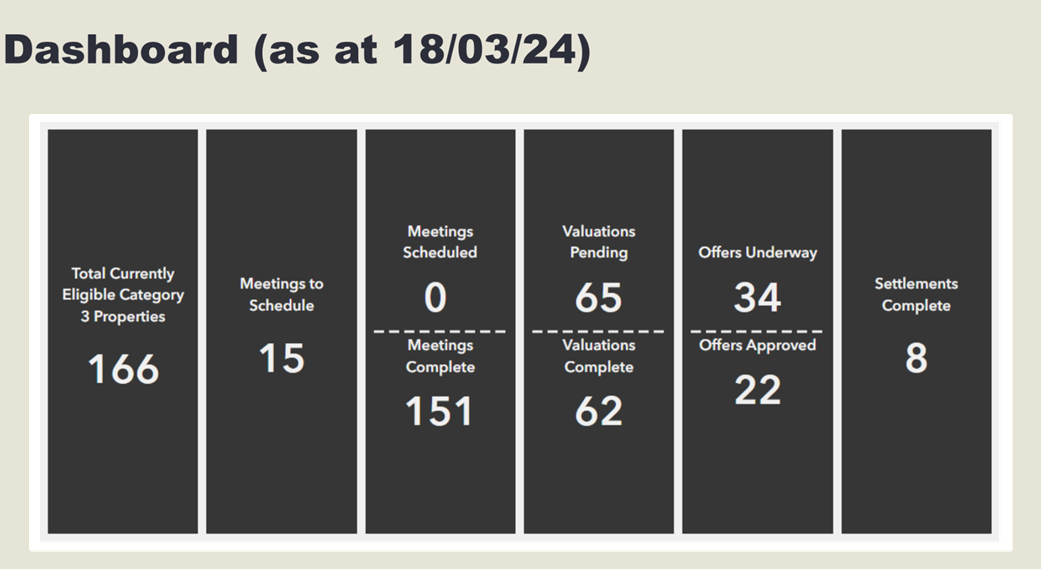

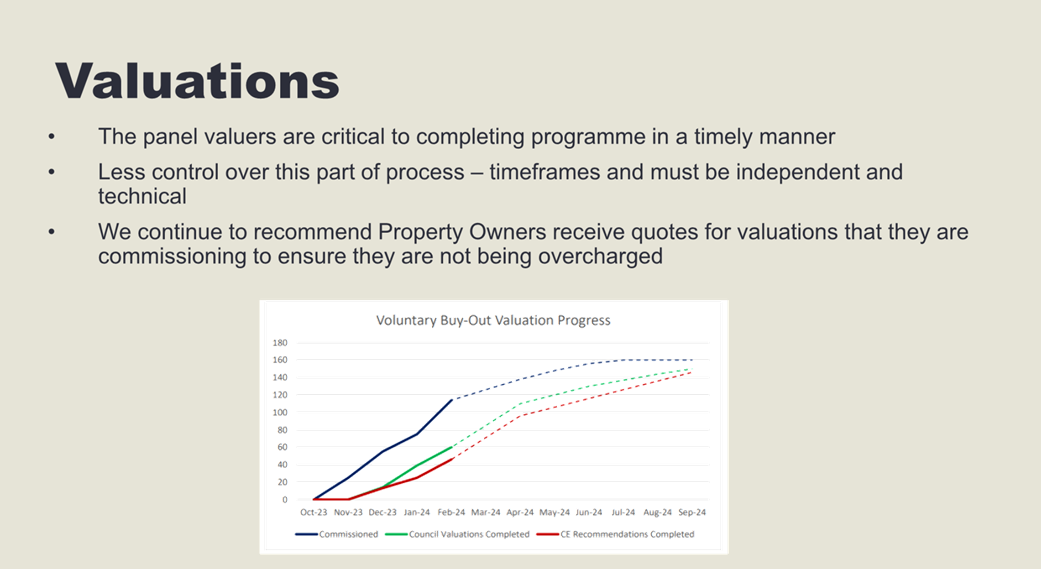

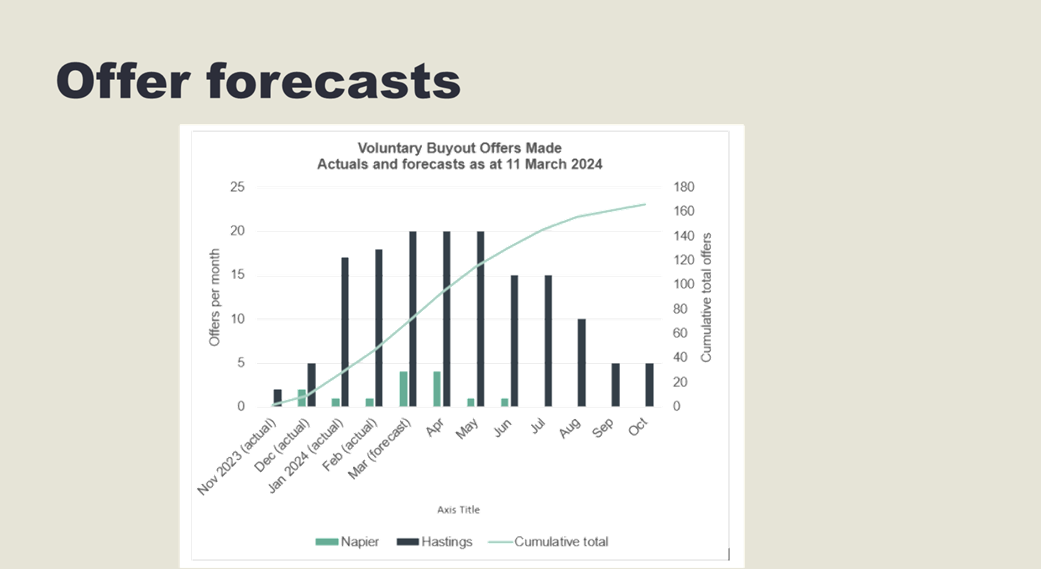

Progress and reporting on Category 3 Buyout

HDC and NCC hold a quarterly progress meeting with Crown Infrastructure Partners and Cyclone Recovery Unit Officials. Such a meeting was held on Tuesday 12 March 2024 to report back on the Hawke’s Bay Funding Agreement programme. A précis of the Councils reporting is included in Attachment 1.

This provides a useful overview of progress and financial performance of the voluntary buyout activity.

