NAPIER CITY COUNCIL

NAPIER CITY COUNCIL

Civic Building

231 Hastings Street, Napier

Phone: (06) 835 7579

www.napier.govt.nz

Finance

Committee

Open

Agenda

|

Meeting Date:

|

Wednesday 14 June 2017

|

|

Time:

|

3pm

|

|

Venue:

|

Main Committee Room

3rd floor Civic Building

231 Hastings Street

Napier

|

|

Council

Members

|

Councillor Wise (In the Chair),

Mayor, Councillors Boag, Brosnan, Dallimore, Hague, Jeffery, McGrath,

Price, Tapine, Taylor, White and Wright

|

|

Officer Responsible

|

Director Corporate Services,

Adele Henderson

|

|

Administrator

|

Governance Team

|

Next Finance

Committee Meeting

Wednesday 2

August 2017

Finance Committee – 14 June 2017 – Open Agenda

ORDER OF BUSINESS

Apologies

Nil

CONFLICTS OF INTEREST

Public forum

Nil

Announcements by the Mayor

Announcements by the Chairperson

Announcements by the Management

Confirmation of Minutes

That the Minutes of the Finance

Committee meeting held on Wednesday, 3 May 2017 be taken as a true and accurate

record of the meeting.

Notification and Justification of Matters

of Extraordinary Business

(Strictly

for information and/or referral purposes only).

Agenda Items

1 Funding Applications........................................................................... 3

2 Fees & Charges 2017/18..................................................................... 6

3 Section 17A Review Work

Programme Plan........................................... 70

4 HB LASS Limited - Statement of

Intent.................................................. 79

5 HB Museums Trust Statement of

Intent 2017 - 19................................. 89

6 Hawke's Bay Airport Limited -

Statement of Intent................................. 95

Public Excluded ............................................................................................... 99

MINUTES…………………………………………………………………………………………………103

Finance Committee – 14 June 2017 – Open Agenda

1. Funding Applications

|

Type of

Report:

|

Operational

|

|

Legal

Reference:

|

Local

Government Act 2002

|

|

Document

ID:

|

351363

|

|

Reporting

Officer/s & Unit:

|

Belinda

McLeod, Community Funding Advisor

|

1.1 Purpose of Report

To seek approval to apply for

external funding to purchase two all-terrain wheelchairs for community use on

the foreshore and inline hockey rink boards for Bay Skate.

|

Officer’s

Recommendation

That Council:

a. Approve

that applications for external funding are made to purchase of two

all-terrain wheelchairs.

b. Approve

that applications for external funding are made to purchase inline hockey

rink boards for Bay Skate.

|

|

CHAIRPERSON’S

RECOMMENDATION

a) That Council adopt the officer’s

recommendation.

|

1.2 Issues

There are two projects that are

seeking external funding.

All-Terrain

Wheelchairs

Officers were

approached by the Halberg Disability Sport Foundation to consider providing all-terrain

wheelchairs, so that physically disabled local children and adults can have

access to recreational activities with their families particularly at the beach.

All-terrain wheelchairs move easily over any surface, including soft sand and

can float in the water, allowing transfer into a boat, surfing and swimming.

With the off-road wheels the chair can be used on wet surfaces, mud, stones,

pebbles and dusty surfaces, so people could access our pathways, beaches and

bush walks.

It is proposed

to have one wheelchair based at the Napier Aquatic Centre (Pandora Pond in the

summer) and one at the Pettigrew Arena, which would give community members easy

access to the chairs. This would give people with disabilities opportunities to participate in

recreational outdoor activities with their family and friends. Council would

provide a booking system and be responsible for the maintenance of the chairs.

The costs for

the two all-terrain wheel chairs is $15,000. The purchase of these chairs

supports the Disability Strategy currently in development.

Inline

Hockey Rink Boards

Rink boards

will enable the skating rink to be more versatile, and provide important

separation between the other skating areas. The rink boards will provide the

required infrastructure to support training, competitive games and events for

both inline hockey and roller hockey. The cost for the rink boards is

$60,000.

The Rink Boards

were not included in the original design of Bay Skate as more detail about the

needs of roller hockey was required and there was no budget allocation for it

at that time. The original focus for Bay Skate was on a functional park

with basic provisions, and it was always the intention to add more features.

For any new additional features, the Council will explore external funding

where possible or use the capital expenditure budget.

1.3 Significance and

Consultation

N/A

1.4 Implications

Financial

By presenting funding

applications to a number of providers both these items could be fully funded

externally.

Rink Boards - If external funding is unsuccessful, or not fully funded, then funding

will be sought from sponsorship (approaches are currently being made). There is

funding available from the 2017/18 Bay Skate capital budget, however, the

priority for this funding is the purchase of ramps.

Social & Policy

N/A

Risk

N/A

1.5 Options

The options available to Council

are as follows:

1. Apply for

external funding and/or sponsorship for the projects.

2. Council could

fund the projects through 2017/18 budgets. However, the rink boards are not as

high a priority as ramps, and would be unlikely to proceed in 2017/18.

1.6 Development of

Preferred Option

The preferred option is to apply

for funding for the two projects as follows:

a) All-Terrain

Wheelchairs

|

Funder

|

Apply Up To

|

|

Pub Charity

|

15000

|

|

Youth Town

|

7000

|

|

North & South Trust

|

7000

|

|

Napier RSA

|

5000

|

|

Taradale RSA

|

5000

|

|

Total:

|

$39,000

|

b) Rink

Boards

|

Funder

|

Apply Up To

|

|

New Zealand Community Trust

|

15000

|

|

North & South Trust

|

15000

|

|

Infinity Foundation

|

15000

|

|

Grassroots Trust Ltd

|

15000

|

|

Total:

|

$60,000

|

Funders have been selected in

line with their criteria/timing, and other Council project funding

requirements. This does not preclude other applications for projects being made

to the funders identified.