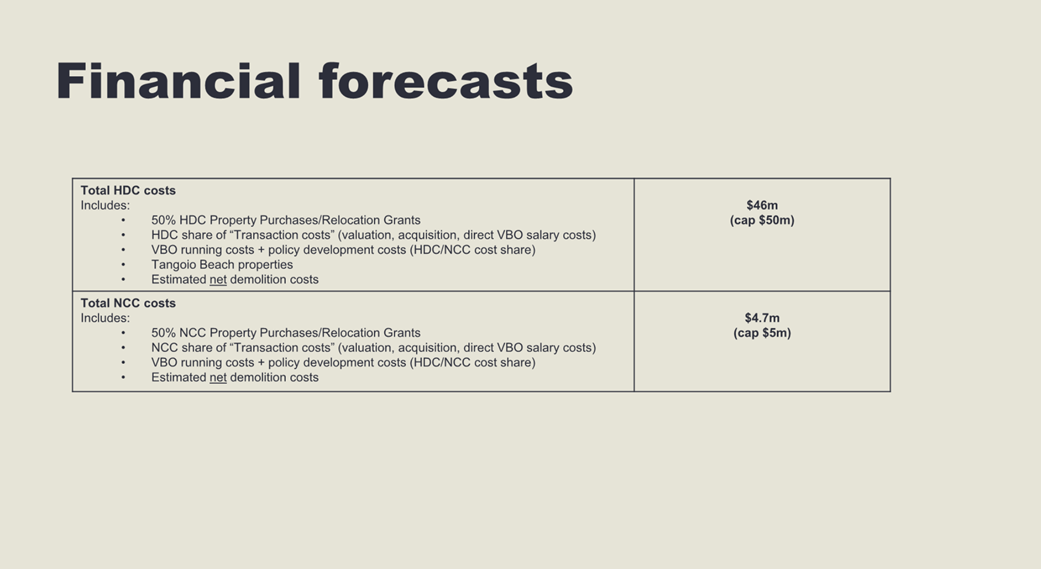

Financial

At the outset based on assumptions, NCC budgeted $4m in costs for the category 3 buyout with $1m contingency. Combined the $5m is represented in the Crown agreement and is eligible for a 50% crown subsidy.

Projections based on costs to date indicate that the activity will cost $4.7m at completion.

These costs are made up of:

· 50% NCC Property purchases/ relocation grants

· NCC share of “transaction costs”

· VBO running costs + policy development costs (cost share)

· Estimated net demolition costs

Risk

Whilst the activity is projected to expend $4.725m which is within the $5m cap for which a 50% subsidy is available from the Government as per the agreement with the Crown it should be noted that:

1) NCC has only 14 properties in Category, with incomplete data around insurance levels and values/cost of future offers.

2) The small sample size means that financial projections can potentially be significantly underestimated by a single property being under insured. This may mean that the $5 cap is at risk of being breached when true costs are identified.

2.4 Options

The options available to Council are as follows:

a) Receive the report and approve amendment to the Category 3 Buy-out Policy

b) Not receive the report and not approve amendments to the Category 3 Buy-out Policy

3. Street Naming - Mission Hills

|

Type of Report: |

Procedural |

|

Legal Reference: |

N/A |

|

Document ID: |

1745256 |

|

Reporting Officer/s & Unit: |

Nick McCool, Principal Resource Consents Planner |

3.1 Purpose of Report

To obtain Council approval for new street names for Stage 1 of the Mission Hills Residential Subdivision Development.

1.2 Background Summary

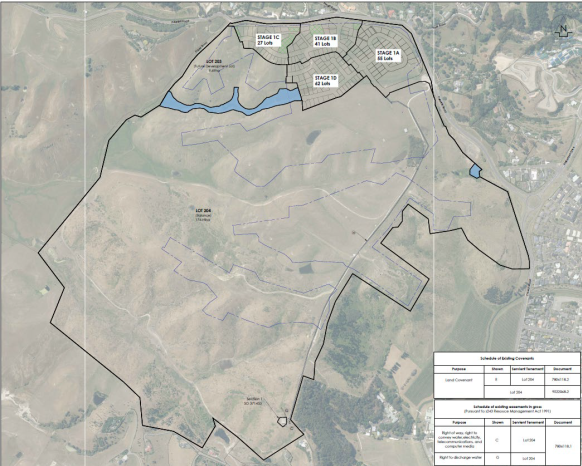

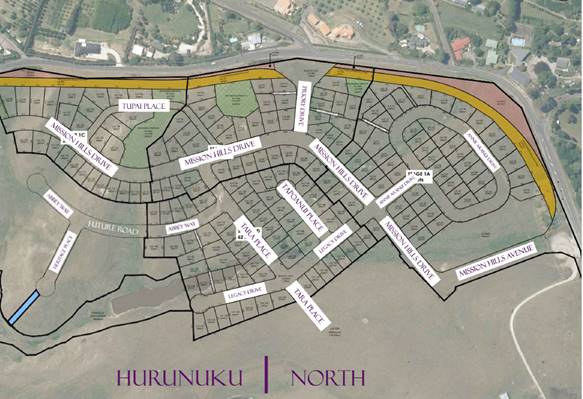

On 3 July 2023 Council granted subdivision consent to Emerald Hills Joint Venture Limited (EHJV) which authorised the creation of 184 residential lots in the northern extent of the Structure Plan area of Lot 2 DP 559656 at 231 Puketitiri Road, Napier.

Road, Local Purpose Reserve(s), Local Purpose (Stormwater) Reserve(s) are to be vested in Council. Figure 1 shows the overall location of Stage 1 within the wider Mission Special Character Zone. Figure 2 shows Stage 1. Figure 3 shows the location of the proposed roads and their names.

Figure 1: Location Plan – Stage 1, Mission Special Character Zone

Figure 2: Stage 1, Mission Hills Residential Subdivision Development

Figure 3: Location of the roads and their proposed names

1.3 Significance and Engagement

The letter dated 11 January 2024 from Alan Martin-Smith, Regional Manager, Cheal states “The final street names have been defined using recent history with the land being formerly part of the “Mission Estate”, as well as in conjunction with extensive consultation with Taiwhenua Te Whanganui Orutu and Mana Ahuriri. As part of this consultation, a number of the proposed names have been promoted and endorsed by both Taiwhenua Te Whanganui Orutu and Mana Ahuriri.”

Meaning behind proposed road names:

“MISSION HILLS AVENUE and DRIVE

A strong and logical name linking the Mission Hills development to the main entry and ridge roads.

ANNIE ARANUI DRIVE

Mana Wahine whakapapa across Ahuriri Hapu supported whanau over a number of years, worked through plan Mission development mitigation strategy at start of korero. Regional Commissioner Ministry of Social Development initiated and implemented social response across the East Coast Region and Nationally for community and made a positive difference in whanau/community lives.

LEGACY DRIVE

‘Legacy’ is used in our Mission Hills logo as we believe the development represents not only the enormous legacy of the Mission Monastery and the local Iwi, however also the four developers who have enabled Mission Hills through their combined vision and expertise.