1.7 Attachments

Nil

Finance Committee – 14 June 2017 – Open Agenda

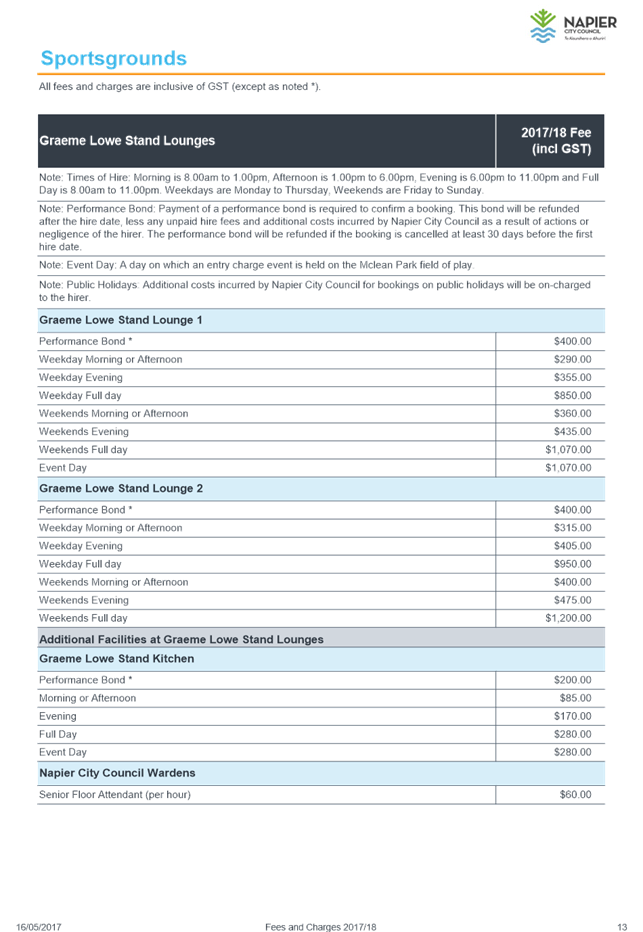

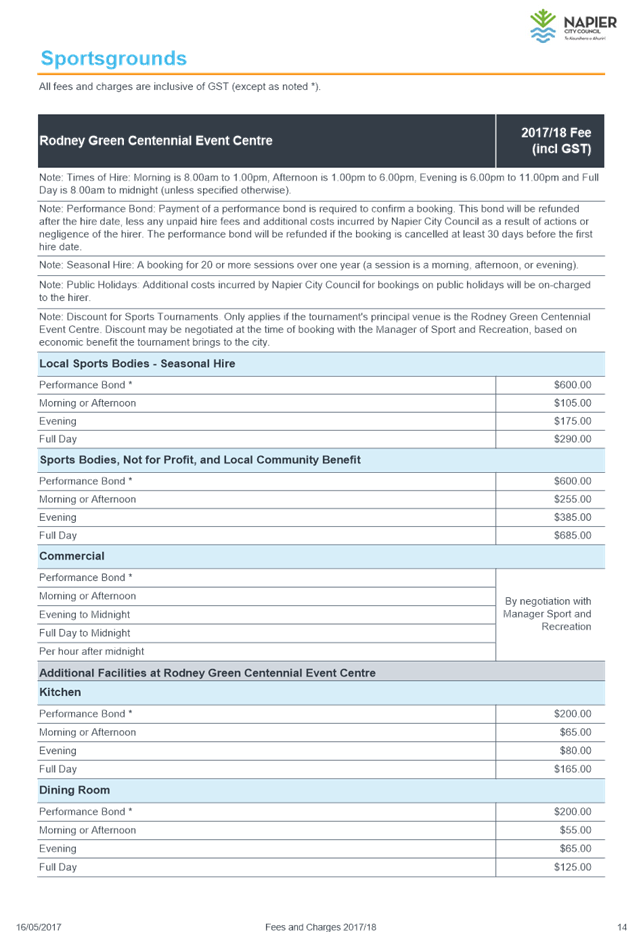

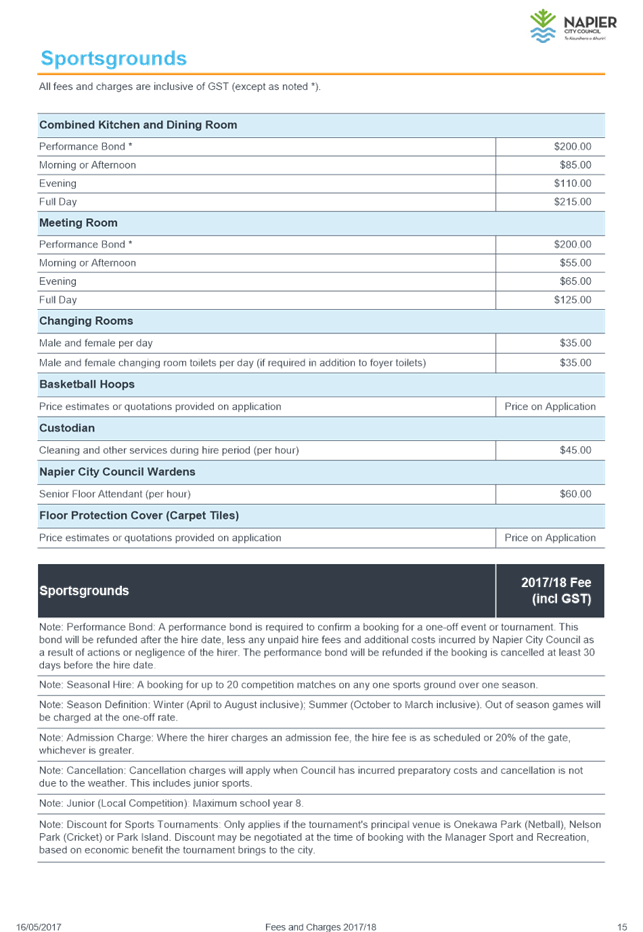

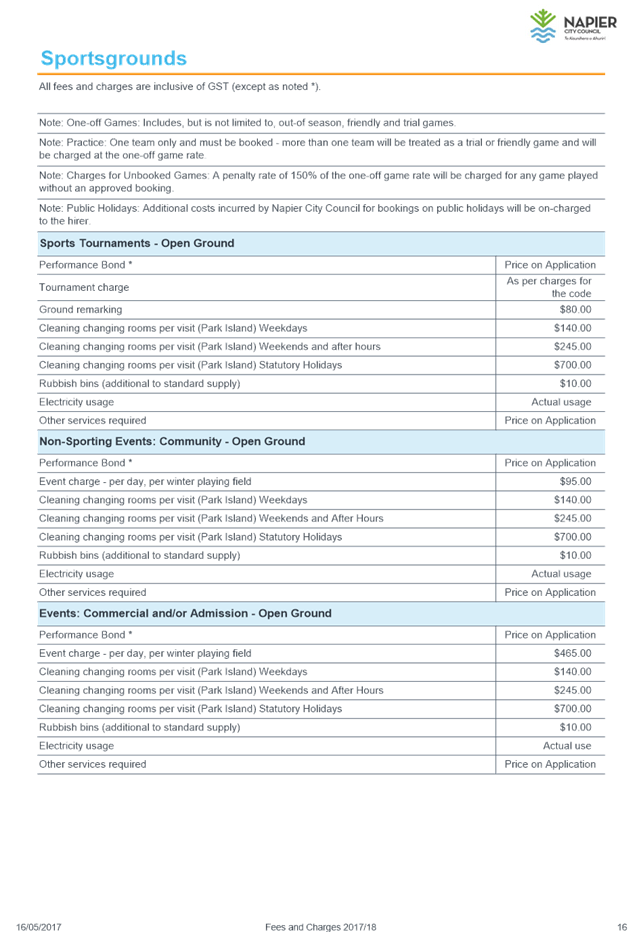

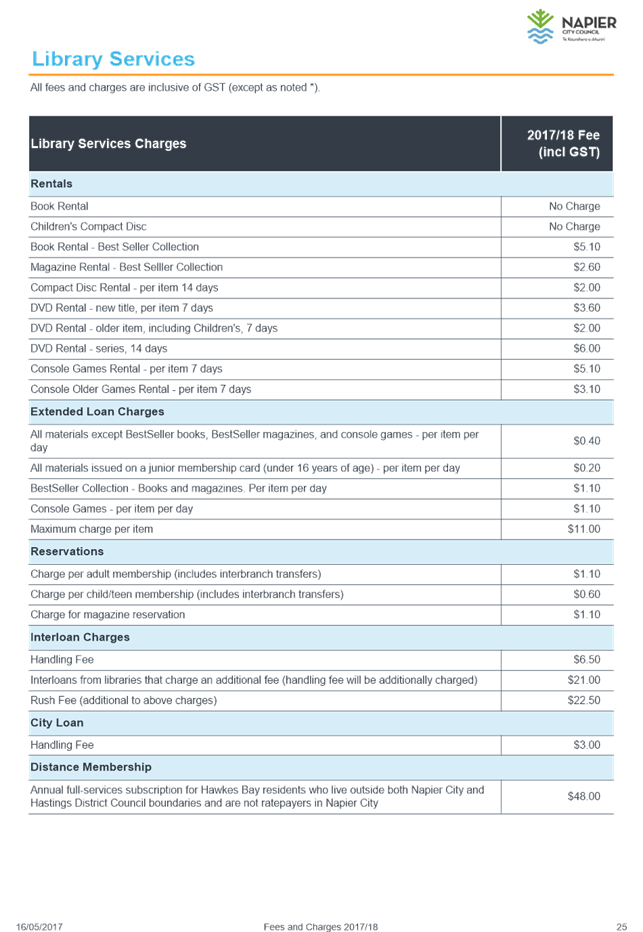

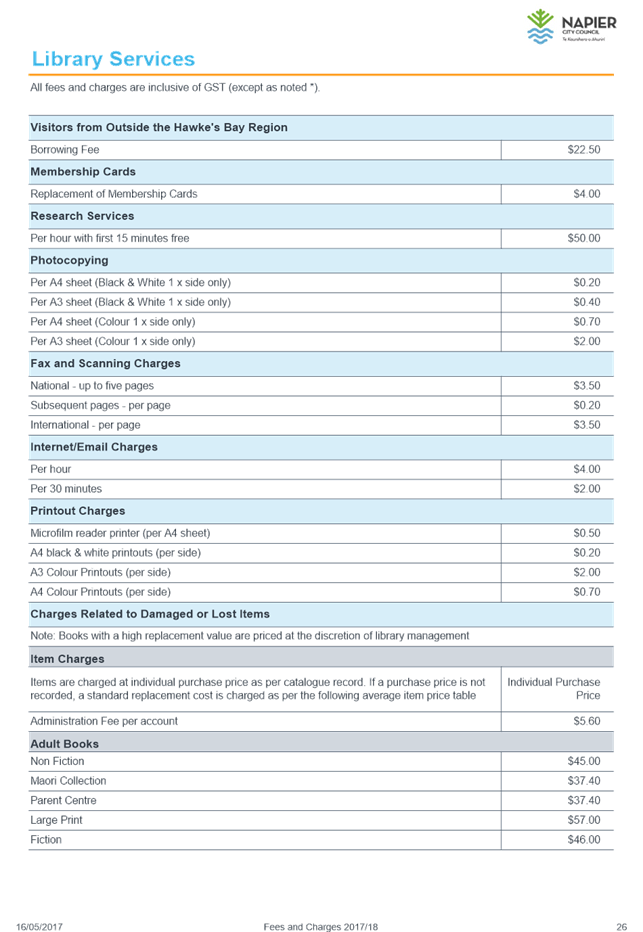

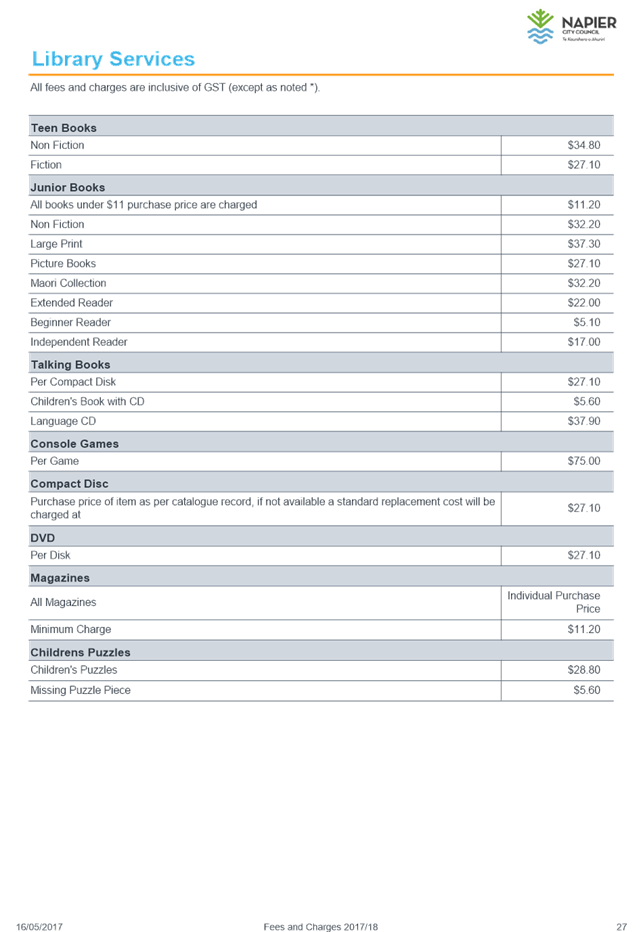

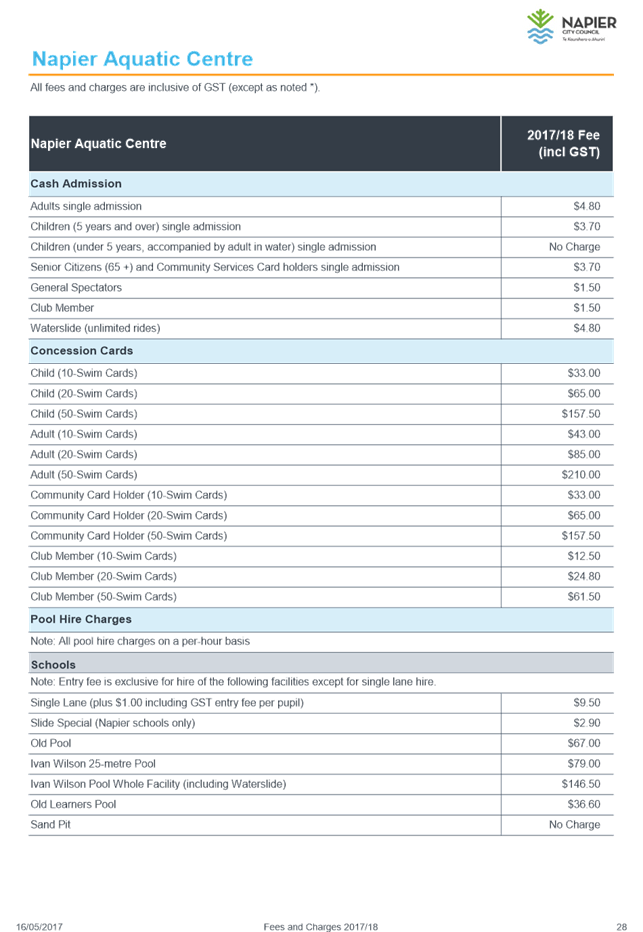

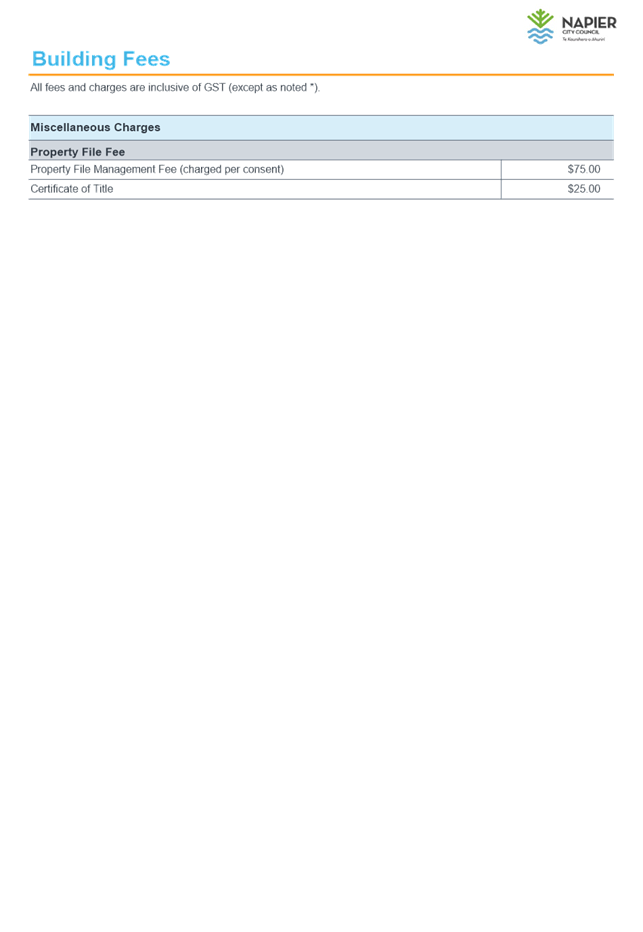

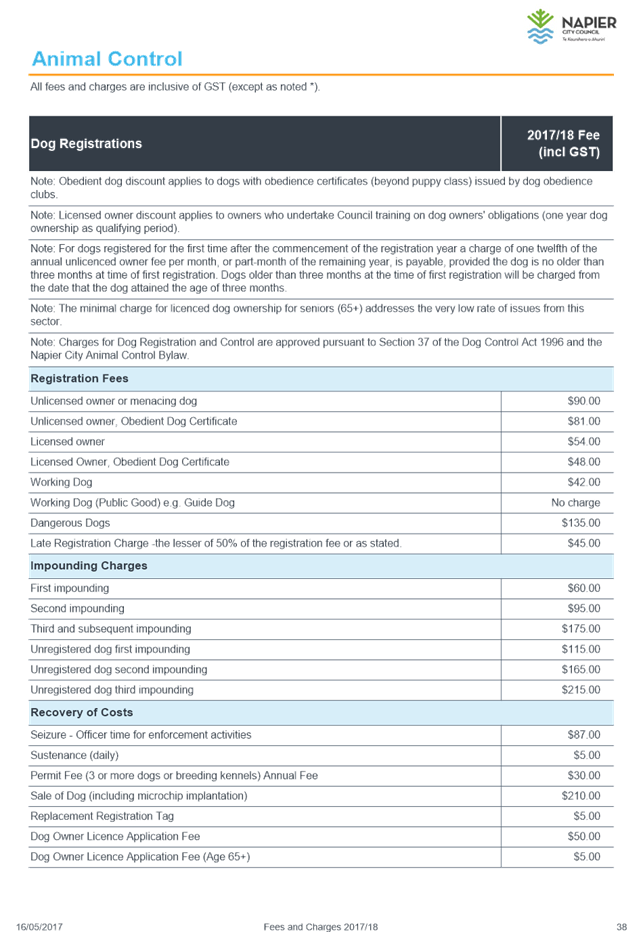

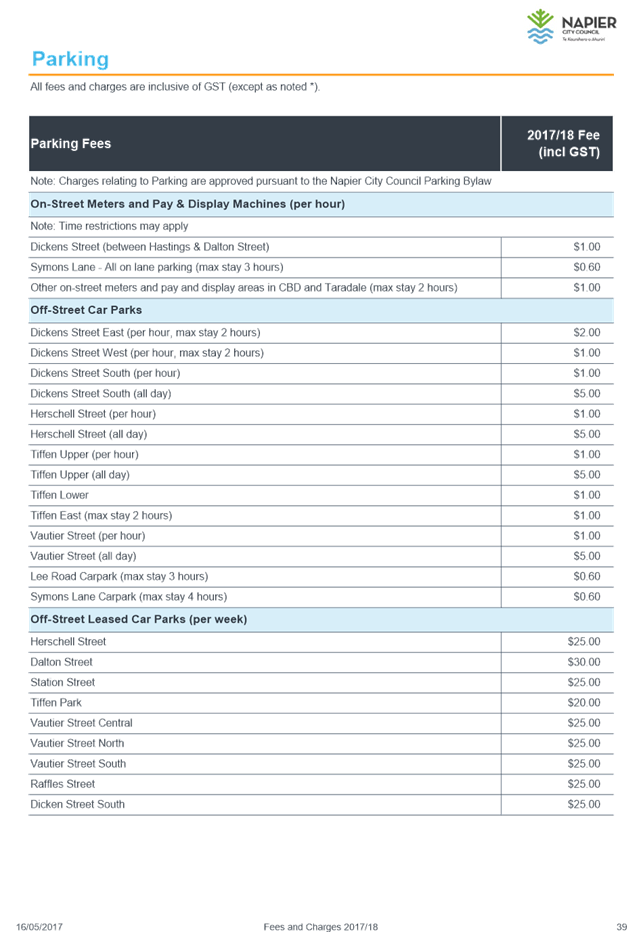

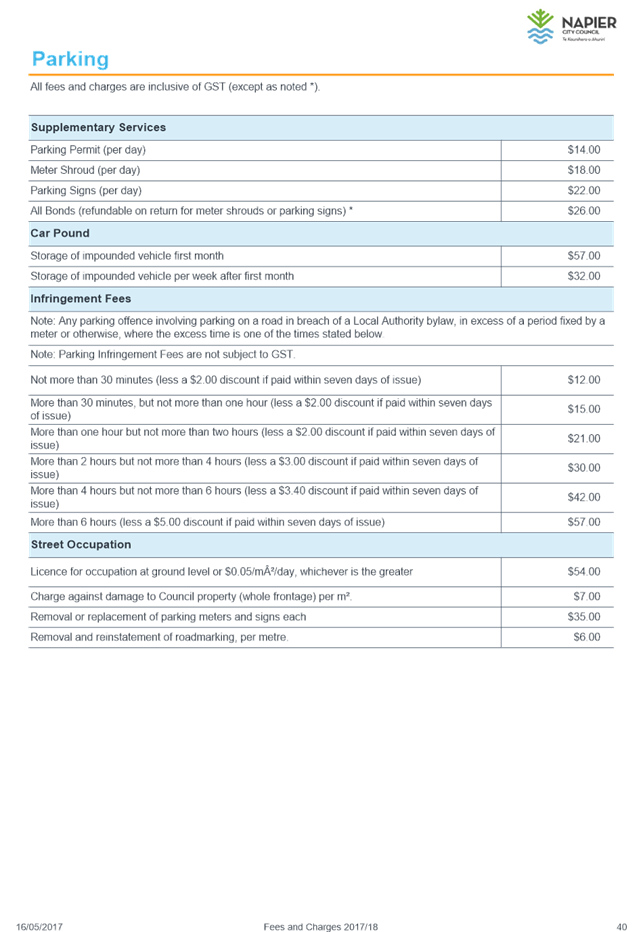

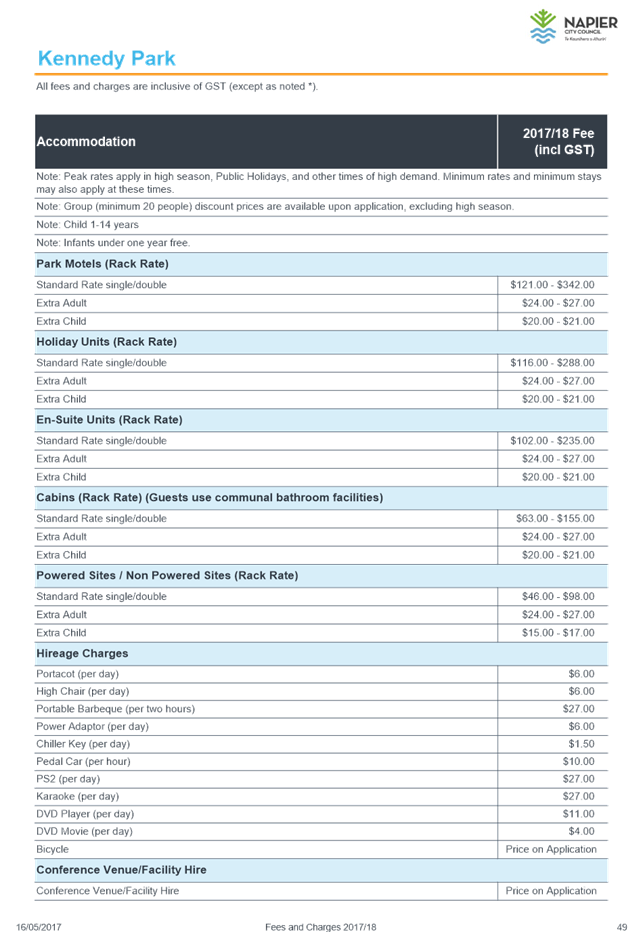

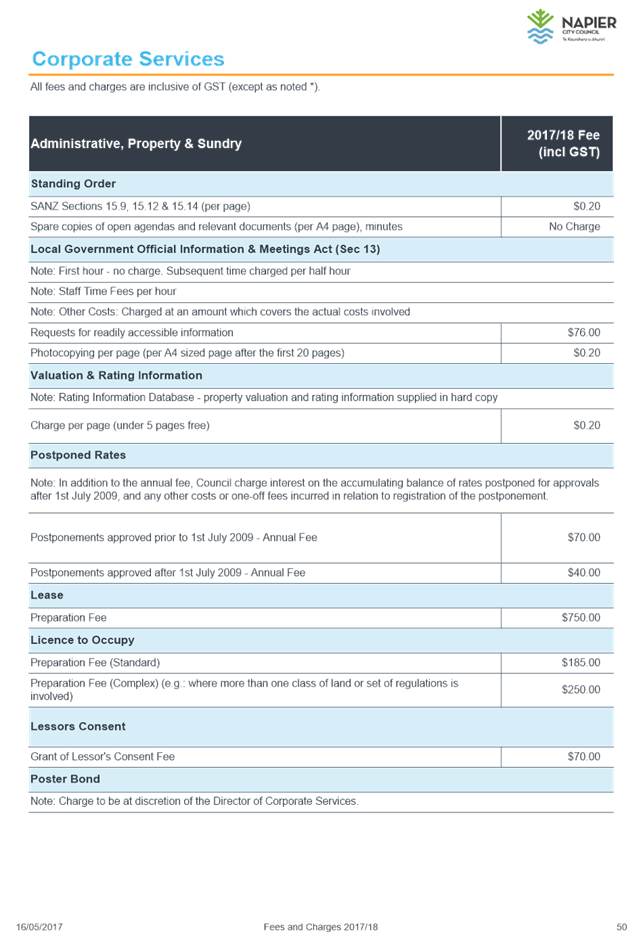

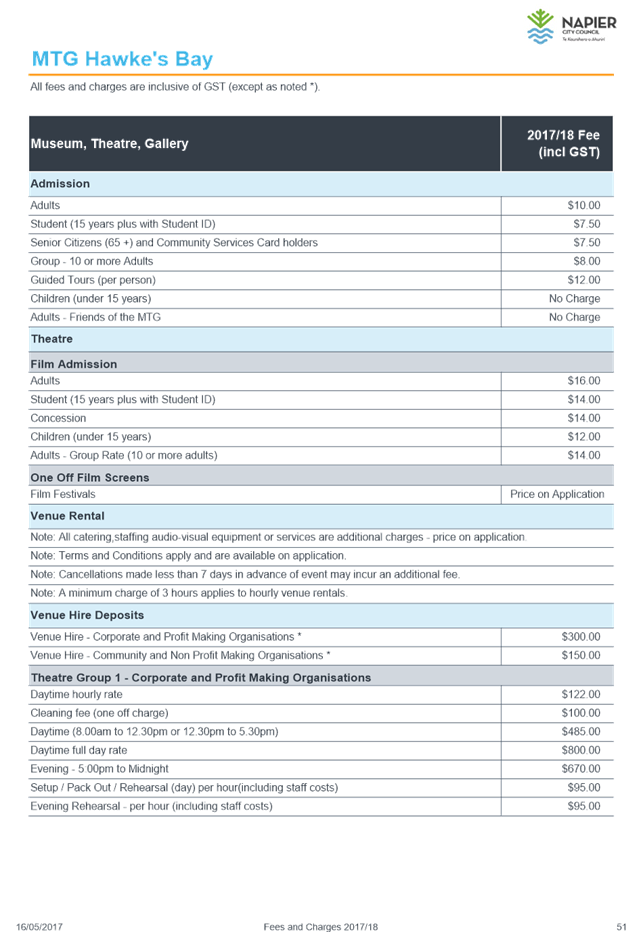

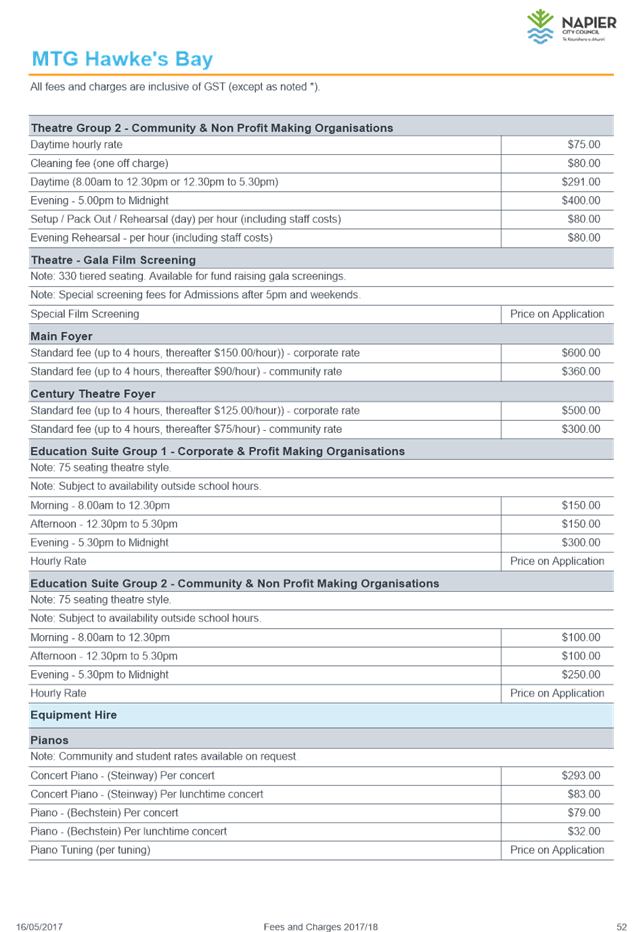

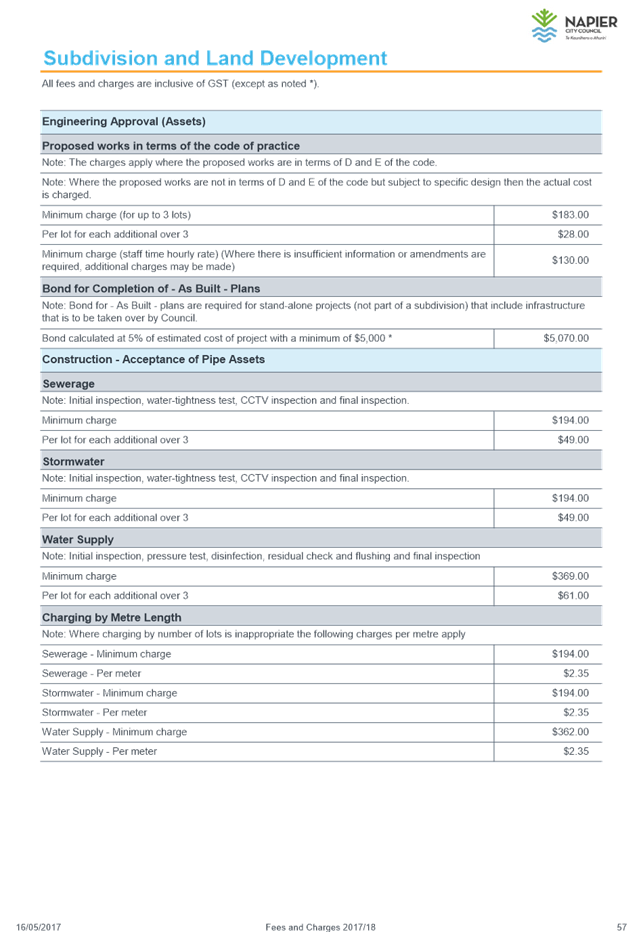

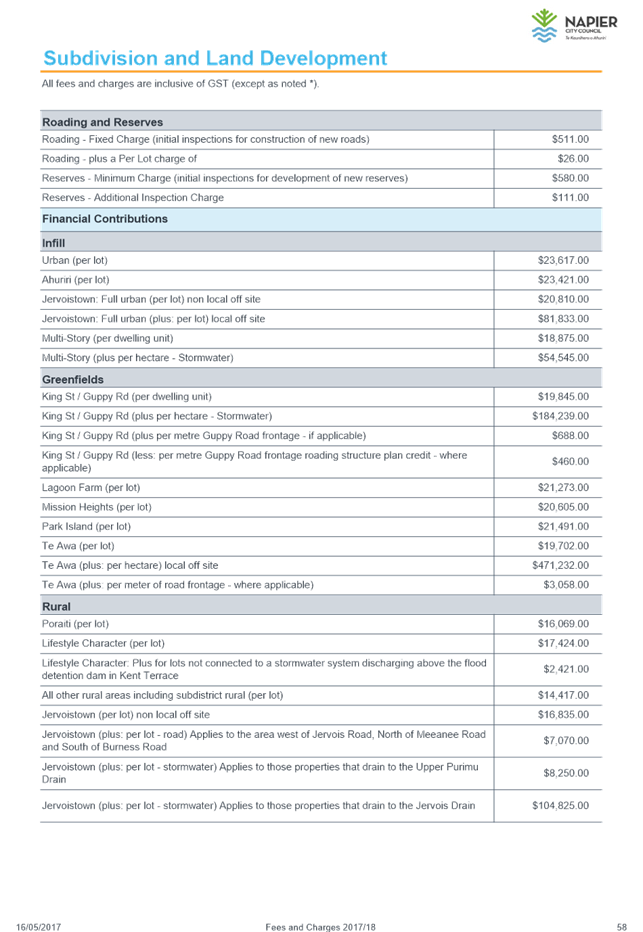

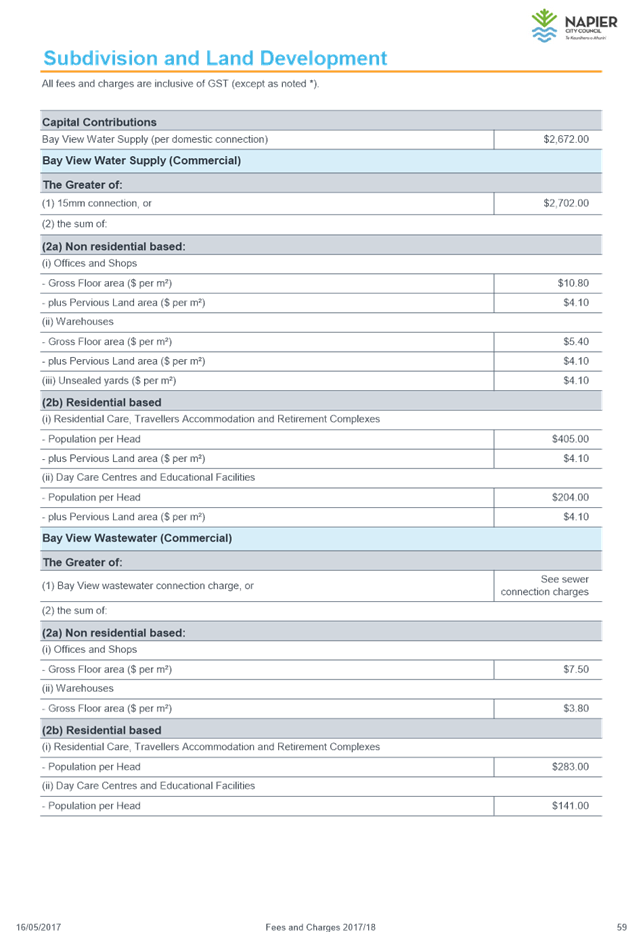

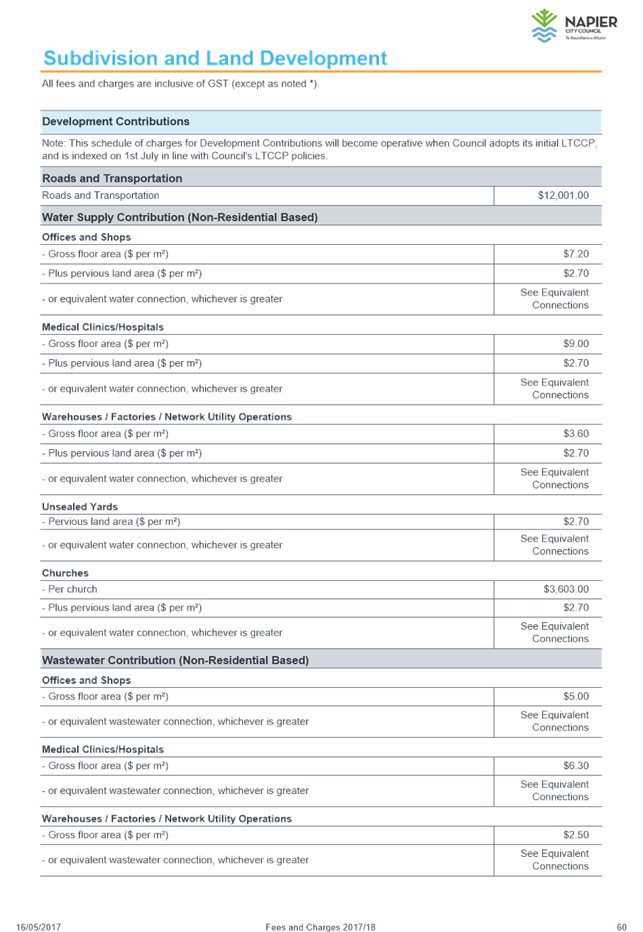

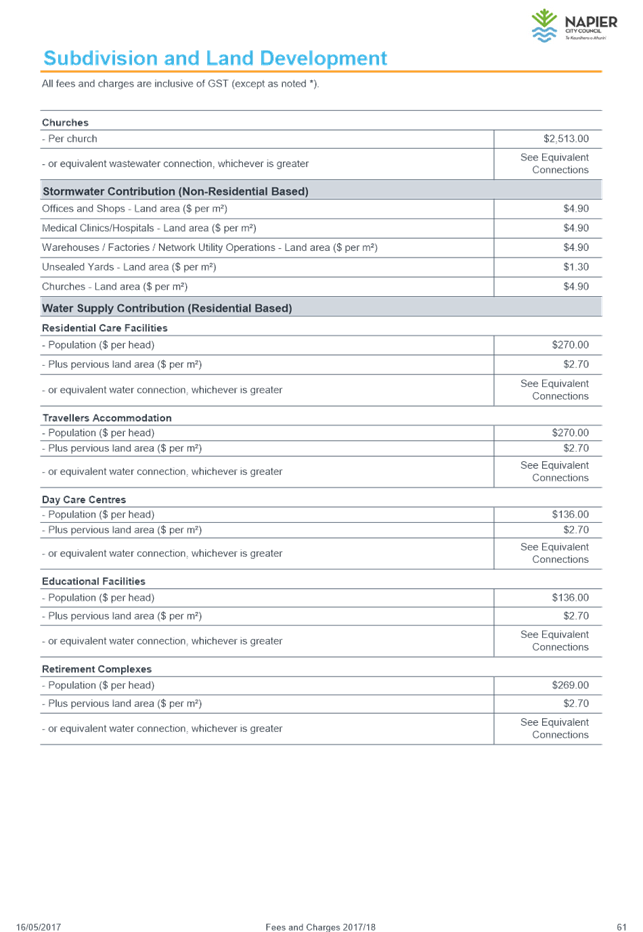

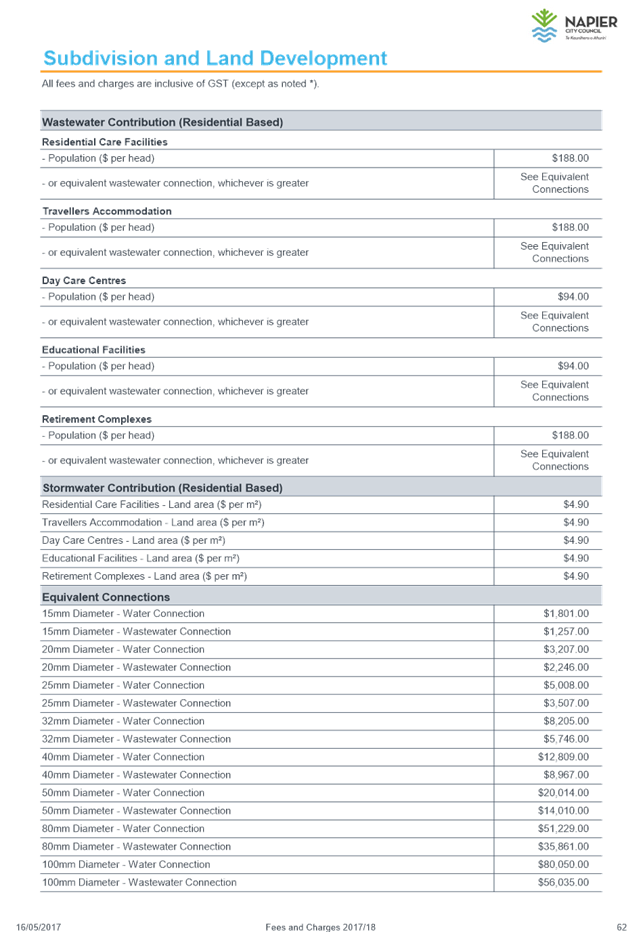

2. Fees

& Charges 2017/18

|

Type of

Report:

|

Operational

|

|

Legal Reference:

|

Local

Government Act 2002

|

|

Reporting

Officer/s & Unit:

|

Caroline

Thomson, Chief Financial Officer

|

2.1 Purpose of Report

To approve Fees and Charges for

the year commencing 1 July 2017.

|

Officer’s Recommendation

That Council

a. Adopt the Schedule of

Fees and Charges for 2017/18.

Note

that once the Schedule of Fees and Charges for 2017/18 has been adopted,

it will form part of the supporting information for the 2017/18 Annual

Plan.

b. Resolve

that a DECISION OF COUNCIL is required urgently to allow for notification

of the Schedule in advance of it becoming effective on 1 July 2017.

c. This will require the

following resolution to be passed before the decision of

Council is taken: That, in terms of Section 82 (3) of the Local Government

Act 2002. That the principles set out in that section have been observed

in such manner that the Napier City Council considers, in its

discretion, is appropriate to make decisions on the recommendation.

|

|

MAYOR’S RECOMMENDATION

That the Council resolve that the

officer’s recommendation be adopted.

|

2.2 Background Summary

Council at its

meeting to adopt the draft Annual Plan 2017/18 resolved to seek feedback on the

proposed Fees and Charges for the Council activities for 2017/18 on the Council

website by 30 April 2017. No feedback from the public was received

through this process.

The Schedule of

Fees and Charges is to take effect from 1 July 2017.

The schedule

was updated in the Draft Fees and Charges schedule for consultation to

incorporate changes to the existing scale of fees and charges, and any new

charges that have been approved by Council during 2016/17.

Where

appropriate all charges have been rounded to the nearest 10 cents or whole

dollar in accordance with Council Policy.

2.3 Issues

Council at its

meeting on 5th April 2017 resolved to make the charging for parking

within the CBD consistent at $1 per hour and sought feedback from the public on

the draft fees and charges schedule by 30th April 2017.

The fees and

charges schedule was made available on Council’s website and no feedback

from the public has been received.