TAPOANUI PLACE

Tapoanui is the surname of Mahu (reflects Ngati Mahu/Hapu local area). Mahu was in Hawke’s Bay before migration and has a strong whakapapa throughout the region.

TUPAI PLACE

Tupai identifies with place of learning and will provide a link in the future with reserve sites. Tupai was a High Priest and his responsibility lay on the land also the school of learning.

ABBEY WAY

A nod to the significance of the Mission Monastery.

HERITAGE PLACE

As above.

PRIORY DRIVE

As above.

TARA PLACE

Tara was the first son of Whatonga and recognized as the first ancestor in Hawke’s Bay.”

While the request for street names was first received by Council from EHJV on 11 January, Morehu Te Tomo, Pou Whakarae for Council advised that not all members of Mana Ahuriri had agreed to the endorsement of the proposed names. Officers took the prudent step of asking for the proposal to be returned to Mana Ahuriri for full endorsement before putting it before Council Committee for a decision. This was obtained on 5th March following hui between Mana Ahuriri and Te Taiwhenua o Te Whanganui ā Orutu. To minimise delay to EHJV, officers continued to process the subdivision consents without street names while awaiting the endorsement.

The proposal has now been extensively consulted with mana whenua. As Ngā Mānukanuaka o te Iwi committee meeting is not until May, it is recommended that the proposal proceed to the earliest available Council Committee meeting being Prosperous Napier Committee.

3.4 Implications

Financial

The financial implications of street naming include minor administrative costs incurred by Council’s GIS team and are covered in the fee paid to Council by the developer. The cost of erecting street signs, road markings, and street lights are costs incurred solely by the developer.

Social & Policy

There are not considered to be any inherent social or policy implications in relation to the use of the proposed street names.

Risk

It is not considered that Council would be liable to any legal risk by the use of the proposed street names.

A check via the Hastings and Napier Council GIS databases confirms that there is no significant clashes between the proposed street names and existing street names within the Hawkes Bay Region. The minor exceptions being:

· Tara Place, c.f. Tara Lane in Parkvale, Hastings.

· Mission Hills Avenue, c.f. Mission Road in Greenmeadows, Napier.

· Mission Hills Drive, c.f. Mission Road in Greenmeadows, Napier.

However, it is considered that with the naming variances of Mission Hills Avenue, Mission Hills Drive and Mission Road, there are sufficient differences to be able to distinguish between the each of the different roading network names. Furthermore, all are adjacent to the Mission Estate, and therefore significantly reduces the potential to create any significant issue in considering geographic location.

Furthermore, as the location of the existing Tara Lane and Tara Place are located in two separate local government areas, it is considered that this complies with Section 4.4.7 of AS/NZ 4819:2011 – Standards New Zealand, Rural and Urban Addressing.

3.5 Considerations

It is considered that the naming process adheres to the criteria set out in AS/NZ 4819:2011. In addition to this, there has been consultation with Iwi and consideration given to the site’s history to devise the names submitted for each of the proposed roads within the new roading network within Stage 1 of the Mission Hills Residential Subdivision Development. Accordingly, the proposed names are considered appropriate.

Nil

4. Procurement planning reporting

|

Type of Report: |

Information |

|

Legal Reference: |

N/A |

|

Document ID: |

1740016 |

|

Reporting Officer/s & Unit: |

Sharon OToole, Procurement Manager |

4.1 Purpose of Report

The purpose of this report is to outline the process for the approval of procurement planning documents and how to improve the visibility of significant projects and contracts to Council through regular reporting.

The delegation of powers and authority from Council to committees and to the Chief Executive is an essential part of having effective and efficient governance and management systems in place.

A Financial Delegation includes the approval to commit expenditure on the Council’s behalf and includes contracts and contract variations, Memorandum of Understanding’s, rents and leases for equipment, as well as purchase orders, works orders, and other purchases of services, works or goods.

Financial delegations are a financial control that help support Council’s strategic priorities to be a financially sustainable Council.

4.3 Issues

Council uses procurement planning documents to help manage the process of finding and selecting the suppliers that will provide services, works or goods. The purpose of a procurement plan is to increase the efficiency, effectiveness and transparency of the procurement process. The document encourages teams to consider how works or services will be acquired and how suppliers and consultants and contractors will be managed during the project - the type of contract that will be used, delivery dates, the type of metrics that will be used to evaluate performance, and an explanation of how the procurement process will be performed.

The procurement plan is an operational document which establishes the roadmap on how expenditure will be made, as it is a ‘plan’ there is no financial commitment. The award of a contract is more usually the expenditure commitment which requires financial approval.

4.4 Significance and Engagement

NA

4.5 Implications

Financial

To ensure appropriate oversight of decisions the approval of procurement plans will be aligned with Council financial delegations. Those that exceed the delegated financial authority of directors will require CE approval. Procurement plans and procurement strategy documents for significant, complex or high-risk projects will be approved by the CE regardless of value.

Details of procurement plans which require CE approval will be included in the quarterly financial report to Council. This will provide greater transparency and visibility around significant contracts and projects. This reporting is in addition to any project specific governance and reporting arrangements that have been agreed.

Social & Policy

NA

Risk

Standardizing the oversight of significant procurement and contract activities will strengthen current risk and assurance processes.

4.6 Preferred Option

Inclusion of procurement plan details which require CE approval to be included in the quarterly financial report to Council.

Nil

5. Treasury Activity and Funding Update

|

Type of Report: |

Procedural |

|

Legal Reference: |

N/A |

|

Document ID: |

1742954 |

|

Reporting Officer/s & Unit: |

Garry Hrustinsky, Corporate Finance Manager Caroline Thomson, Chief Financial Officer |

5.1 Purpose of Report

The purpose of this report is to update the Prosperous Napier Committee on Council’s treasury activity.

|

|

Officer’s Recommendation The Prosperous Napier Committee: a. Receive the report titled Treasury Activity and Funding Update dated 28 March 2024.

|

Investments

As at 8 March Council held $14m on term deposit at an average interest rate of 5.70%.

The following table reports the cash and cash equivalents on 29 February 2024:

|

8 March 2024 |

$000 |

|

Cash on call |

$4,160 |

|

Short term bank deposits |

$14,000 |

|

Total cash and deposits |

$18,160 |

Debt

Council’s current total external debt position as at 8 March is $10m. During June 2023 $10m was borrowed from the Local Government Funding Agency (LGFA) in two tranches at fixed interest rates. The details are as follows:

|

Draw date |

Amount |

Interest rate |

Maturity date |

|

21/06/2023 |

$5m |

5.61% |

15/04/2026 |

|

21/06/2023 |

$5m |

5.46% |

15/05/2028 |

Council’s debt portfolio is managed within macro limits set out in the Treasury Policy. It is recognised that from time to time Council may fall out of policy due to timing issues. The Treasury Policy allows for officers to take the necessary steps to move Council’s funding profile back within policy in the event that a timing issue causes a breach in policy.

Year end external debt is forecast to be $67m (2023/24 projections)

Council’s internal debt balance is $98.2m

Council is currently compliant with its Treasury Management Policy.

Council’s current Long Term Plan (LTP) forecasts a closing debt position of $312m at the end of 2026/27. This calculation is based on the assumption that capital projects budgets will be completed.

The Reserve Bank of New Zealand’s (RBNZ) Official Cash Rate (OCR) is at 5.5% at its last review on 28 February 2024. The next review is on 10 April 2024.

In making it’s decision the RBNZ noted “Core inflation and most measures of inflation expectations have declined, and the risks to the inflation outlook have become more balanced.” Although no further rate rises are expected this year, inflationary pressure from sectors such as the rental market have prevented cuts during this rates review.

Debt to revenue ratio headroom

This is the key measure for Councils debt profile as it is the measure used by Council’s major funders.

The closer Council gets to its limits the more likely it is that it will experience problems raising new debt. A Council with a credit rating would experience an increase in cost of funds (lower credit rating and higher borrowing margins).

Council’s Treasury Policy for net external debt as a percentage of income is set at 175%. As at 29 February Council’s debt to income ratio was 6.9%. Council has substantial debt headroom (extra capacity to borrow) to respond to any future event.

Council is compliant with its debt to income ratio for the LTP. Officers are exploring the option around taking on a credit rating. This would unlock more competitive borrowing rates through the LGFA and could increase Council’s debt limit to 280% of its revenue (providing more headroom to borrow). There is a cost to maintain a credit rating and requires council’s financials to be externally audited each year. Once Council reaches approximately $100m of external borrowings the interest savings achieved from having a credit rating start to outweigh the audit cost.

5.3 Issues

No issues

5.4 Significance and Engagement

N/A

5.5 Implications

Financial

N/A

Social & Policy

N/A

Risk

N/A

5.6 Options

The options available to Council are as follows:

a. Receive the report titled Treasury Activity and Funding Update dated 28 March 2024

b. Amend the report titled Treasury Activity and Funding Update dated 28 March 2024.

c. Reject the report titled Treasury Activity and Funding Update dated 28 March 2024.

5.7 Development of Preferred Option

N/A

Nil

6. Financial Forecast to 30 June 2024

|

Type of Report: |

Operational and Procedural |

|

Legal Reference: |

N/A |

|

Document ID: |

1739748 |

|

Reporting Officer/s & Unit: |

Caroline Thomson, Chief Financial Officer Talia Foster, Financial Controller |

6.1 Purpose of Report

To report to Council the financial forecast to the 30 June 2024 for the whole of Council.

|

|

Officer’s Recommendation The Prosperous Napier Committee: a. Receive the report titled Financial Forecast to 30 June 2024.