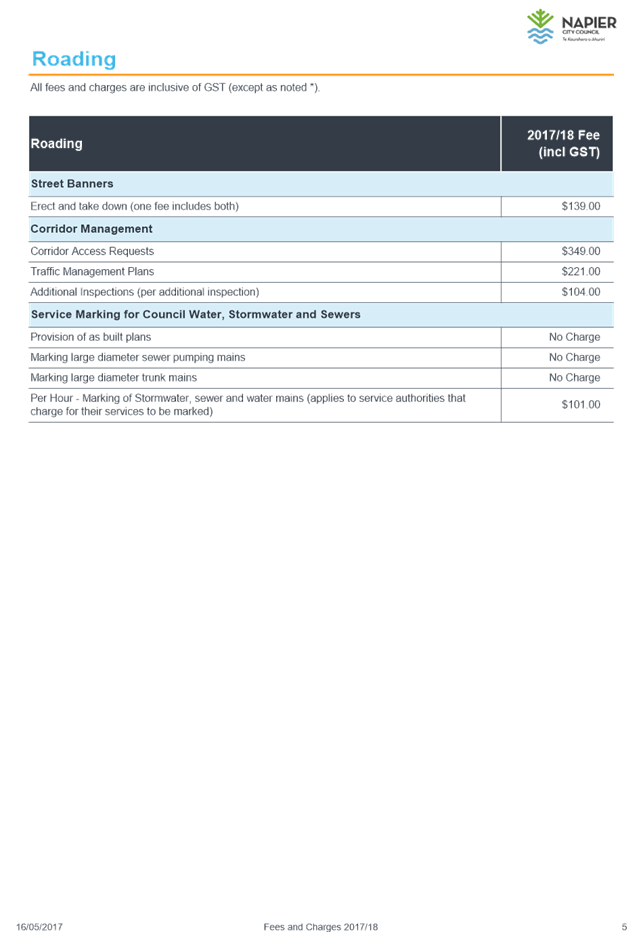

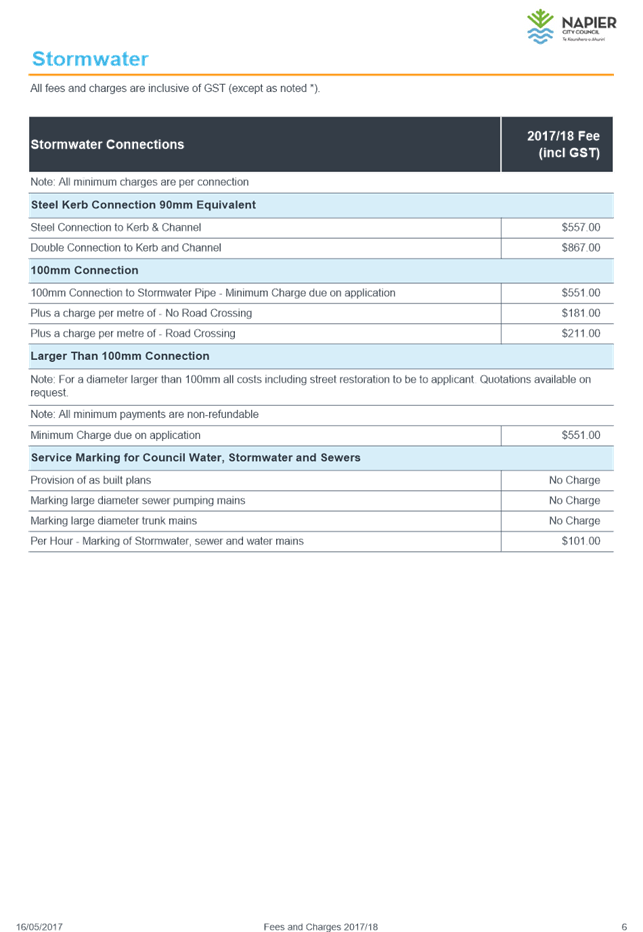

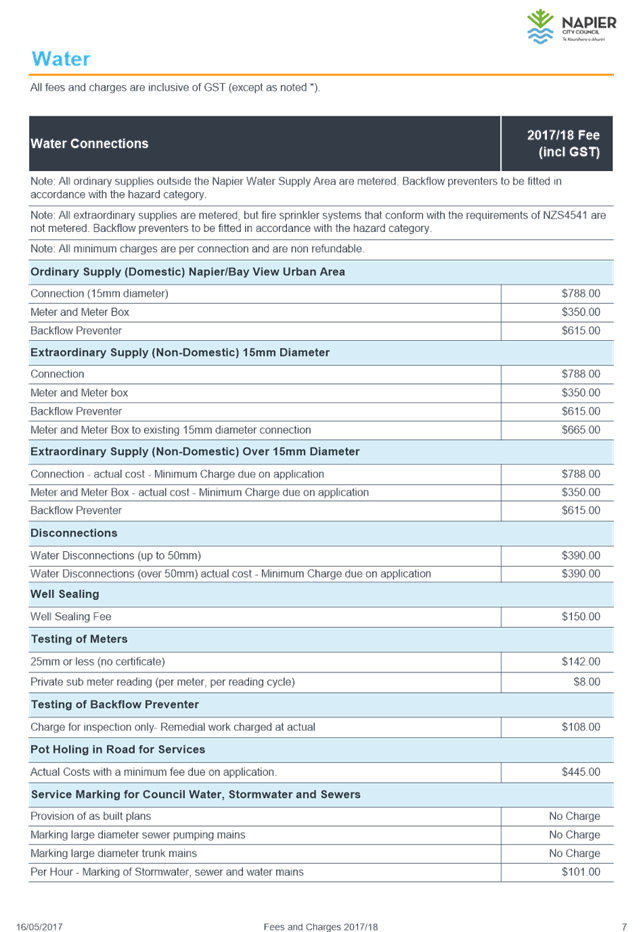

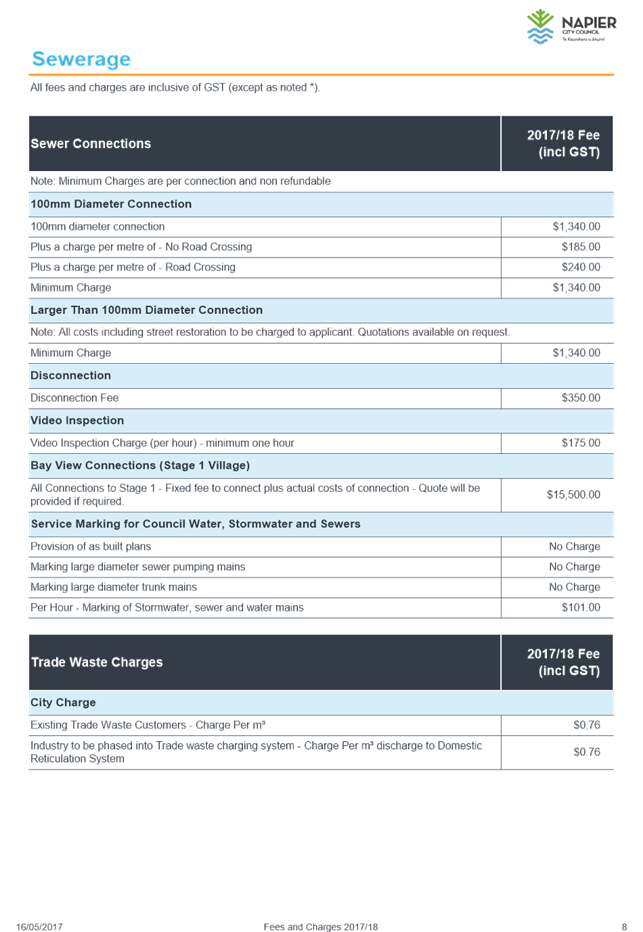

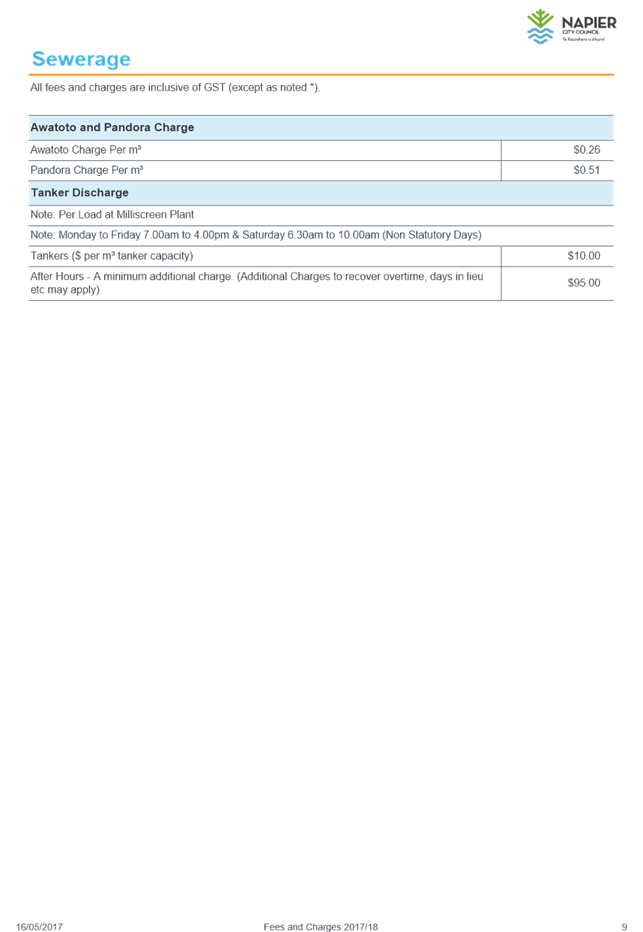

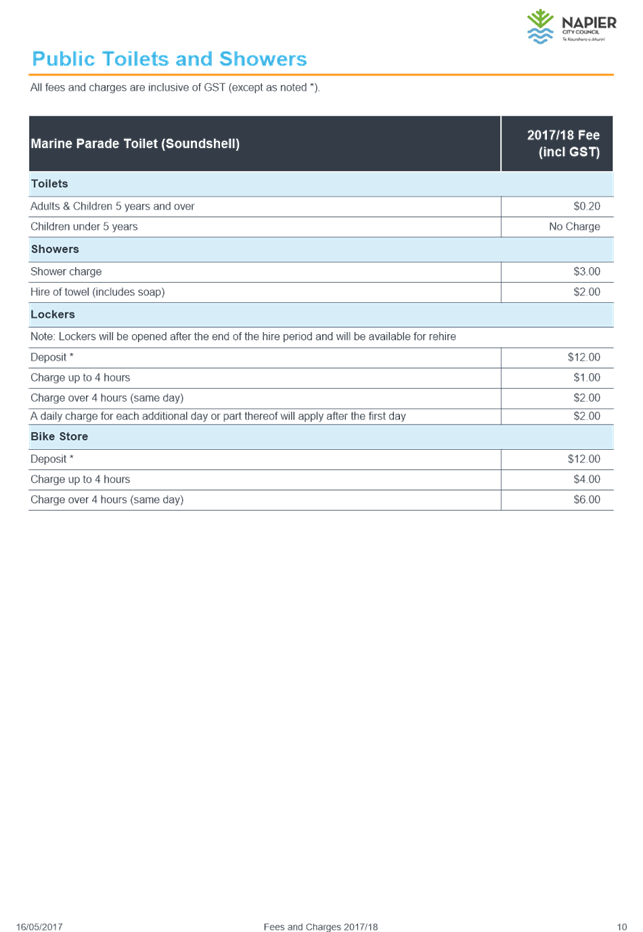

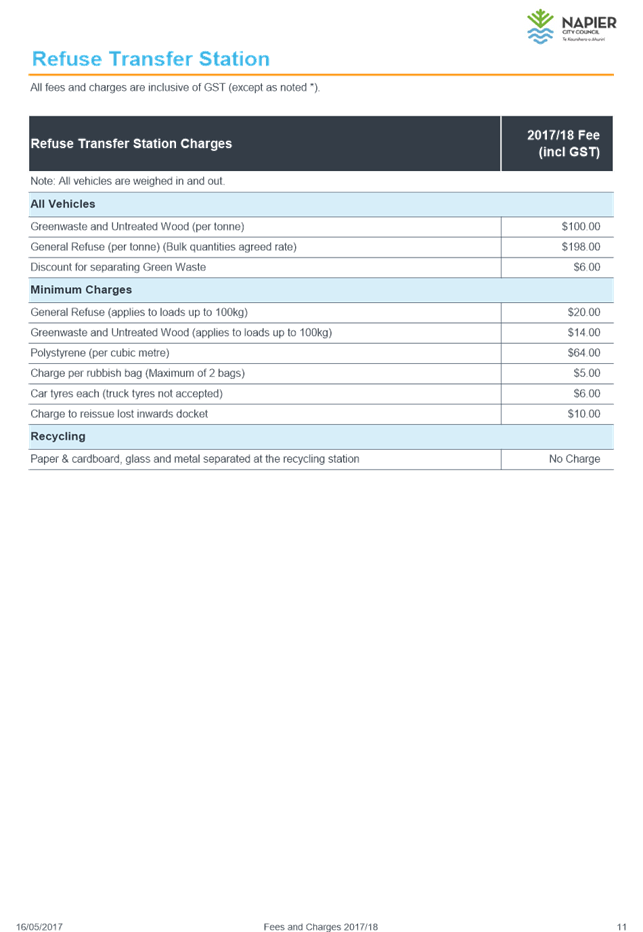

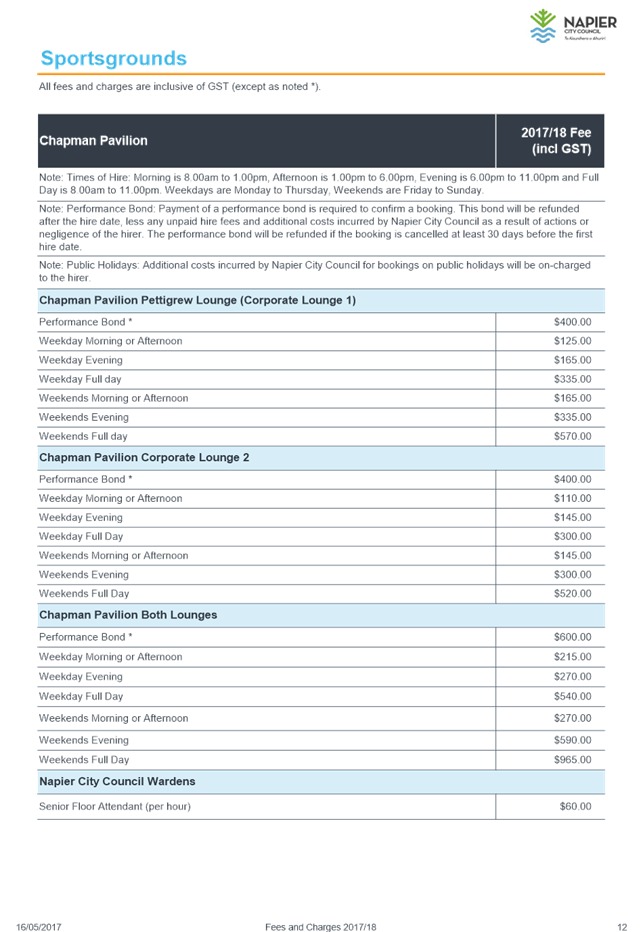

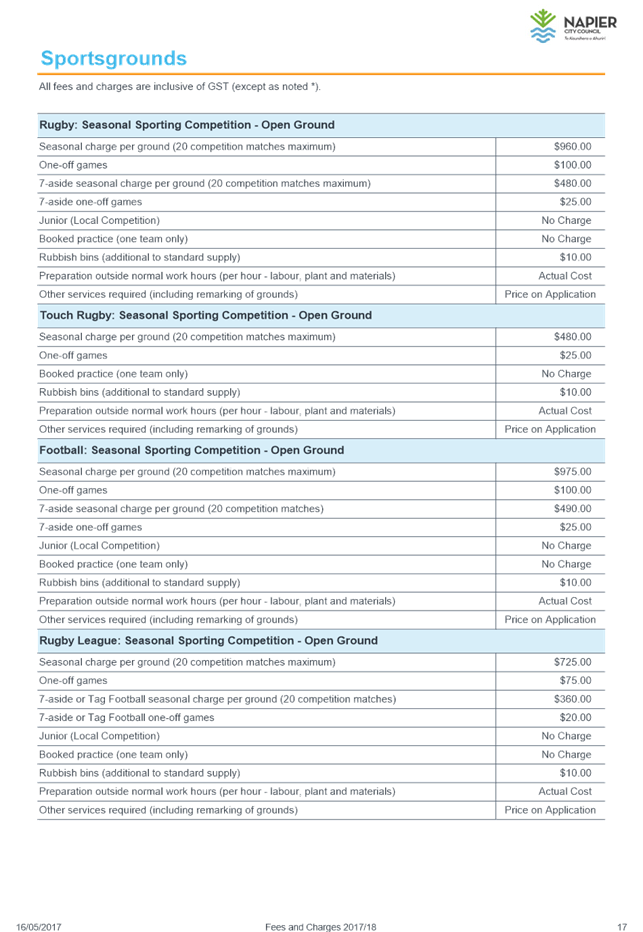

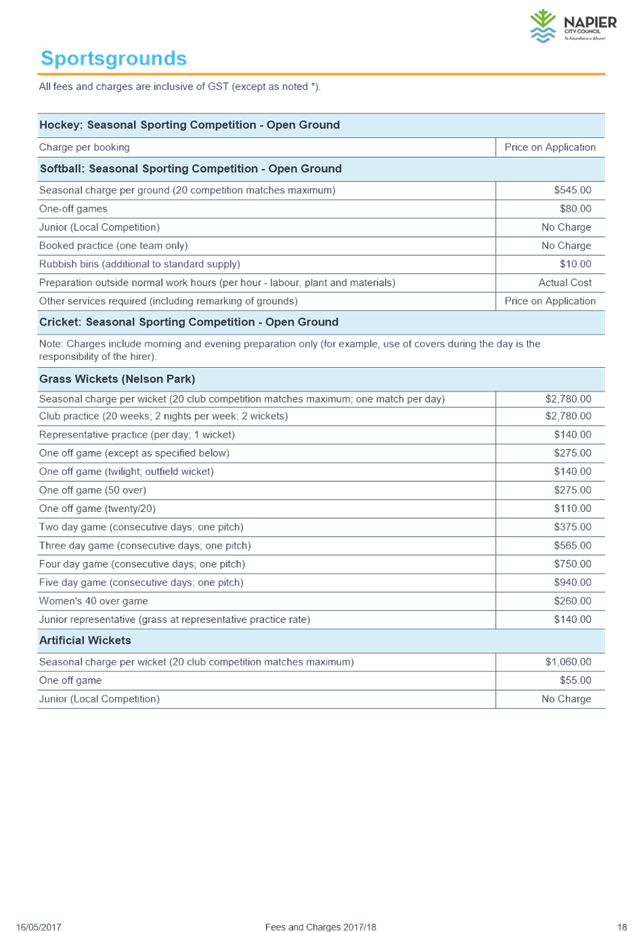

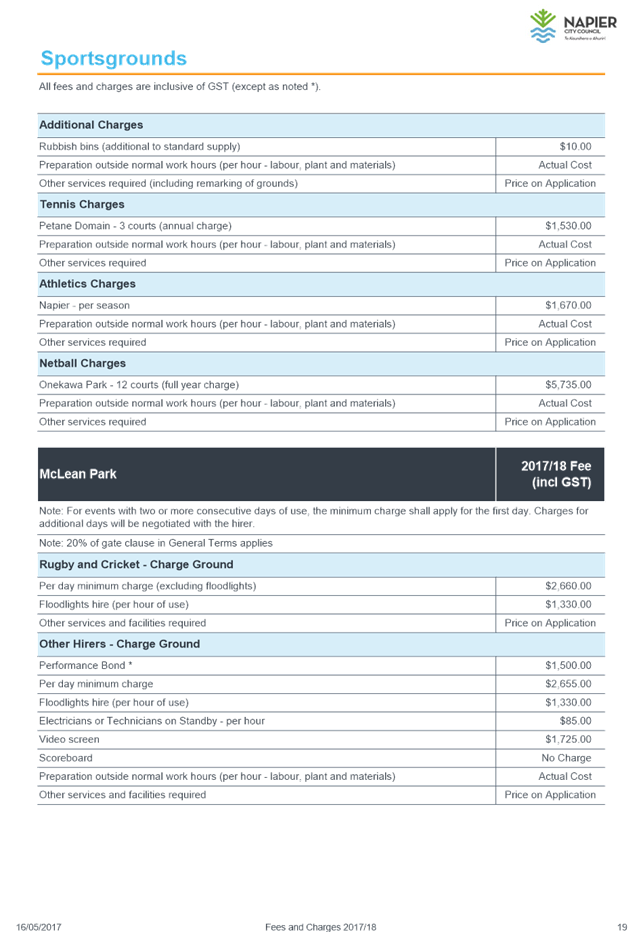

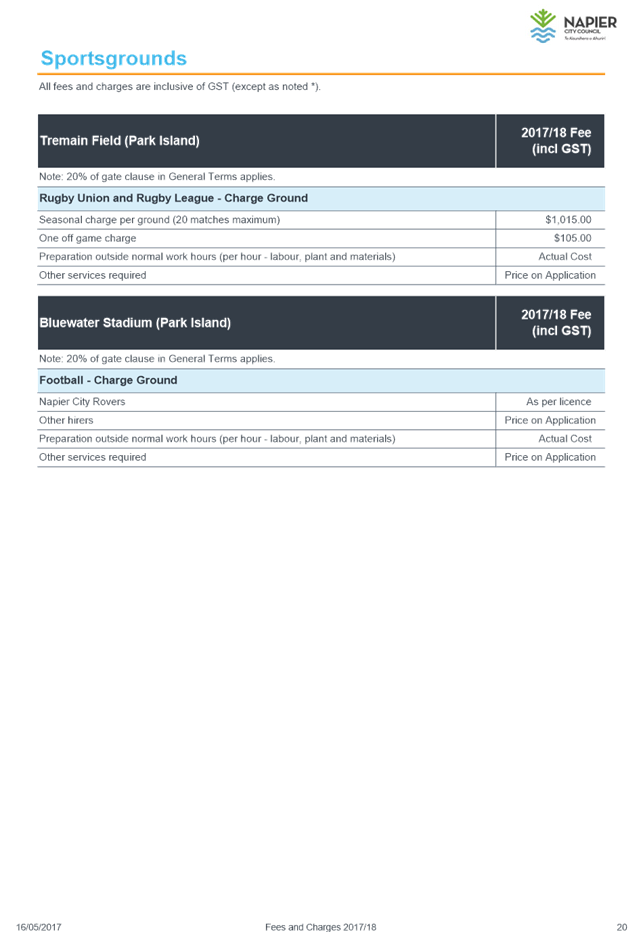

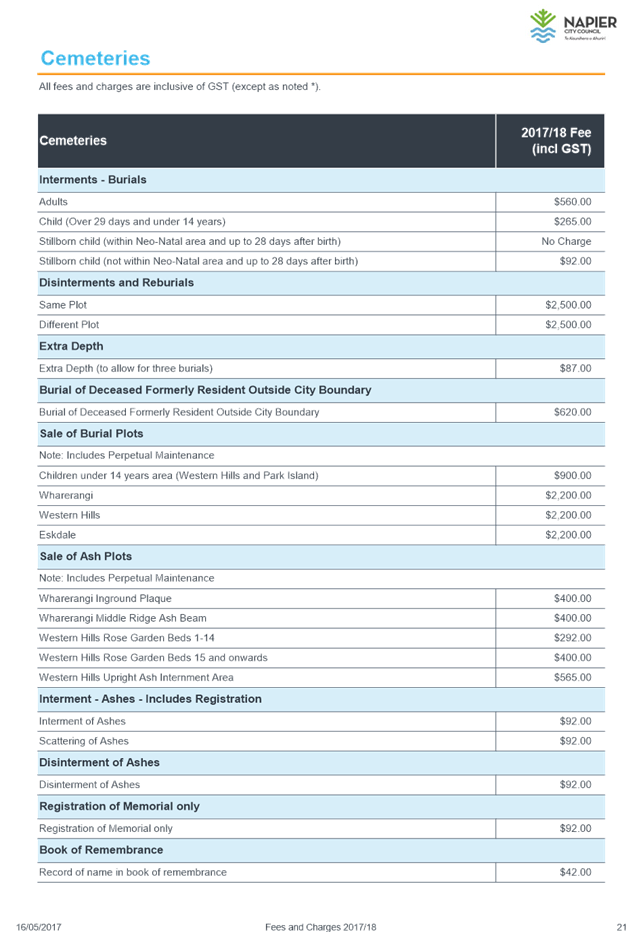

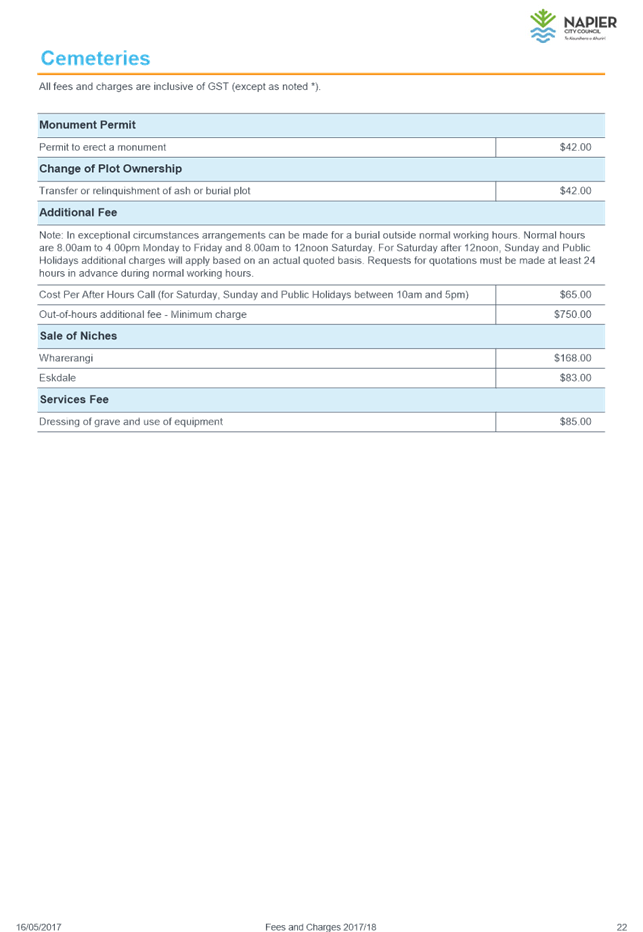

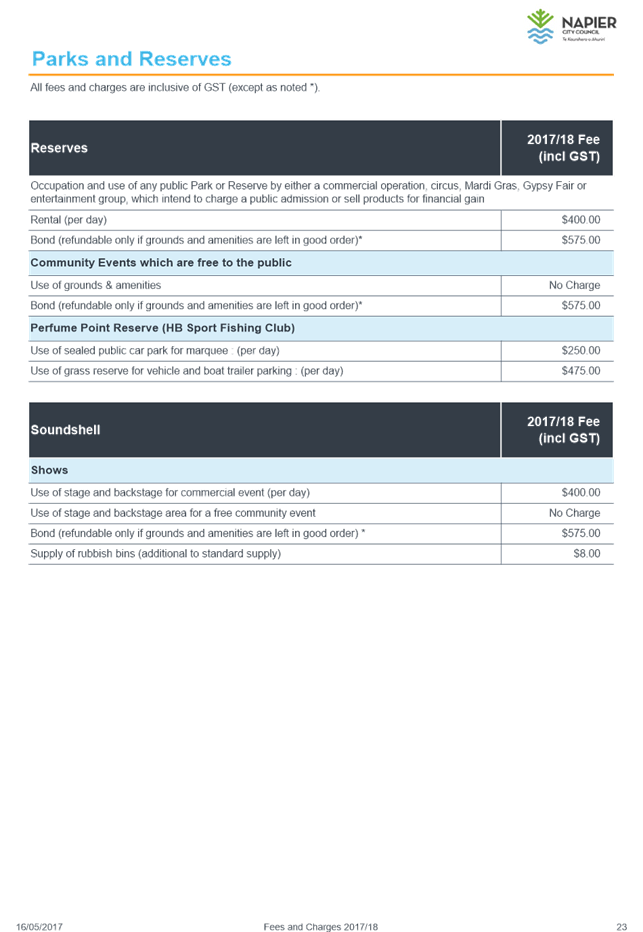

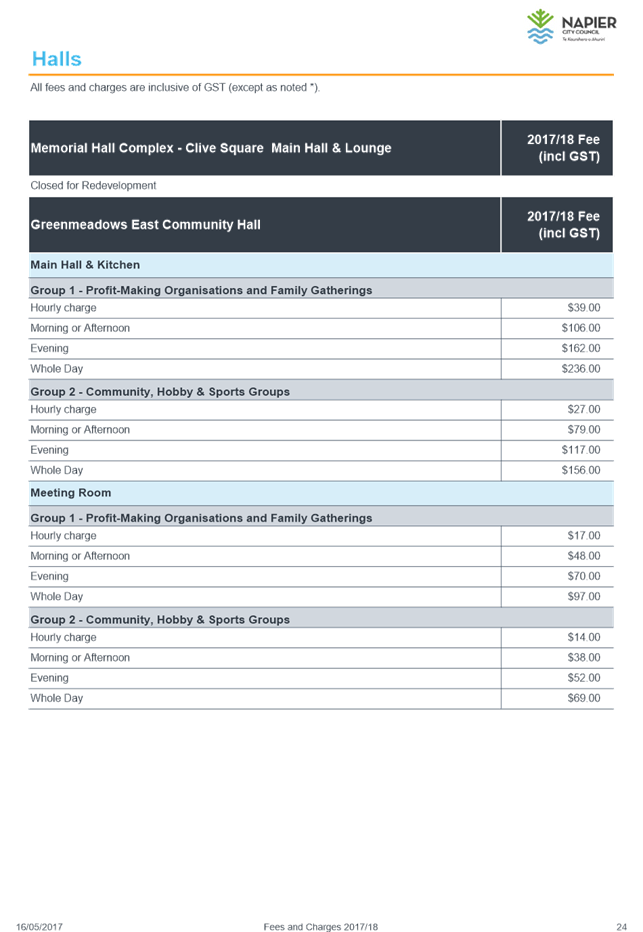

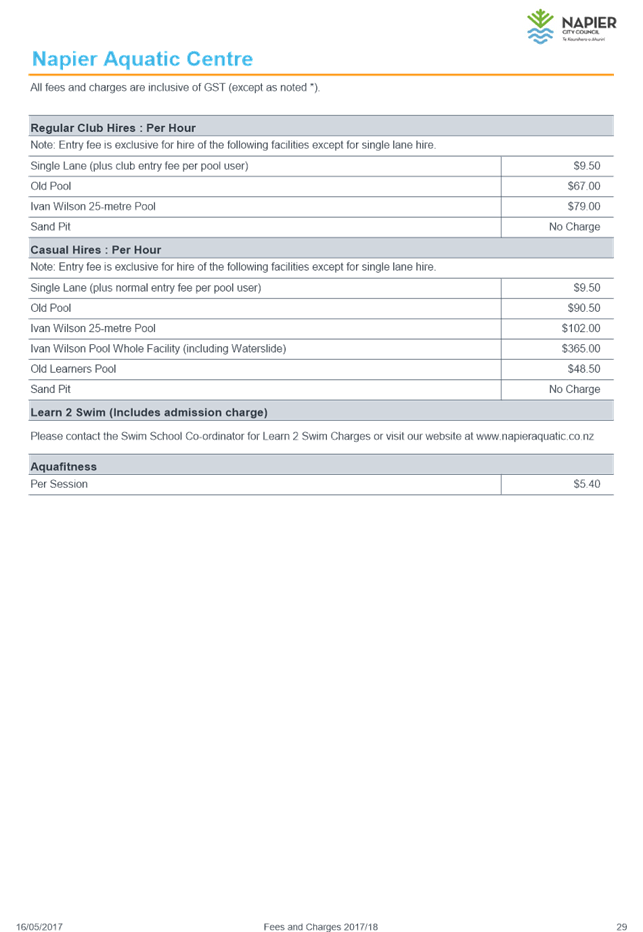

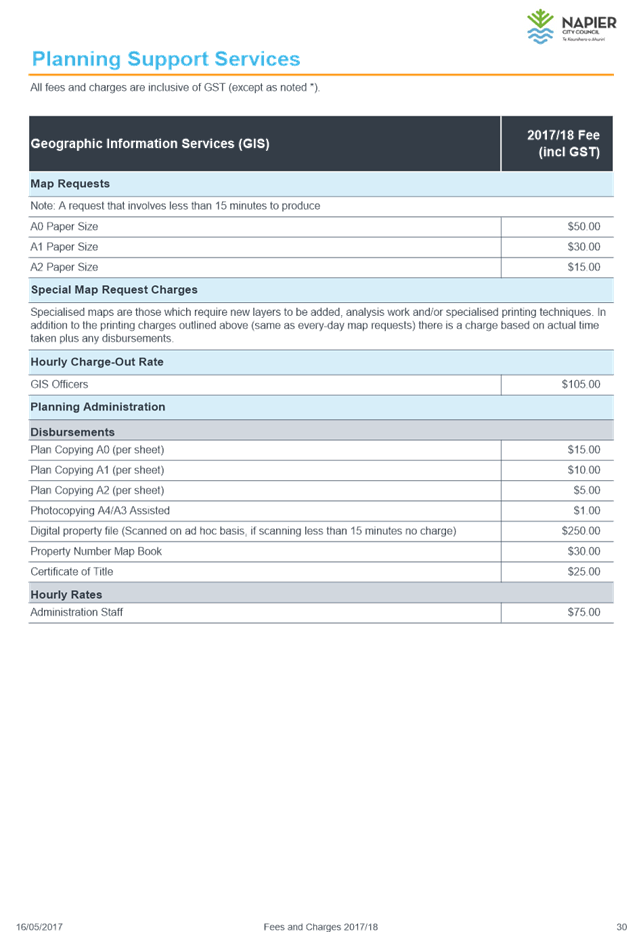

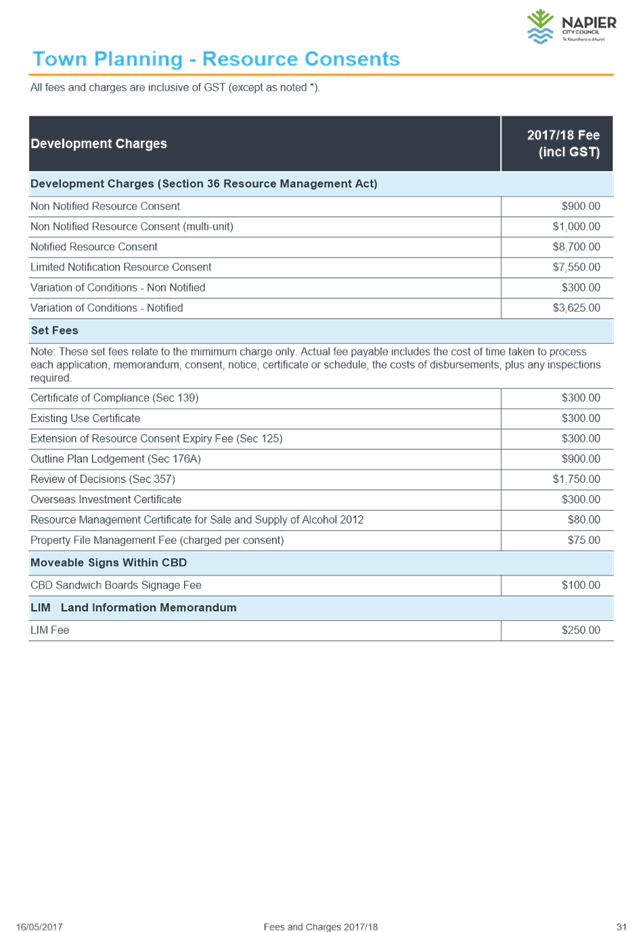

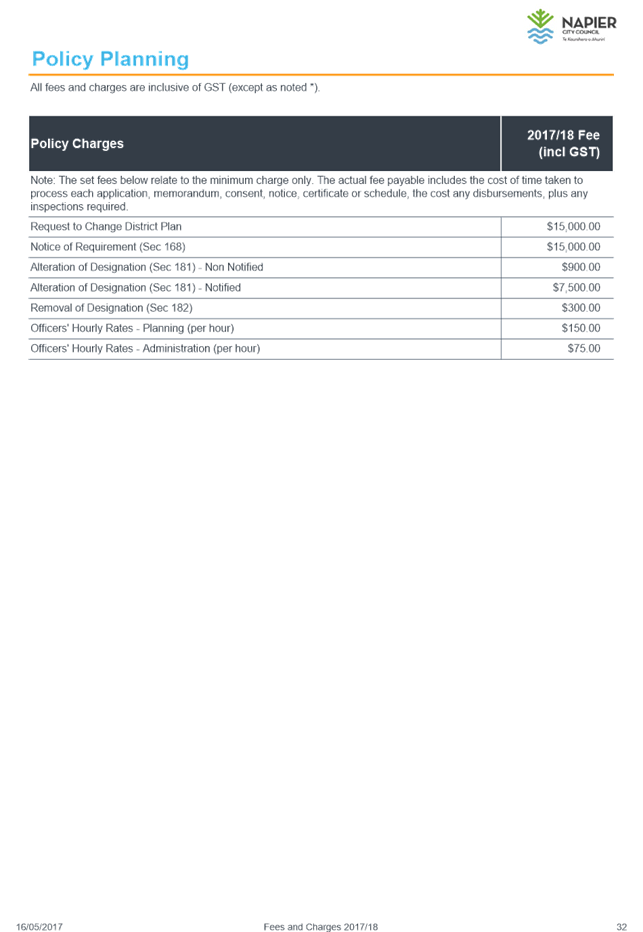

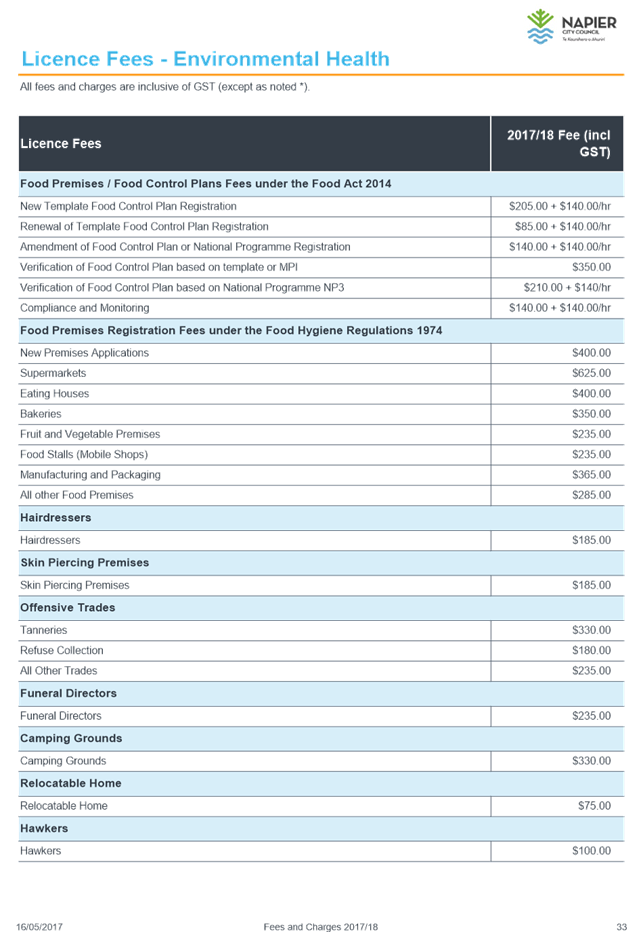

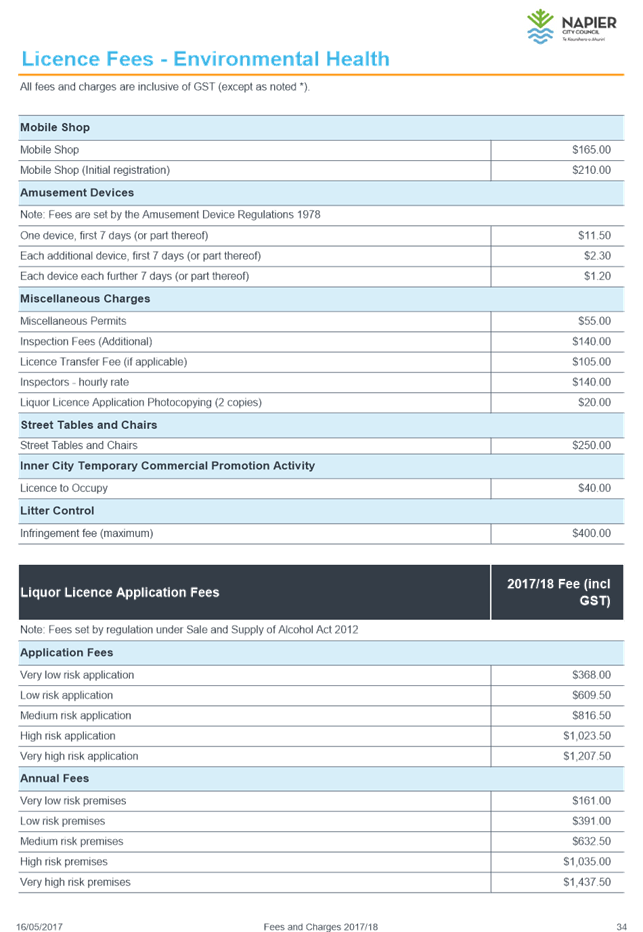

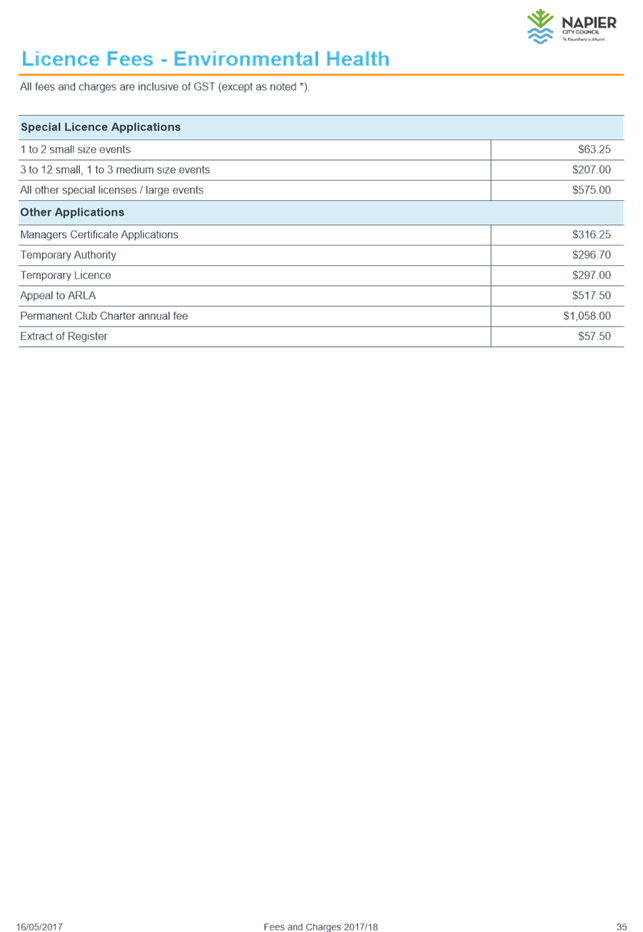

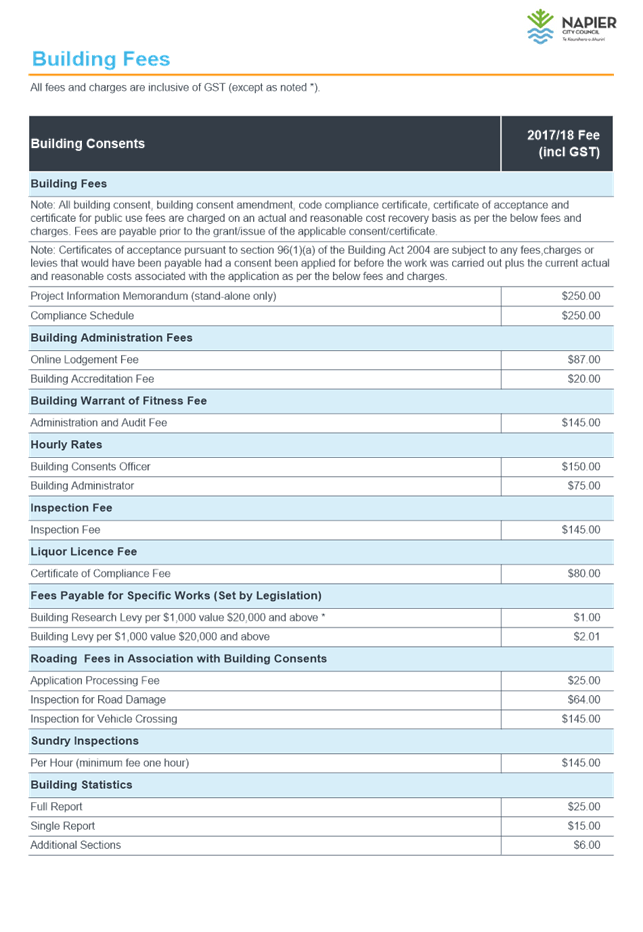

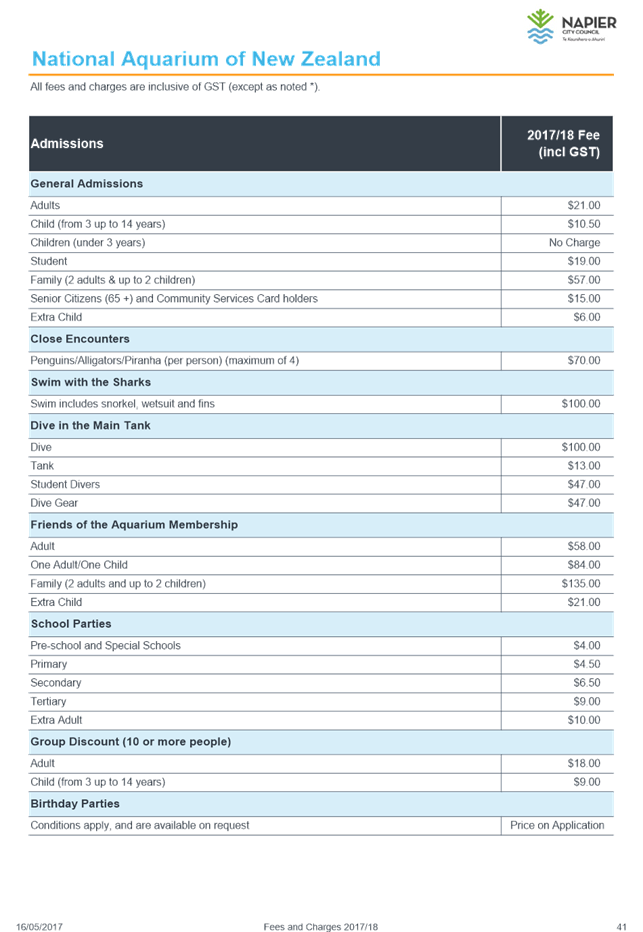

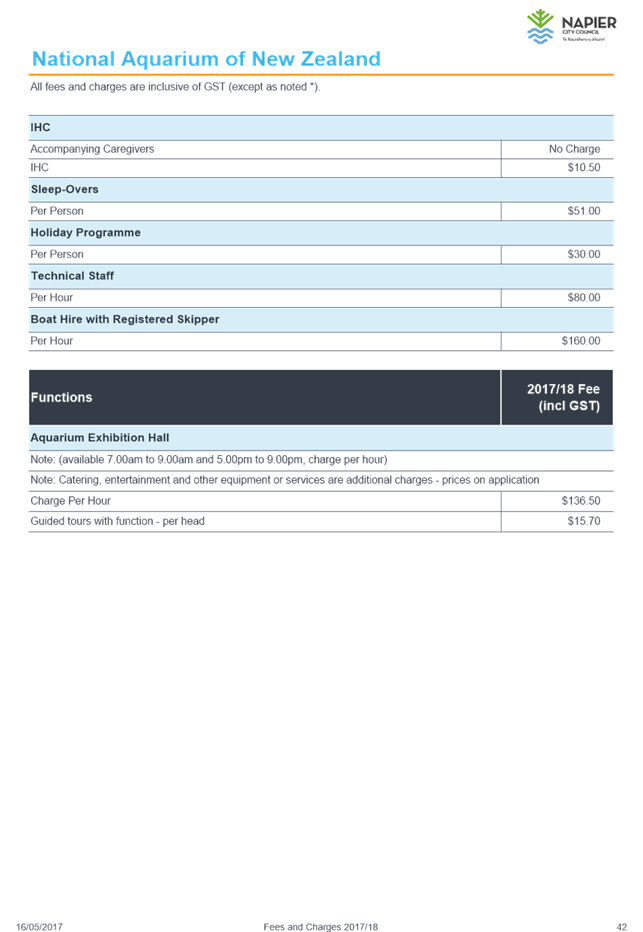

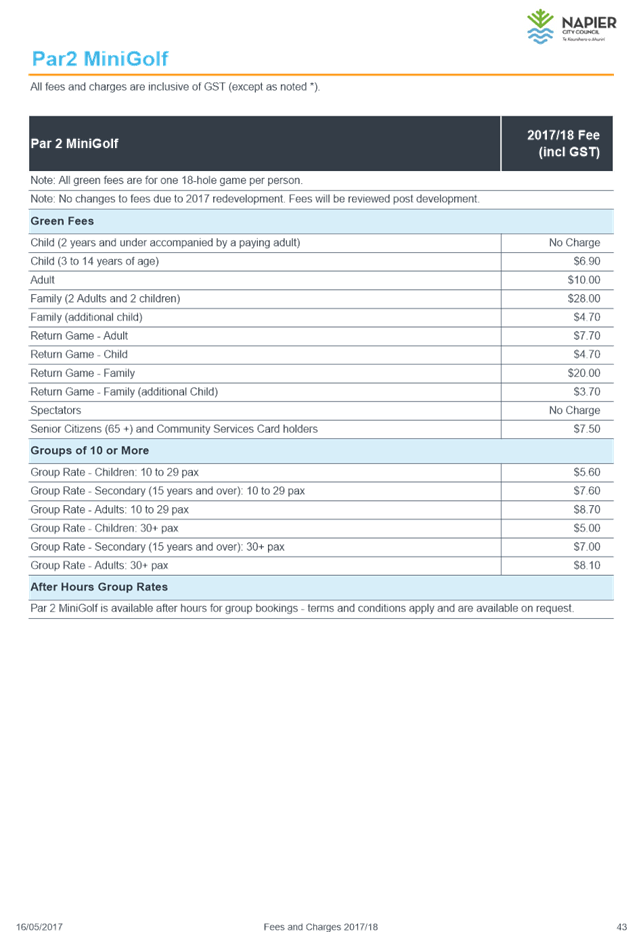

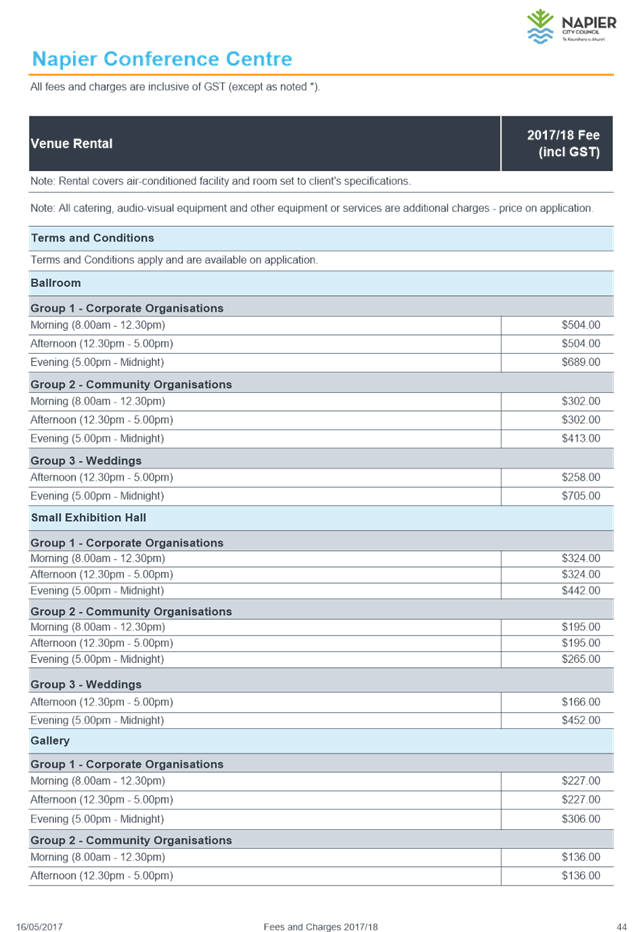

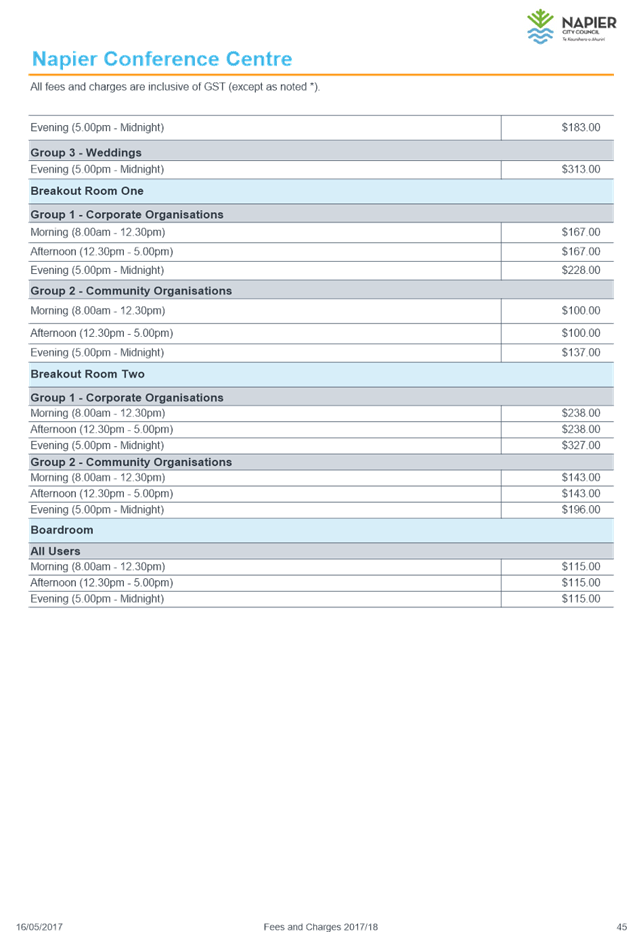

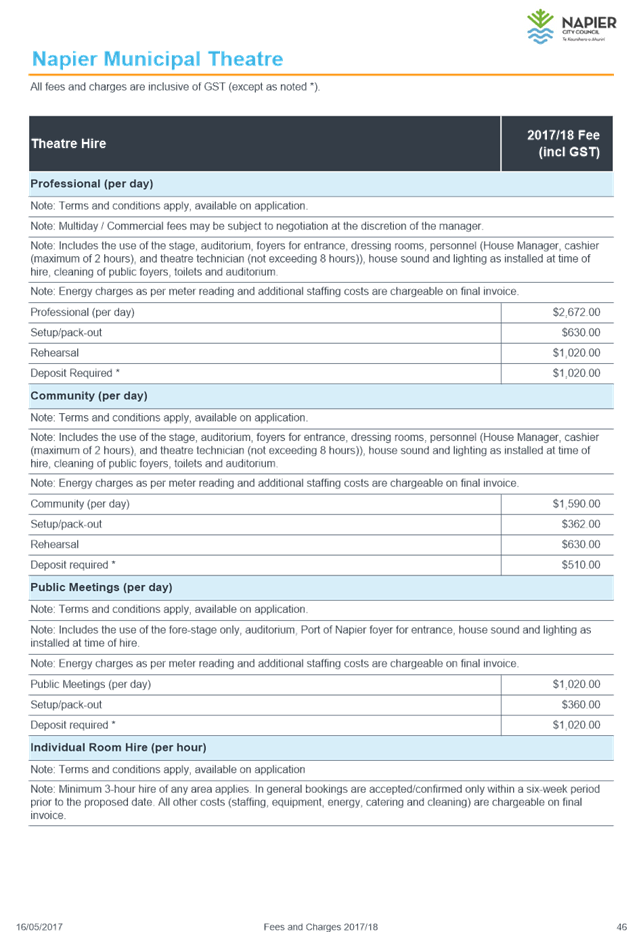

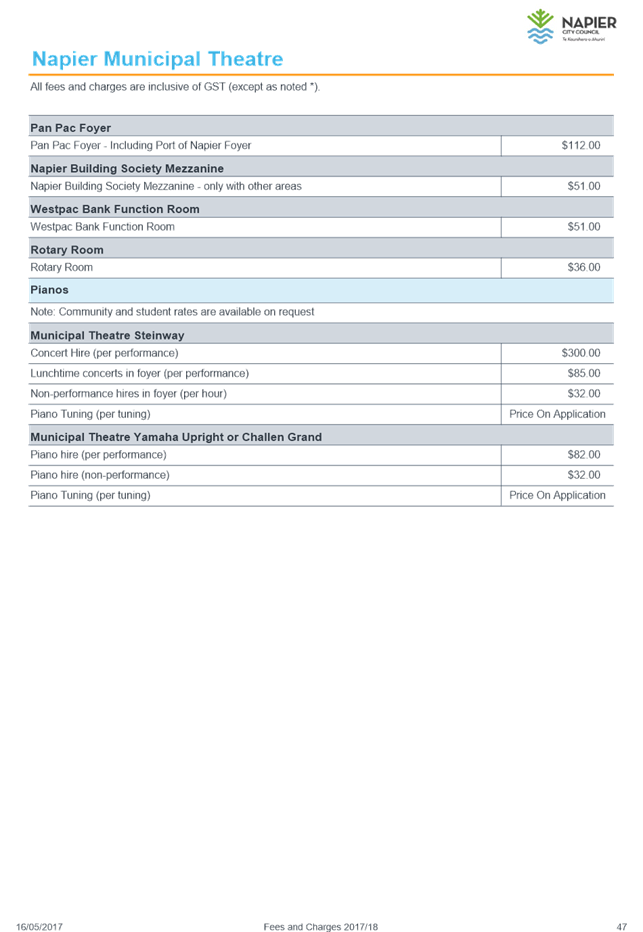

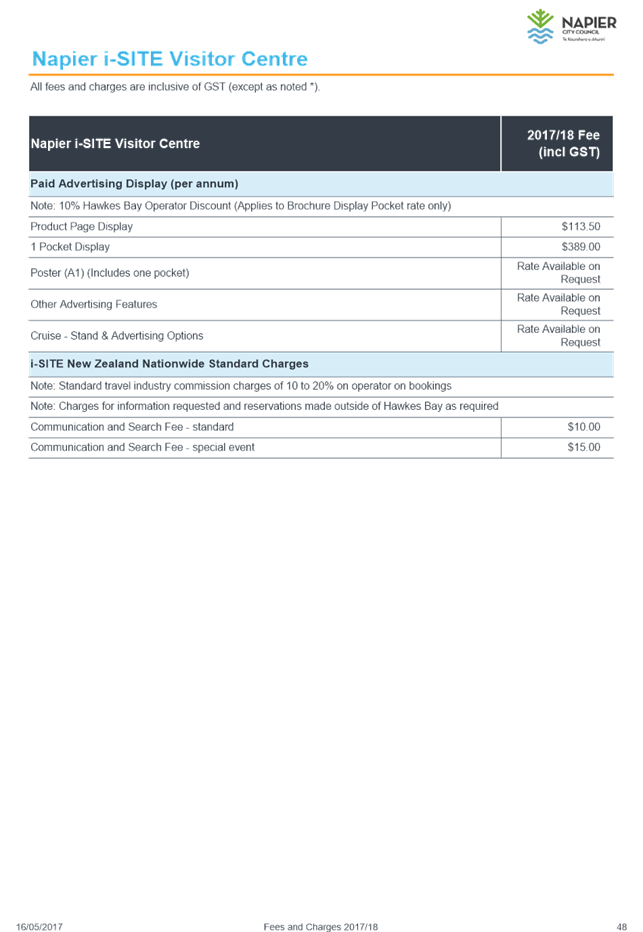

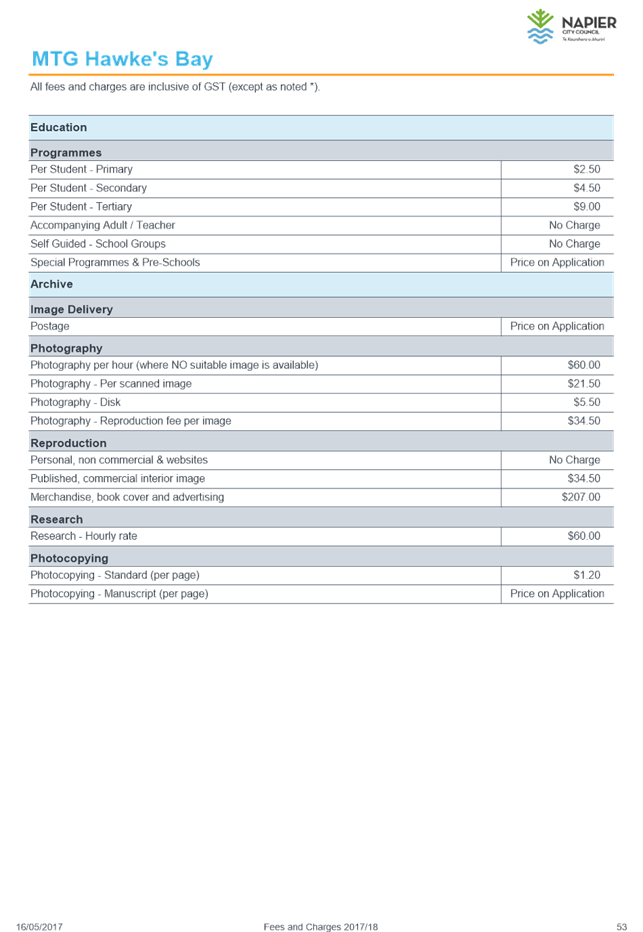

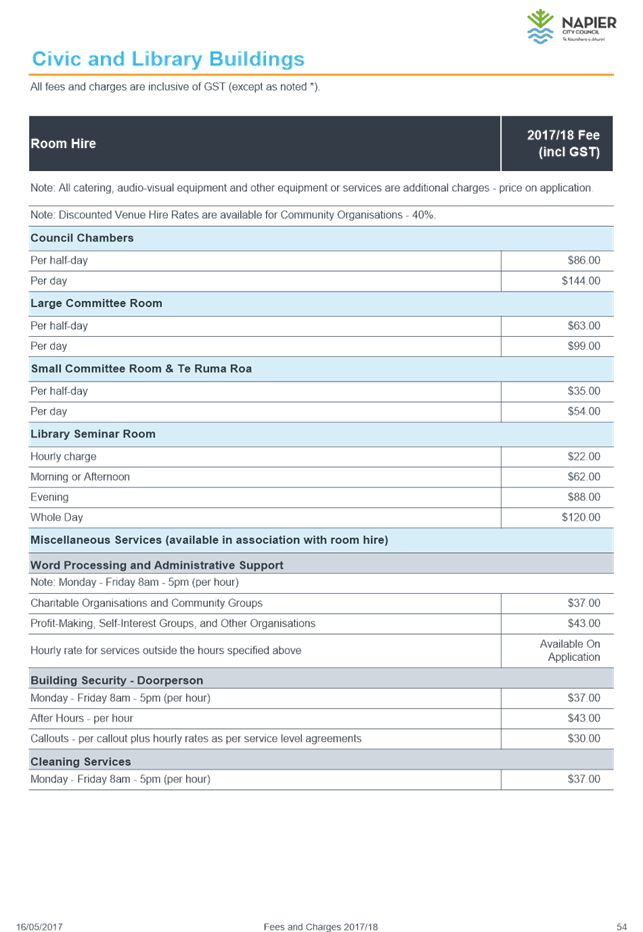

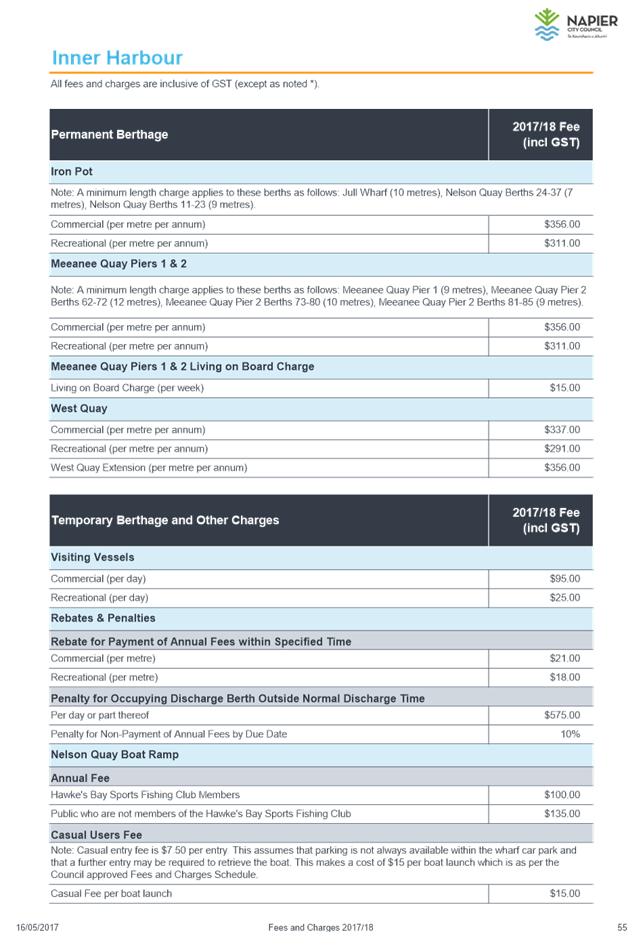

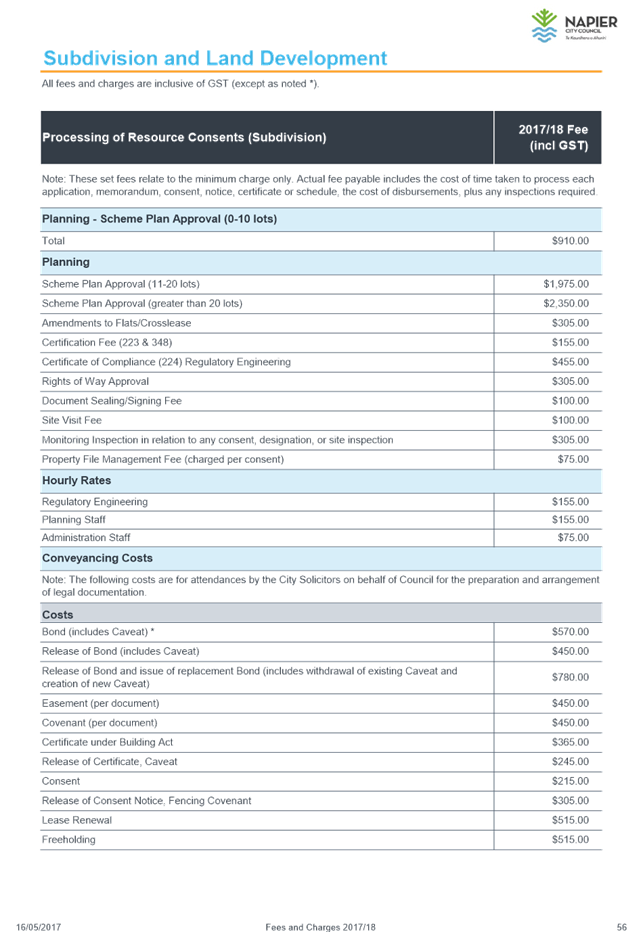

2.3 Attachments

a NCC

Schedule of Fees and Charges 2017/18 ⇩

Finance Committee – 14 June 2017 – Open Agenda

Finance Committee – 14 June

2017 – Open Agenda

3. Section

17A Review Work Programme Plan

|

Type of

Report:

|

Legal and

Operational

|

|

Legal

Reference:

|

Local

Government Act 2002

|

|

Document

ID:

|

356245

|

|

Reporting

Officer/s & Unit:

|

Rachael

Horton, Manager Business Excellence & Transformation

|

3.1 Purpose of Report

The purpose of

this paper provide Council with an update on the progress of the Local

Government Act (2002) Section 17A service delivery reviews

|

Officer’s

Recommendation

That Council

a. Note

that Local Government Act Section (2002) 17A of the Local Government Act

places an obligation on local authorities to routinely review their services

for cost effectiveness.

b. Note

the timeframe for the reviews Napier City Council will undertake.

c. Endorse

the proposed schedule of Section 17A reviews.

|

|

MAYOR’S/CHAIRPERSON’S RECOMMENDATION

That the Council resolve that the

officer’s recommendation be adopted.

|

3.2 Summary

In 2014 changes to legislation were made

with the introduction of section 17A of the Local Government Act

(‘LGA’) which placed an obligation on local authorities to

routinely review their services for cost effectiveness.

Clause 1A of the schedule requires

councils to complete reviews of all functions other than those covered by the

exceptions within 3 years of the enactment of the Local Government Act (by 8

August 2017). The section provides for exceptions including being

satisfied that the potential benefits do not justify the cost of the

review.

All NCC activities were assessed for

review. Out of 71 activities, 27 aggregated services are required to be

reviewed under section 17A.

Each review was

prioritised against a set criteria to ensure those services with the greatest

opportunity for improvement were reviewed first, and that resources are managed

across all work programmes. Reviews are scaled to match the size of the

service, the issues and anticipated benefits.

3.3 What are 17A reviews?

Early in 2012, government announced a

programme of local government reform entitled Better Local Government. A number

of amendments to the legislative framework for councils were made, including,

in 2014, the introduction of section 17A of the LGA.

Section 17A places an obligation on

councils:

· to review the cost

effectiveness[1]

of current arrangements for providing local infrastructure, services and

regulatory functions at regular intervals. Reviews must be undertaken when

services levels are significantly changed, before current contracts expire, and

in any case not more than 6 years after the last review. The LGA has a

transitional provision that requires all services to be reviewed by 8 August

2017; and

· to ensure that there

is a binding contract or agreement where delivery of infrastructure, services,

or regulatory functions is to be undertaken by a different entity than the

entity responsible for the governance of those things. The

contract/agreement must cover key matters such as service levels, performance

assessment and reporting, risk management and accountability.

A review should

consider three elements: how a service is governed, how it is funded, and how

it is delivered. The intent of the legislation is to encourage

efficiencies as well as collaboration between councils. Reviews provide

an opportunity to improve the delivery of services to our residents, ratepayers

and visitors.

3.4 NCC’s approach to 17A reviews

The LGA Section 17A was enacted 8 August