|

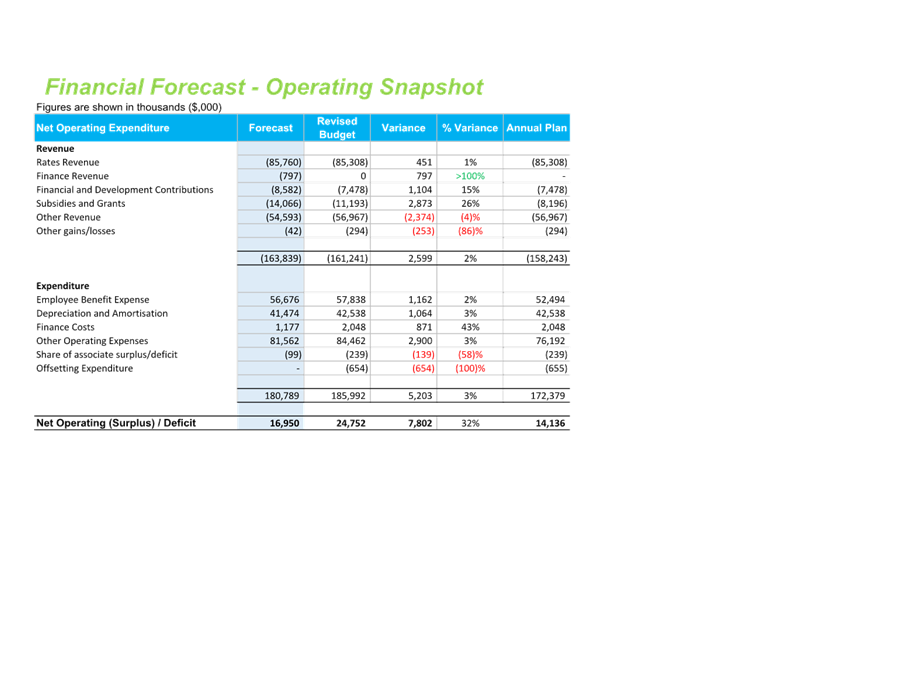

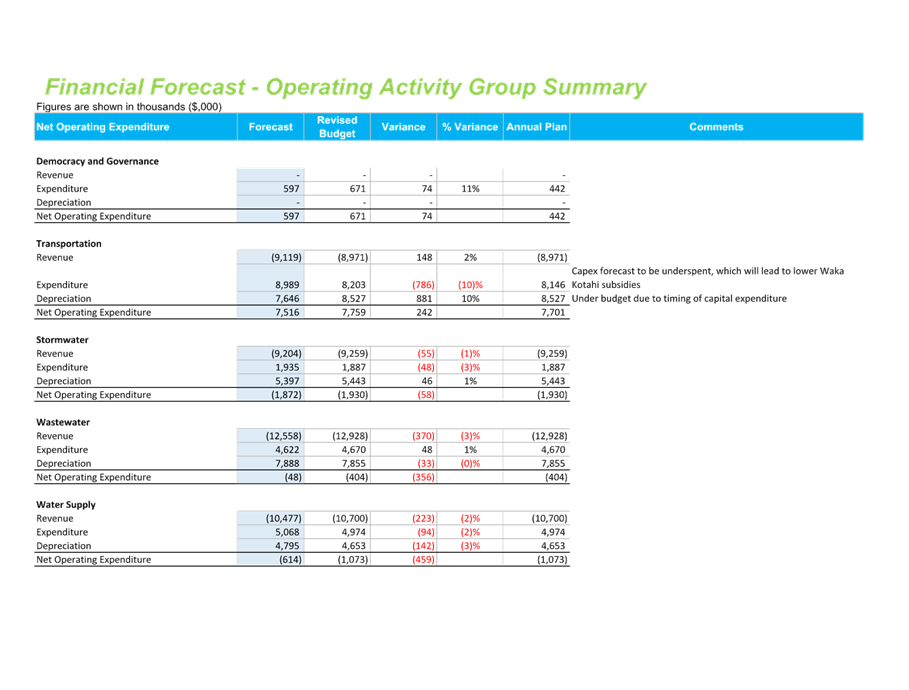

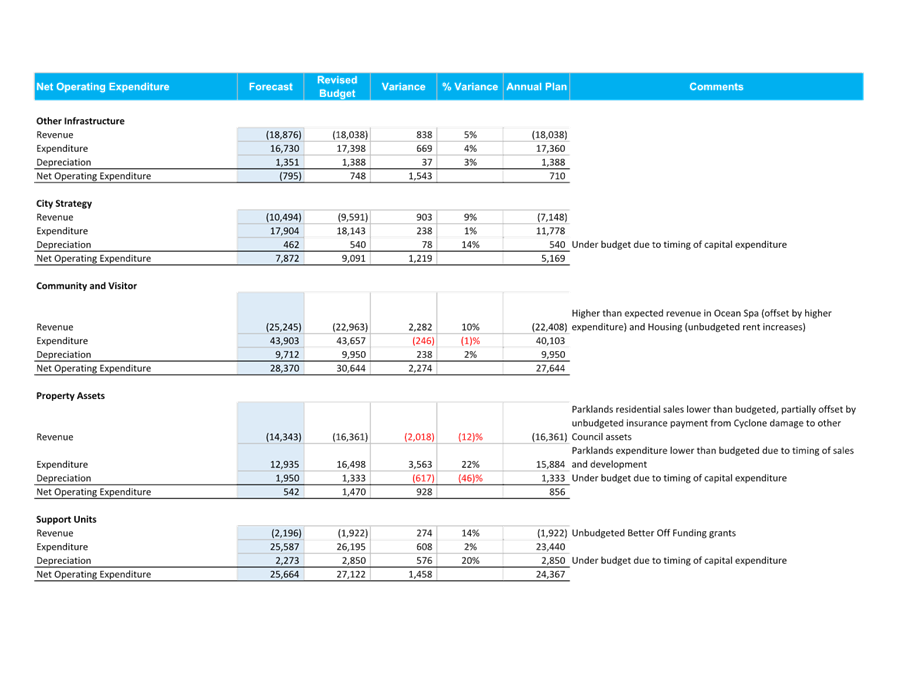

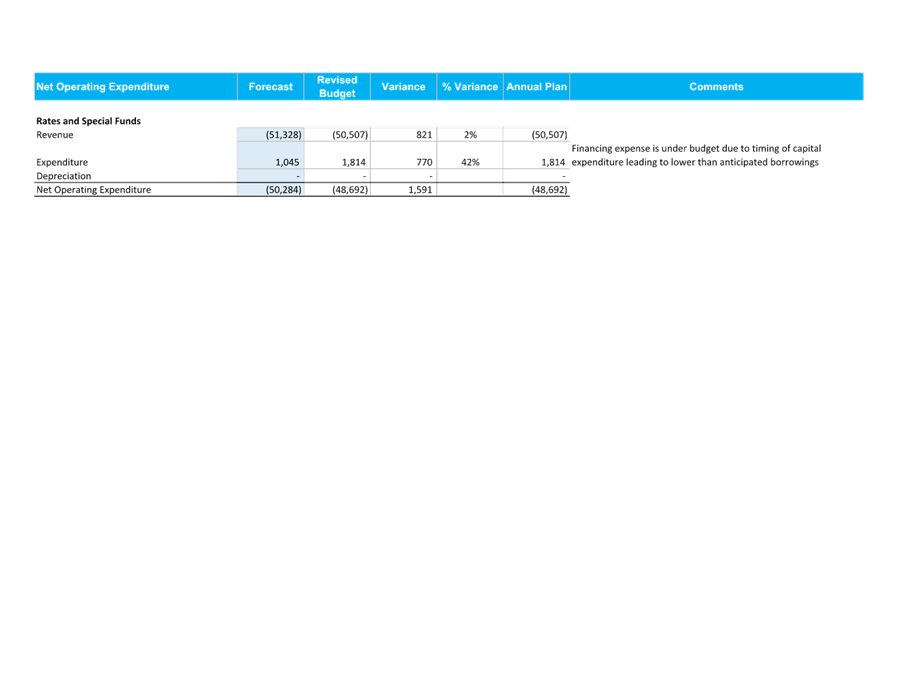

The purpose of this report is to provide a financial forecast for Council’s operating and capital expenditure to 30 June 2024. The operating and capital forecasts are based on actual expenditure January year to date, plus estimated remaining spend for the 2023/24 financial year. Attachment 1 provides analysis of the variations between the financial forecast for 2023/24, the revised budget, and the Annual Plan 2023/24 for both capital and operational items.

The revised budget is where the Annual Plan has been amended for capital and operating budgets carried forward from 2022/23, and additional staffing resources approved since the adoption of the Annual Plan.

Net operating expenditure (accounting result)

The operational forecast shows a forecast net deficit of $17.0m at 30 June 2024 which is below the revised budget deficit of $24.8m, but above the Annual Plan budget deficit of $14.1m (see Attachment 1).

When we set the Annual Plan for 2023/24 Council agreed to loan fund operating costs so that the rates increase was smaller. This meant borrowing to fund operating expenditure, resulting in an unbalanced budget and net operating deficit position. This funding approach is not considered sustainable in the long term. Council has changed its funding strategy for the Long Term Plan and is not proposing to borrow for operating expenditure and will run a balanced budget for 9 out of the 10 years.

The main variance in the operating expenditure compared to the Annual Plan is due to Employee Benefits. Additional resources which were approved since the adoption of the Annual Plan were intended to be offset by additional revenue and lower expenditure in other areas. While the Other Operating Expenditure is lower than budget, it is not enough to fully offset the additional employee expenses. Additional revenue looks unlikely to be achieved.

Net rates position

In terms of Local Government, the rating result is regarded as being an important indicator as it shows how the rates that were collected have been spent.

The forecast rates position shows a net rates surplus of $530k mainly due to lower than anticipated other operating expenditure and higher than budgeted revenue from subsidies and grants. There will be an exercise at year end to review the timing of the grant revenue (i.e. if we have not spent it we may not be able to record the income), and to ensure that the expenditure is correctly recorded to offset it. This exercise could further affect the rates position. The forecast rates surplus of $530k equates to 0.6% of rates. Officers will be recommending that any rates surplus at year end is used to repay debt.

The following table sets out Council’s forecast rates position for the year ended 30 June 2024:

Capital plan

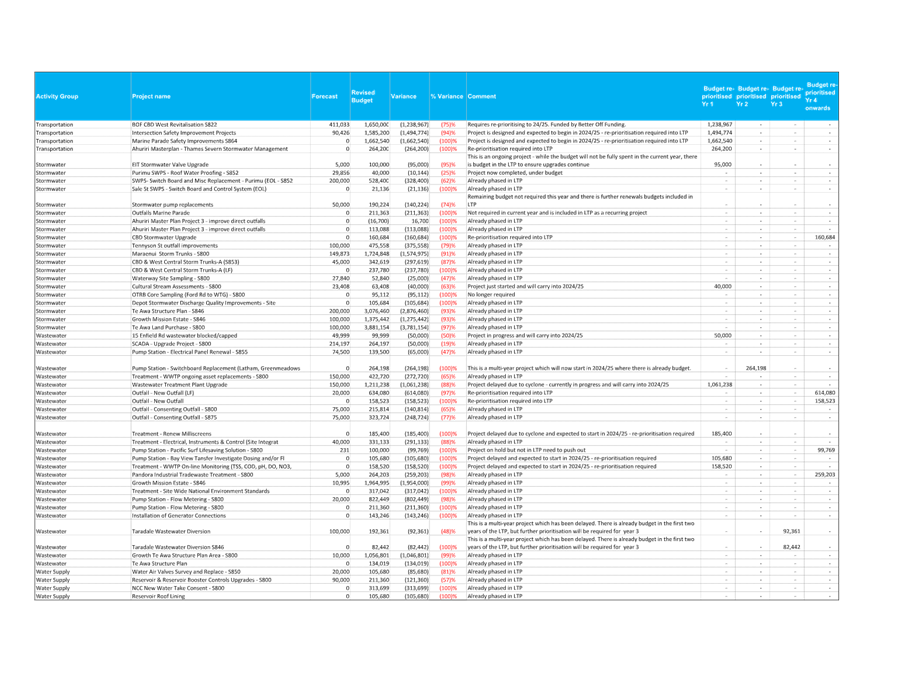

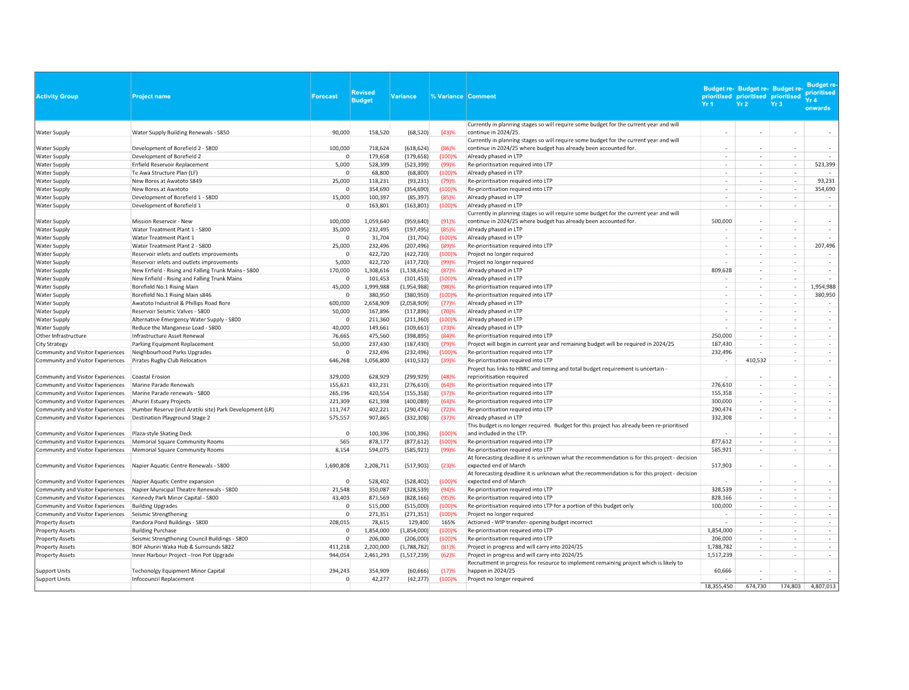

Officers have reviewed the timing of the capital programme and this has resulted in a number of projects being reprioritised. The capital plan for 2023/24 (including vested assets) is forecast at $51.7m compared to a revised budget of $102.3m and Annual Plan budget of $75.9 (see Attachment 1). The key movements in the forecast capital plan are set out below:

|

Figures are shown in thousands ($,000) |

|

|

|||

|

Capital Expenditure |

Forecast |

Revised Budget |

Variance |

% Variance |

Annual Plan |

|

Transportation |

10,302 |

14,962 |

(4,660) |

(31)% |

11,848 |

|

Stormwater |

3,780 |

15,528 |

(11,748) |

(76)% |

14,452 |

|

Wastewater |

5,484 |

14,293 |

(8,809) |

(62)% |

12,017 |

|

Water Supply |

6,266 |

17,359 |

(11,093) |

(64)% |

16,474 |

|

Community and Visitor Experiences |

17,762 |

24,713 |

(6,951) |

(28)% |

15,557 |

|

Property Assets |

2,314 |

7,551 |

(5,237) |

(69)% |

423 |

6.3 Issues

There are capital projects worth $25m that have been re-budgeted in the proposed capital plan for the 2024-34 Long Term Plan. Council’s policy position of not carrying forward budget from one financial year to the next means that funding for the remaining unspent capital budgets of $25m will be re-forecast as part of the revised budget process in 24/25. Officers will work to the same fiscal envelope for 2024/25 when revising the capital budgets which may involve moving projects into future years of the LTP.

Executive Directors will be available at the meeting to provide further detail on the status of capital projects.

6.4 Significance and Engagement

The issues for discussion are not significant in terms of Council’s Significance and Engagement Policy and no consultation is required.

6.5 Implications

Financial

The attachment includes a summary schedule showing forecast operating and capital expenditure by activity group against the revised budget and compared to Annual Plan. The attachment also includes detail at a project level where the forecast expenditure varies from the revised budget.

Social & Policy

N/A

Risk

Given the large capital programme there is a risk that some projects may not be completed as forecast due to capacity and market constraints. Officers will continue to monitor and identify any variance to the capital work programme and will report to management on a monthly basis and Council quarterly.

6.6 Options

The options available to Council are as follows:

a. Council receive the financial forecast to 30 June 2024.

b. Council provide feedback to officers.

6.7 Development of Preferred Option

Option a. Council receives the financial forecast to 30 June 2024.