2014, with a period of three years to complete the first set of reviews.

During September 2015, Hawkes Bay

underwent an Amalgamation Poll where the proposal was to amalgamate all five

Councils in the Region. The turnout rate for this Poll was high with

approximately 80% of Napier residents voting against amalgamation.

Overall the proposal was defeated, ratepayers had shown they were satisfied

with the current service provision of NCC.

As a result, any significant progression

within NCC was put on hold, including the 17A programme. It was

determined that there was no cost benefit in undertaking reviews during this

time given the significant change being proposed.

Following the poll, the next stage was to

review the organisation structure to ensure it was appropriate for the delivery

of current and future services.

This review was, in effect, the start of

the 17A work programme. Without a clear structure in place the

effectiveness of further 17A review work would be undermined.

The review followed a logical and

structured approach and resulted in the implementation of a new management

structure and leadership framework to deliver our services.

The new structure has strengthened

NCC’s approach to service delivery within each Directorate:

· The City Strategy

Directorate is leading, coordinating and integrating

strategies across NCC, looking ahead for the City and bringing together all

related thinking and planning.

· Community Services

Directorate is bringing a coordinated approach to community strategies and

programmes, business operations, and the use of associated facilities to

improve service to customers.

· The Infrastructure

Directorate is strengthening strategic decision making around assets, and the

delivery of related activities, and reinforced NCC’s commitment to environmental

sustainability. A Project Management Office was established to deliver the

capital programme.

· The Corporate Services Directorate established the Business

Excellence and Transformation team, with the primary focus of leading and

supporting best practice within Council. This team will continue the 17A

work with a programme of reviews over the next three years, and on a six year

cycle.

In addition to the review of NCC’s

management structure, we have also completed the following reviews:

· Waste Futures –

joint project with Hastings regarding the options on the treatment of waste in

the region

· Internal Audit Services

– regional collaboration for procurement of services

· Lagoon Farm – review

of service delivery model

· Cleaning services – consolidation

of council services

· After Hours Call Services

– review of service delivery, resulting in a contract to Palmerston North

City Council for service provision

· Shared web services

provided by Napier for 4 councils with approval for last Council to begin

services shortly

· Provision of shared HR

services to Wairoa Council

· Provision of shared

Economic Development resourcing with Central Hawkes Bay

· Bay Skate service

provision bought in house

· Review of service provision for Faraday Centre

3.5 The 17A work programme going forward

Following the establishment of the

Business Excellence and Transformation team, we are in a position to continue

our 17A reviews under a more formal work programme.

Over the next three years, we are

proposing a common sense approach that balances the need to comply with

legislation with the need to carefully manage NCC’s operational

resources. This approach would ensure a focus on reviewing services with

the most significant opportunities for improvement first.

At the scoping

phase, the review will be scaled to match the size of the service and the

issues and opportunities presented by the review. Elected members will be

asked to provide political direction early to individual reviews as

appropriate.

NCC’s approach to 17A reviews is

based on the following objectives:

· To maximise opportunities

to improve the delivery of services to our residents, ratepayers and visitors

(including considering shared service opportunities with other councils).

· To prioritise NCC

resources to reviewing services and contracts with the greatest potential for

cost effectiveness gains.

· To scale the scope of the

review to match the size of the service and the issues and anticipated

benefits.

· To ensure compliance with

the legislation.

· To keep excellent records

of the decisions made and reviews undertaken to support the ongoing life of the

programme.

We will optimise and collaborate with the

reviews being undertaken by other Councils in the region where possible, and we

will be cognisant of central government lead legislation changes eg Havelock

Water Inquiry and potential impacts to the way in which we deliver

services. We will continue to work as a region through initiatives

identified through the Hawkes Bay Shared Services work programme.

3.5 What needs to be reviewed?

Section 17A

uses the same terminology as section 10 in the LGA, that is to say it refers to

the local infrastructure, local public services, and the performance of

regulatory functions. The focus is therefore on public-facing services.

Back-office services, such as IT, debt

collection (or other more transactional elements of the finance function) will

be addressed through internal business excellence initiatives and therefore do

not need to be considered within the 17A review programme.

There are two exceptions to reviews under

the legislation:

· Delivery arrangements that

are bound by legislation, contract or binding agreement so that they cannot be

changed within the next two years.

· If the local authority is

satisfied that the potential benefits do not justify the cost of the review.

In determining whether the potential

benefits justify the cost of the review, Officers have undertaken some analysis

in order to identify an appropriate point at which Council could consider not

undertaking reviews. We are of the view that that

any service, contract, or other agreement that has a total value of $500,000 or

less (total budgeted operational and capital expenditure) should not be

reviewed. In the absence of other factors (e.g. high probability of

significant savings, high public interest in the service), it will be assumed

that reviewing a service below this size is unlikely to generate savings that

outweigh the costs.

Once conducted a section 17A review has a

statutory life of up to six years. This means that each service must be

reviewed at least once every six years – unless one of the other events

that trigger a review comes into effect.

There are two statutory triggers for a

review under the legislation:

· When a local authority is

considering a significant change to a level of service[2].

· When a contract or other

binding agreement is within two years of expiration.

Decision to review

To determine which services require a

review, each service was assessed using the following criteria:

· Was the last service

review more than six years ago?

· Does the contract expire

in the next two years?

· Is a change in level of

service proposed?

· Does the potential benefit

of the review justify the cost of the review (total value <$500,000)?

· Can the contract (or other

agreement) be changed in the next six years?

· Is there any other reason

why the service review should not be undertaken?

NCC has approximately 72

activities. Applying the above criteria, 30 services fall within the

scope of the legislation. Some services have been combined for the

purposes of review, reducing the aggregated number of reviews to be undertaken

to 27. Please see Attachment 1 for a list of the 27 reviews to be

undertaken.

3.6 What are the priorities for review?

It is necessary to prioritise each review

in order to manage NCC’s limited resources and to ensure those reviews

with the greatest potential for improvement are reviewed first.

Reviews need to be decided and

prioritised on a six year cycle. However, it is likely that within that time

priorities will change as either triggers or exceptions to the legislation come

into effect arising from decisions of council, and/or operational management of

capital, assets and services. Therefore NCC will review the work

programme annually.

Regional collaboration is an opportunity

that may present itself as the individual reviews are undertaken, but as each

council has their own priorities and timeframes, it is not a driver for

prioritising reviews. Options for shared services will be included as part of

each review process.

Prioritisation of service delivery

reviews

To determine the priority of reviews,

each service was assessed using the following criteria:

· What issues or

opportunities have been identified (including opportunities for significant

savings, for shared reviews or shared services)?

· What is the impact of the

service?

· Is the service achieving

set or expected levels of service?

· What is the cost of the

service (operating and capital expenditure)?

· Are alternative methods for

service delivery possible?

· What is the level of public interest in the service?

The scores and

weightings of each criteria determined the priority of each review. As a

result, five services were rated high priority, 15 services rated medium

priority and seven services rated low priority.

Scheduling

of reviews will take into account the priority, as well as other factors,

including opportunities for shared reviews and/or services with other councils,

resourcing and capability considerations. The Senior Leadership Team

(‘SLT’) have proposed a timetable of reviews for 2017 to 2020. See Attachment

1 for the schedule of reviews.

3.7 How will reviews be resourced?

The

resourcing of any review will be a decision for the responsible Director in consultation

with SLT and the Chief Executive. Resourcing could be as small as a

single person (such as a service manager) or as large as a multidisciplinary

team. Where possible, internal resources will be used, however, NCC does not

have the capacity to undertake all of the required section 17A work.

There may also be further benefits to be gained from the use of appropriately

qualified external advisory resources. Use of internal staff or external