Recommendation to Exclude the public

That the public be excluded from the following parts of the proceedings of this meeting, namely:

AGENDA ITEM

1. Debt write off

The general subject of each matter to be considered while the public was excluded, the reasons for passing this resolution in relation to each matter, and the specific grounds under section 48(1) of the Local Government Official Information and Meetings Act 1987 for the passing of this resolution were as follows:

|

General subject of each matter to be considered.

|

Reason for passing this resolution in relation to each matter.

|

Ground(s) under section 48(1) to the passing of this resolution.

|

|

1. Debt write off |

7(2)(a) Protect the privacy of natural persons, including that of a deceased person |

48(1)(a) That

the public conduct of the whole or the relevant part of the proceedings of

the meeting would be likely to result in the disclosure of information for

which good reason for withholding would exist: |

Prosperous Napier Committee

Open Minutes

|

Meeting Date: |

Thursday 8 February 2024 |

|

Time: |

9.30am – 11.45am |

|

Venue |

Chapman Room |

|

|

Livestreamed via Council’s Facebook page |

|

Present |

Chair: Councillor Crown Members: Mayor Wise, Deputy Mayor Brosnan, Councillors Boag, Browne, Chrystal, Greig, Mawson, McGrath, Price, Simpson, Tareha and Taylor (Deputy Chair) Ngā Mānukanuka o te Iwi representative – Evelyn Ratima |

|

In Attendance |

Chief Executive (Louise Miller) Deputy Chief Executive / Executive Director Corporate Services (Jessica Ellerm) Executive Director Infrastructure Services (Russell Bond) Executive Director Community Services (Thunes Cloete) Manager Communications and Marketing (Julia Atkinson) Chief Financial Officer (Caroline Thomson) Programme Manager- Long Term Planning (Stephanie Murphy) Corporate Finance Manager (Mr Hrustinsky) Strategic Programmes Manager (Mr Gillies) Senior Advisor Corporate Planning (Danica Rio) Commercial Director (Richard Munneke) Manager Community Strategies (Anne Bradbury) Scott Hamilton - Tautaki Consulting [via zoom link] Team Leader Governance (Anna Eady) |

|

Administration |

Governance Advisor (Carolyn Hunt) |

Prosperous Napier Committee – Open Minutes

Table of Contents

Order of Business Page No.

Karakia

Apologies

Conflicts of interest

Public forum

Announcements by the Mayor

Announcements by the Chairperson

Announcements by the management

Confirmation of minutes

Agenda Items

1. Direction for the Preparation of the Three-Year Plan 2024-27

2. Due Diligence Report of Civic Accommodation Business case

3. Investment Policy Review

4. Investment Property Portfolio Policy (Leasehold) Review

5. Investment Strategy Next Steps

Minor matters

Order of Business

The meeting opened with the Council karaka.

|

Councillors Mawson / Tareha That the apology from Joe Tareha (Ngā Mānukanuka o te Iwi representative) be accepted. Carried |

Nil

Nil

Nil

Announcements by the Chairperson

Nil

Announcements by the management

Nil

|

Councillors Mawson / Price That the Minutes of the Prosperous Napier Committee meeting held on 7 September 2023 were taken as a true and accurate record of the meeting.

Carried |

1. Direction for the Preparation of the Three-Year Plan 2024-27

|

Type of Report: |

Legal and Operational |

|

Legal Reference: |

Local Government Act 2002 |

|

Document ID: |

1730288 |

|

Reporting Officer/s & Unit: |

Danica Rio, Senior Advisor Corporate Planning Stephanie Murphy, Programme Manager- Long Term Planning Jessica Ellerm, Deputy Chief Executive / Executive Director Corporate Services Caroline Thomson, Chief Financial Officer |

1.1 Purpose of Report

Council has been providing direction for the preparation of NCC’s Three-Year Plan 2024-27 through a series of workshops over 2023 and early 2024. The plan is being prepared under the Severe Weather Emergency Recovery Legislation (SWERL) and replaces the Long Term Plan due to the legislation. The report summarises the following for formal approval and adoption:

· Direction on the financial and infrastructure information that will underpin the combined Finance and Infrastructure Strategy

· Proposed topics for consultation that is scheduled to begin on 25 March 2024

· Direction on Strategic Priorities and Community Outcomes

|

At the meeting Senior Advisor Corporate Planning, Ms Rio spoke to the report and displayed a PowerPoint presentation (Doc Id 1736691) providing an overview of the report. Community Services have indicated an intention for the Faraday Centre facility to be re-imagined, and that Te Pihinga would be considered as part of the Halls Review programmed for Year 2. Key dates noted for the programme are: · 14 March 2024 –Council adoption of the consultation document · 25 March-26 April 2024 – Public consultation period · 27-28 May 2024 – Council submission Hearings · 27 June 2024 – Council adoption of the three year plan. In response to questions the following was clarified: The Chief Financial Officer, Ms Thomson referred to the Capex projects that were high spend but required minimal officer input and explained the implications to Council’s budget. · Vested assets are where a developer funds an infrastructure project in a new development or subdivision and it is vested back to Napier City Council (NCC) as capital. Capital assets need to be included in the fixed asset register. · Property purchases are transactions where NCC is buying property. · Omarunui is the Landfill which is owned and funded jointly between Hastings District Council and NCC. The Landfill is operated by Hastings District Council. Napier’s share of the joint funding is approximately 33%. · Parklands is a transactional project. · Ms Thomson confirmed the operational costs listed for the Ahuriri Regional Park remained in Council budgets.

|

|

|

Committee resolution

|

Councillors Mawson / Price The Prosperous Napier Committee: a. Receive the report titled “Direction for the Preparation of the Three Year Plan 2024-27” and confirm it as being a record of direction setting for the development of the Three-Year Plan 2024-27. Carried |

|

|

Attachments 1 LTP PowerPoint presentation (Doc Id 1736691) |

2. Due Diligence Report of Civic Accommodation Business case

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |

|

Document ID: |

1710275 |

|

Reporting Officer/s & Unit: |

Darran Gillies, Strategic Programmes Manager Alix Burke, Strategic Programme Coordinator |

2.1 Purpose of Report

To report on a robust due diligence process that ensures that the preferred option of Officer Accommodation Business Case continues to be the best course of action for council. This includes making sure that the work enables the best possible outcomes of the public-facing component of the programme, primarily the implementation of the design and construction of Te Aka - Library and Council Chambers.