services will be dependent on the scale and complexity of the review.

Scaling

NCC

will take a scaled approach to section 17A reviews as follows:

· Level 1 – a minimal review is carried out focusing on easy

implementation and quick wins. This will most likely be small in scale

and conducted using in-house resources. An example of level 1 is a contract

review.

· Level 2 – a medium sized review is carried out. This

review may involve more complex efficiency gains and may involve some change in

delivery mechanism, governance or funding.

· Level 3 – a significant review is carried out. It is

likely to be a complex, multi-party review and may result in substantive

governance and/or funding changes.

3.8 What should reviews focus on?

Section

17A requires consideration of the following options:

· Funding, governance and delivery by NCC;

· Responsibility for funding and governance is undertaken by NCC and

delivery is undertaken by another local authority;

· Responsibility for funding and governance is undertaken by NCC and

delivery is undertaken by a CCO wholly owned by NCC;

· Responsibility for funding and governance is undertaken by NCC and

delivery is undertaken by a CCO, where NCC is a part owner (the other owner or

owners might be a local authority or other organisation);

· Responsibility for funding and governance is undertaken by NCC and

delivery is undertaken by some other person or agency (such as a private or

community sector agency);

· Responsibility for funding and governance is delegated to a joint

committee or other shared governance arrangement and delivery is undertaken by

some other person or agency; and

· Any other reasonably practicable option for funding, governance and

delivery.

Opportunities

for improving performance

17A

reviews should consider and report on options for generating efficiency gains

or improving our performance even if no change in funding, governance and

delivery is proposed. This is consistent with NCC’s focus on

business excellence. It ensures efficiency across the 17A and business

excellence work programmes. It also minimises the disruption of too

frequent reviews, which can unsettle teams.

3.9 Significance

and Consultation

While

local authorities are not required to engage with the community when

undertaking 17A reviews, obligations to engage may exist where levels of

service are being changed, or should options such as establishment of a CCO be

mooted. The Significance and Engagement Policy provides guidance on

consultation requirements.

Regardless of any obligations to engage, NCC considers that it would

be beneficial to the reviews to convene a community focus group to consult with

when developing options for service funding, delivery or governance. The use of

a focus group or any other form of consultation should be identified at the

scoping stage of a review and utilised where appropriate

Any government led legislation/governance changes may not be subject

to our normal consultation processes.

2.0 Implications

Financial

There will be direct

financial costs associated with the undertaking of section 17A review

work. NCC has conservatively budgeted $250,000 over three years, with

some ongoing provision in order to undertake the work.

It is noted that, depending

on what the analysis finds, and what decision are made by NCC, the work

proposed should lead to savings in costs to Council or ratepayers/service users

and/or gains in service quality and consistency.

Social & Policy

None

Risk

None

2.1 Options

Council is required to undertake

the work specified in section 17A LGA. To that extent, there are no

substantive options with regard to undertaking these reviews.

Council can vary the priorities

for the work, but based on discussions between the Senior Leadership Team, the

timeline for reviews set out in Attachment 1 is recommended.

2.2 Development of Preferred Option

N/A

3.6 Attachments

a Attachment

1: Timeline for 17A reviews ⇩

Finance Committee – 14 June 2017 – Open Agenda

Finance Committee – 14 June 2017 –

Open Agenda

4. HB

LASS Limited - Statement of Intent

|

Type of

Report:

|

Operational

and Procedural

|

|

Legal

Reference:

|

Local

Government Act 2002

|

|

Reporting

Officer/s & Unit:

|

Adele

Henderson, Director Corporate Services

|

41.1 Purpose of Report

To receive the Final Statement

of Intent 2017/18 for Hawke’s Bay Local Authority Shared Services Limited

(HB LASS Ltd) to Council as part of the reporting requirements

for Council-Controlled Organisations.

|

Officer’s Recommendation

That Council:

a. Receive the Final approved Statement of Intent for

2017/18 for HB LASS Limited (HB LASS Ltd).

|

|

CHAIRPERSONS RECOMMENDATION

That the Council resolve that the officer’s

recommendation be adopted.

|

4.2 Background

The Local Government Act 2002

sets out monitoring and reporting requirements of council organisations (Part

5, Section 66, Local Government Act 2002). The HB LASS

Limited is a council-controlled organisation as defined under Part 1,

Section 6, of the Local Government Act 2002.