|

The Strategic Programmes Manager, Mr Gillies spoke to the report summarising the preferred option where Council sells the ex-Library Tower and leases back part of a redeveloped site for NCC’s long-term occupation. Scoring highest on both the best outcomes score and the best value for money score. In response to questions the following was clarified: · There is officer capacity within Council to run the Te Aka project. · Mr Gillies advised that in regard to timeframes for delivery completion, the ground lease to developer to Council redevelopment there would be a negotiation period that would be required within the developer option and Resource Management Act consultation undertaken. · If negotiations went well the timeframe could be brought forward, however there is a risk of a timeline increase if one party opts out during negotiations as the process would need to commence again. · The concept work provides a better understanding of Council’s requirements and work that needs to be undertaken. · An amount of $7m has been identified for the “soft fit out” and IT, however full requirements have yet to be determined. It is envisaged that the $48m budget plus professional fees will be the total for the project. · If Council retain ownership of the building there is the opportunity to generate income through tenancy on the top floor and partial tenancy on the ground floor. · However the current community expectation is that NCC will retain ownership and stay onsite. · Retention of ownership has not been communicated to the public prior to the business case. The site had been referred to as a “precinct” and that the project would be staged. The risk, being time is cost and benefit cost realisation was not taken into account in mobilisation of one contract, looking at shared services across the two projects. The risk is what that the subdivision looks like and is it attractive to the developer. · The business case indicated $4m for hard fit out but did not include additional fittings required for an operational office block. The revised budget is now $7m. · The next stage in the programme is testing the full concept and design of the tower and how it relates to Te Aka, specifically the Chambers. The aim is to bring the tower and Te Aka projects together for shared synergies and to understand the costs. · If approved by Council this will assist in moving to the plan for the procurement process |

|

|

Committee resolution

|

Deputy Mayor Brosnan / Councillor Tareha The Prosperous Napier Committee: a. Receive The Due Diligence Report of the Civic Accommodation Business Case. b. Approve option 5a from the Civic Accommodation Business Case (Doc Id 1690557) – The NCC lead Redevelopment of the library to be the preferred option within the Long Term Plan consultation; and to proceed into the next stages of the programme of work to support that option. Carried |

|

Type of Report: |

Legal and Operational |

|

Legal Reference: |

Local Government Act 2002 |

|

Document ID: |

1732872 |

|

Reporting Officer/s & Unit: |

Garry Hrustinsky, Corporate Finance Manager |

3.1 Purpose of Report

The purpose of this report is to review the Investment Policy with consideration to proposed changes to Napier City Council’s investment strategy.

|

At the meeting The Corporate Finance Manager, Mr Hrustinsky spoke to the report providing a brief summary of the three material amendments to the policy being clarification of the role of Development Property, Investment Property and Council Controlled Organisations (CCOs). Mr Hrustinsky also noted due to the specialised nature of investing public consultation was not required for amendments to this policy. Changing the policy to expand and enable the use of CCOs provides NCC with the flexibility to use CCOs but is not binding. |

|

|

Committee resolution

|

Mayor Wise / Councillor Mawson The Prosperous Napier Committee: a) Approve the amended Investment Policy (Doc Id 1735035). Carried |

4. Investment Property Portfolio Policy (Leasehold) Review

|

Type of Report: |

Operational |

|

Legal Reference: |

Local Government Act 2002 |

|

Document ID: |

1733205 |

|

Reporting Officer/s & Unit: |

Garry Hrustinsky, Corporate Finance Manager |

4.1 Purpose of Report

In addition to the requirement to review this policy at least every 3 years, the main purpose of this report is to review the Investment Property Portfolio Policy with consideration to proposed changes to Napier City Council’s investment strategy.

|

At the meeting The Corporate Finance Manager, Mr Hrustinsky spoke to the report advising that NCC was currently reviewing its investment strategy which means some amendments to this policy are required. Mr Hrustinsky provided a brief summary on the three material changes, being the removal of reference to outdated reports, the process for freeholding land being updated to reflect proposed investment changes and the option for Council to delegate to a Council Controlled Organisation or investment team. In response to questions the following was clarified: · Where an offer to freehold is not accepted by the current lessor Council would have the option to look at offers from other parties. This had not previously been possible. · In practice Council could not enforce a lessor’s right to occupy if it sells land. Council can give the lessor first refusal to buy the land the lessor occupies, if they decline then Council could sell that land to another party - but the lessor retains their right to occupy. · Changes in the policy provides language consistency. · If a person has a lease and invests in capital items on the property and could not or did not want to purchase the property it cannot be sold and the lease would be renewed. · If a leaseholder did not wish to continue with the lease it would be a trigger for this policy. Council is bound by its leases and contracts. · If the contract renews, Council would honour the renewal. If the contract does not renew and the lessee chooses to buy the property Council would honour that. If the contract does not renew and the lessor chooses not to buy the property and looks to exit the property the Council would then have the option to sell. · If the lease agreement comes to an end Council could renegotiate a new contract if lessee exits the property. · Legal advice will be sought in relation to the a leaseholder retaining occupancy rights if NCC sells a property to a third party.

The meeting agreed to seek legal advice on transfer of leases and that the decision for approval be referred to the Council meeting on 14 March 2024.

|

|

|

Committee resolution

|

Councillors Crown / Taylor The Prosperous Napier Committee: a) Defer approval of the amended Investment Property Portfolio Policy (Doc Id 1735038) subject to legal advice being sought in relation to the transfer of leases.

b) Refer the Investment Property Portfolio Policy report to the Ordinary Council meeting on 14 March 2024 for a decision on approval. Carried |

Councillor Boag left the meeting at 10.31am

5. Investment Strategy Next Steps

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |

|

Document ID: |

1713691 |

|

Reporting Officer/s & Unit: |

Richard Munneke, Commercial Director Garry Hrustinsky, Corporate Finance Manager |

5.1 Purpose of Report

The purpose of this report is to obtain a decision from the Council on a proposal to establish a Council Controlled Trading Organisation (CCTO) to manage Napier City Council’s (NCC) core financial investments and to consult on its establishment through the 2024-34 Long Term Plan.

|

At the meeting The Commercial Director, Mr Munneke briefly summarised the report which would provide a way for Council to view its financial investments (Parklands and leasehold land) as a whole for the future. In response to questions the following was clarified: · Research by officers suggests that the use of a Council Controlled Trading Organisation (CCTO) would be beneficial to improve returns derived from council investment assets, and gradually reduce the rates burden on the city. · Council would like to explore the establishment of a CCTO, and will seek community feedback to do so through the Long Term Plan process. · The Long Term Plan will provide councillors the mechanism to explore CCTOs on behalf of the community in regard to external/internal membership of the Board and what assets would be included. · This was a phased approach, firstly with the exploration of creating a CCTO and what assets it may manage. · The Significance and Engagement Policy was created approximately 20 years ago. It would be beneficial to the community if some of NCC’s strategic assets are managed by the CCTO. The strategic asset list will be considered separately to the matter of a CCTO. |

|

|

Committee resolution

|

Councillors Browne / Chrystal The Prosperous Napier Committee: a. Receive the report titled “Investment Strategy Next Steps”. b. Explore the establishment of a Council Controlled Trading Organisation for the management of Council’s Investment Portfolio being Parklands development, development sites, commercial and residential leasehold properties, investment related deposits and managed investment portfolios. d. Endorse Council building investment capability within it’s team to address immediate investment activity needs. Carried |

There were no Minor Matters.

The meeting closed with a karakia at 11.45am

|

Approved and adopted as a true and accurate record of the meeting.

Chairperson .............................................................................................................................

Date of approval ...................................................................................................................... |