4.3 Implications

Financial

None

Social & Policy

None

Risk

None

4.4 Attachments

a HB

LASS Limited Statement of Intent 2017/18 ⇩

Finance Committee – 14 June 2017 – Open Agenda

Finance Committee – 14 June

2017 – Open Agenda

5. HB

Museums Trust Statement of Intent 2017 - 19

|

Type of

Report:

|

Legal

|

|

Legal

Reference:

|

Local

Government Act 2002

|

|

Document

ID:

|

358905

|

|

Reporting

Officer/s & Unit:

|

Adele

Henderson, Director Corporate Services

|

5.1 Purpose of Report

To receive the final Statement of Intent 2017

– 19 for the Hawke’s Bay Museums Trust to Council

required for reporting requirements for Council-Controlled Organisations.

|

Officer’s Recommendation

That Council:

Receive the final Hawke’s Bay Museums Trust Statement of

Intent 2017 – 19.

|

|

CHAIRPERSON’S RECOMMENDATION

That the officer’s recommendation

be adopted.

|

5.2 Background

The Local Government Act 2002

sets out monitoring and reporting requirements of council organisations (Part

5, Section 66, Local Government Act 2002). The Hawke’s Bay Museums

Trust is a council-controlled organisation as defined under Part 1, Section 6,

of the Local Government Act 2002.

5.3 Implications

Financial

None

Social & Policy

None

Risk

None

5.4 Attachments

a HB

Museums Trust Statement of Intent 2017/18 ⇩

Finance Committee – 14 June 2017 – Open Agenda

Finance Committee – 14 June

2017 – Open Agenda

6. Hawke's

Bay Airport Limited - Statement of Intent

|

Type of

Report:

|

Operational

and Procedural

|

|

Legal

Reference:

|

Local Government

Act 2002

|

|

Reporting

Officer/s & Unit:

|

Adele

Henderson, Director Corporate Services

|

61.1 Purpose of Report

To receive the final Statement

of Intent 2017/18 for Hawke’s Bay Airport Limited (HBAL)

to Council required for reporting requirements for Council-Controlled

Organisations.

|

Officer’s Recommendation

That Council:

a. Receive the final Statement of Intent for 2017/18 for

Hawke’s Bay Airport Limited (HBAL).

|

|

CHAIRPERSONS RECOMMENDATION

That the Council resolve that the

officer’s recommendation be adopted.

|

6.2 Background

The Hawke’s Bay Airport

Limited is a Council Controlled Organisation (CCO). It is a company

incorporated under the Companies Act and is owned by the Crown, Hastings

District Council and Napier City Council. Napier City Council has a 26%

shareholding.

The Local Government Act 2002

requires Council Controlled Organisations (CCO) to submit a Statement of Intent

to their shareholders for consideration.

The Hawke’s Bay Airport

Ltd Statement of Intent is attached.

6.3 Implications

Financial

None

Social & Policy

None

Risk

None

6.4 Attachments

a Hawke's

Bay Airport Limited Statement of Intent ⇩

Finance Committee – 14 June 2017 – Open Agenda

Hawke’s Bay Airport Limited

Statement of Intent

For the year ended 30 June 2018 and the two following

years.

1.0 Governance

Governance

sits with the Board of Directors of Hawke’s Bay Airport Limited, which is

responsible for the strategic and overall direction of the organisation.

Directors are appointed by the company’s shareholders; the Napier City

Council (26%), Hastings District Council (24%) and the Crown (50%).

The Board has

four Directors, two of whom are appointed by the Napier City Council and the

Hastings District Council and two whom are appointed by the Crown. The Board

meets regularly with Management to review the company’s performance and

provides quarterly, half yearly and annual business performance reports to

shareholders.

2.0 Nature

and Scope of Activities

2.1 Mission

Statement

The mission

of Hawke’s Bay Airport Limited is: -

· to provide convenient, safe and

sustainable services and facilities for airlines, air travellers, employees,

our community of tenants, contractors and all other visitors to the

airport

· to support regional economic

development through the provision of strategic infrastructure

· to generate appropriate returns on

assets employed and shareholder’s equity

· to position the business for growth

and embrace collaboration and strategic alliances with others

2.2 Vision

Statement

· Our vision is to be a welcoming

gateway to Hawke’s Bay and to be recognised as a major contributor to the

economic development and wellbeing of the Hawke’s Bay community.

2.3 Values

· We are customer focused

· We are commercially driven

· We are committed to safety and

security

· We think strategically and plan for

the long term

· We work as a team

· We act with integrity

2.4 Strategy

Our

Strategic Imperative:

To maintain operational capability in an efficient, safe and sustainable

manner, position the business for the future, achieve growth across all revenue

streams and manage risk.

Our Strategic

Objectives:

1. Operate an

airport that is fit for purpose.

2. Preserve the

Airport’s ability to operate and maintain a high level of security

consciousness and awareness across the Airport community.

3. Operate HBAL as a

successful business, growing revenue, profitability and shareholder value on an

annual basis.

4. Generate

additional revenue from non-aeronautical activities.

5. Proactively

manage health and safety risks and provide a safe, healthy and thriving

environment through consultation, co-operation and co-ordination between

persons conducting a business or undertaking (PCBU) within the Airport

community.

6. Operate the Airport

in a socially and environmentally sustainable manner.

7. Maintain and

enhance business-critical infrastructure, services and facilities for all users

of the Airport.

8. Realise the

long-term value of the business park.

HBAL will pursue the following

strategy:

1. Redevelop and

construct an efficient and fit for purpose terminal building and Airport Rescue

Fire Service Building.

2. Maintain

operational capability with minimal disruption throughout the terminal

development project.

3. Rezone and

freehold the Business Park land and minimise the land development

costs.

4. Continue to

strengthen our relationships with all operators of air services and with all

tenants and prospects.

5. Improve the

security culture and consciousness at the Airport

6. Improve the

customer experience at the Airport for all travellers, meeters and

greeters.

7. Maintain active

membership and contribution to New Zealand Airports Association.

8. Maintain

effective engagement and relationships with key stakeholders and the wider

stakeholder community.

9. Form strategic

alliances and collaborate with other airports.

10.

Investigate potential for JV partnerships to develop the airport land.

3.0 Key

Objectives: Business Plan FY 2017/18

|

ACTIVITY

|

OUTCOME

|

TARGET DATE

|

|

Operate a successful business

|

Achieve Financial Targets

|

30/06/18

|

|

Appropriate Infrastructure

|

Effect CAPEX Investments

|

30/06/18

|

|

Health & Safety focus

|

Continue to work toward zero harm

|

ongoing

|

|

Progress Terminal Redevelopment

|

Project complete

|

30/06/19

|

|

Strengthen Rescue Fire Station

|

Project complete

|

30/06/18

|

|

New Airport Entranceway

|

Project complete

|

30/06/18

|

|

Business Park rezoned

|

Project complete

|

30/06/18

|

|

Key Customer Relationships

|

Meetings with key customers

|

Ongoing

|

|

Consolidate waste and recycling

management

|

Bi-annual audit of consumption

|

June, December

|

|

Review Strategic Plan

|

Current, Refreshed Strategic Plan

|

30/06/18

|

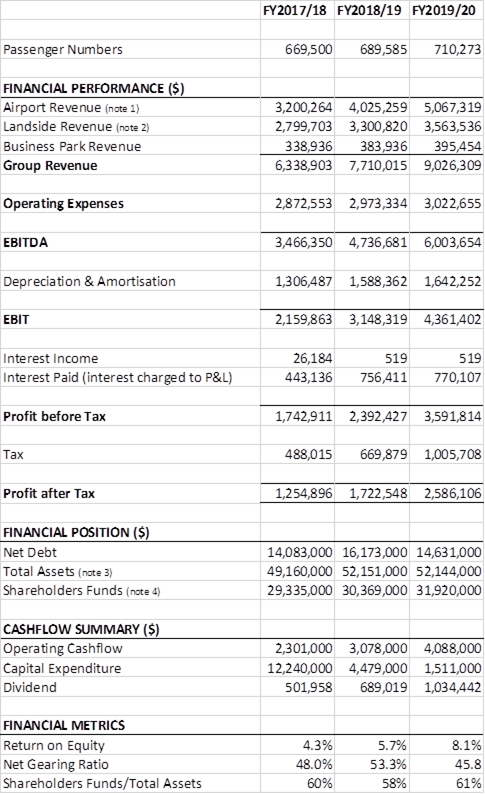

3.1 Financial

Performance Targets

The

performance targets include continued growth in passenger numbers and increases

in landing charges, rental and concession income. Significant further

capital expenditure is proposed which will increase interest and depreciation

expenses and the gearing ratio over the next 3 financial years.

Note 1: Airside Revenue includes aircraft landing

and parking charges

Note 2: Landside Revenue includes car parking,

rents, concessions, advertising and other income Note 3: Total Assets is

the total of all current and non-current assets

Note 4: Shareholders Funds is the total of share

capital and retained earnings

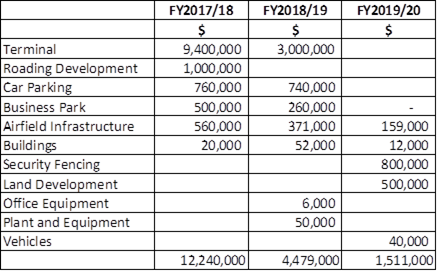

3.2 Capital

Expenditure

4.0 Accounting

Policies

The

accounting policies adopted by HBAL are consistent with New Zealand’s

International Financial Reporting Standards and generally accepted New Zealand

accounting practices. The policies are included within HBAL’s

Annual Report that is available on the Company’s website;

www.hawkesbay-airport.co.nz/about/company/annual report

5.0 Distributions

The Board has

considered an alternative dividend policy based on an agreed proportion of free

cash flow measure, rather than net profit after tax (NPAT). However, the Board

has decided to retain its current dividend policy of 40% NPAT. Had the

proportion of free cash flow measure been adopted as policy, no free cash would

have been available for distribution to Shareholders during the period of

significant capital expenditure in our infrastructure. Retention of the current

dividend policy (40% NPAT) will enable annual dividends to be paid to

shareholders throughout the capital expenditure programme.

6.0 Information

to be provided to Shareholders

Shareholders will receive:

· An annual report including audited

financial statements within 3 months of balance date.

· A 6-monthly report including

non-audited financial statements within 2 months of balance date.

· A Quarterly Report within 2 months of

the end of each quarter.

· A Statement of Intent submitted for

shareholders’ consideration in accordance with the Local Government Act

2002

· Other interim financial reports as

agreed with the shareholders

· Reports on matters of material

interest to shareholders. Shareholders will continue to be kept informed of key

developments, consistent with the Crown’s ‘No Surprises’

policy.

7.0 Acquisition

Procedures

The

acquisition of any interest in a company or organisation will only be

considered when it is consistent with the long-term commercial objectives of

the company. Any material acquisition will be the subject of consultation with

shareholders.

Major

transactions as defined by the Companies Act 1993 will require shareholder

approval.

8.0 Compensation

Sought from Local Body Shareholders

At the

request of the shareholders the company may undertake activities that are not

consistent with normal commercial objectives.

The company

may seek, in these circumstances, a specific subsidy to meet the full

commercial cost of providing such activities, however none are contemplated in

the planning period.

9.0 Estimate

of Commercial Value

The net book

value of Shareholders investment in the company as at 31 December 2016 is

$28,466,588.

The

non-current assets owned by HBAL were revalued at 30 June 2015 to their current

market value resulting in an uplift in value of $9.5 million (net of the

deferred tax impact). The individual assets and liabilities included on

the balance sheet at 30 June 2016 are therefore not considered by the Directors

or Management to be materially different from the current market value.

HBAL will

continue to undertake a revaluation approach to its assets on a regular cycle

of every 3 years or when there has been a significant change in the market, to

consider the gap between current book values of the assets and liabilities versus

the commercial value of the business.

Tony M Porter

Chairman

Hawke’s Bay Airport Limited

2 June, 2017

PUBLIC EXCLUDED ITEMS

That the public be excluded from the following

parts of the proceedings of this meeting, namely:

AGENDA ITEMS

1. Hawke's

Bay Airport Limited - Report to Shareholders

2. Bad

Debt Write Off

The general subject of each matter to be

considered while the public was excluded, the reasons for passing this

resolution in relation to each matter, and the specific grounds under Section

48(1) of the Local Government Official Information and Meetings Act 1987 for

the passing of this resolution were as follows:

|

GENERAL SUBJECT OF

EACH MATTER TO BE CONSIDERED

|

REASON FOR PASSING THIS RESOLUTION IN RELATION TO EACH MATTER

|

GROUND(S) UNDER SECTION 48(1) TO THE PASSING OF THIS RESOLUTION

|

|

1. Hawke's Bay Airport Limited -

Report to Shareholders

|

7(2)(h) Enable the local authority to carry out,

without prejudice or disadvantage, commercial activities

|

48(1)A That the public conduct of the whole or the

relevant part of the proceedings of the meeting would be likely to result in

the disclosure of information for which good reason for withholding would

exist:

(i) Where the local authority is named or specified in Schedule 1 of this

Act, under Section 6 or 7 (except 7(2)(f)(i)) of the Local Government

Official Information and Meetings Act 1987.

|

|

2. Bad Debt Write Off

|

7(2)(a) Protect the privacy of natural persons, including

that of a deceased person

7(2)(h) Enable the local authority to carry out,

without prejudice or disadvantage, commercial activities

|

48(1)A That the public conduct of the whole or the

relevant part of the proceedings of the meeting would be likely to result in

the disclosure of information for which good reason for withholding would

exist:

(i) Where the local authority is named or specified in Schedule 1 of this

Act, under Section 6 or 7 (except 7(2)(f)(i)) of the Local Government

Official Information and Meetings Act 1987.

|

NAPIER

CITY COUNCIL

NAPIER

CITY COUNCIL

Civic Building

231 Hastings Street,

Napier

Phone: (06) 835

7579

www.napier.govt.nz

Finance

Committee

Open

MINUTES

|

Meeting Date:

|

Wednesday 3 May 2017

|

|

Time:

|

3pm-3.20pm

|

|

Venue:

|

Main Committee Room

3rd floor Civic Building

231 Hastings Street

Napier

|

|

Present:

|

Councillor Wise (In the Chair), Mayor

Dalton, Councillor Boag, Dallimore, Hague, Jeffery, McGrath, Price,

Tapine, Taylor, White, and Wright

|

|

In Attendance:

|

Chief Executive, Director Corporate

Services, Director Infrastructure Services, Director Community Services,

Director City Strategy, Manager Communications

|

|

Administration:

|

Governance Team

|

Finance Committee – 14 June 2017 – Open Agenda

Apologies

CONFLICTS

OF INTEREST

Nil

Public

forum

Nil

Announcements

by the Mayor

Nil

Announcements

by the Chairperson

Nil

Announcements

by the Management

Nil

Confirmation

of Minutes

|

Councillors Taylor / Wright

That the Minutes of the meeting held

on 22 March 2017 were taken as a true and accurate record of the meeting.

CARRIED

|

|

Councillors Price / McGrath

That the Minutes of the meeting held

on 29 March 2017 were taken as a true and accurate record of the meeting.

CARRIED

|

1. HB LASS Limited - Draft Statement of

Intent

|

Type of Report:

|

Operational and Procedural

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Reporting Officer/s & Unit:

|

Adele Henderson, Director Corporate Services

|

11.1 Purpose

of Report

To

provide the draft Statement of Intent 2017/18 for Hawke’s Bay Local

Authority Shared Services Limited (HB LASS Ltd) to Council for its consideration as

part of the reporting requirements for council-controlled

organisations.

|

At the Meeting

In response to queries from Councillors, it was clarified

that:

·

The HB LASS

consists of Chief Executives and an external Chair.

·

The HB LASS can

bring in outside expertise as it considers appropriate.

·

Outside expertise

may be called on during the discussions on Section 17A review requirements,

in particular on asset management and infrastructure matters.

·

Section 17A

reviews are a requirement under the Local Government Act and require local

authorities to assess their current service provisions, and opportunities for

finding efficiencies.

·

There are a number

of informal and other shared services which are not specifically touched on

within the statement of intent document, but are which are captured in

council’s annual report.

·

Hastings District

Council, Hawke’s Bay Regional Council and Wairoa District Council have

all approved the HB LASS statement of intent without amendments.

|

|

Committee's

Recommendation

Councillor Hague /

Councillor Jeffery

That Council:

a. Receive the

Draft Statement of Intent for 2017/18 for HB LASS Limited (HB LASS Ltd) and

provide any feedback to the HB LASS board by 31 May 2017.

CARRIED

|

2. Quarterly Report to 31 March 2017

|

Type of Report:

|

Operational

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

347953

|

|

Reporting Officer/s & Unit:

|

Mary Quinn, Senior Management Accountant

Caroline Thomson, Chief Financial Officer

|

2.1 Purpose

of Report

To

consider the Quarterly Report on performance by Activity Group for the period 1

January 2017 to 31 March 2017 and the Health and Safety Report to March 2017.

|

At the Meeting

The Director Corporate Services gave a brief overview of

the key highlights of the third quarter including that:

·

The Seawall

project has been completed and well received.

·

The Napier Conference

Centre was completed and successfully relaunched as an events venue.

·

Online building

consents are now available.

·

Council’s

free Wi-Fi offering was extended into new areas.

·

Earthquake

strengthening of the Ivan Wilson pool has been completed.

·

Marine Parade

development continued.

·

Tourism areas

performed better than expected so income from the quarter was higher than

forecast.

In response to a questions from Councillors, it was

clarified that:

·

The Infrastructure

Services group are working closely with contractors on the Marine Parade

development to re-establish a new timeframe for completion of the works.

·

Improvements have

already been made to the structure of our contract template, and procurement

process to ensure that council have the ability to enact greater penalties

for breach of contract.

·

The Infrastructure

Services group are working with the contractor of the Embankment Bridge

project to clarify the scope and specifications of the work.

·

Local Marae are

included in Civil Defence and emergency management planning including

community resilience considerations.

·

While the audit of

council’s building warrants of fitness has been behind schedule in the

third quarter, it is still anticipated that this work will be completed by

the end of the financial year.

|

|

·

Action required:

Director Corporate Services to provide Councillors financial savings as a

result of the decision

not to consult on council’s annual plan.

|

|

Committee's

Recommendation

Councillor Taylor /

Councillor Hague

That Council:

a. Receive

the Quarterly Report for the period 1 January 2017 to 31 March 2017.

b. Receive

the Health and Safety Report to March 2017.

CARRIED

|

3. Joint Waste Futures Project Committee -

Terms of Reference

|

Type of Report:

|

Procedural

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

349973

|

|

Reporting Officer/s & Unit:

|

Deborah Smith, Governance Advisor

|

3.1 Purpose

of Report

The

purpose of this report is to obtain approval from Council for the amended Terms

of Reference (ToR) for the Joint Waste Futures Project Steering Committee.

|

At the Meeting

In response to a question on what the key changes are

between the revised TOR and the previous version, it was noted that the

proposed changes are outlined in the report.

|

|

Committee's

Recommendation

Councillors Dallimore

/ Tapine

That Council

a. Approve

the updated Terms of Reference for the Joint Waste Futures Project Steering

Committee.

b. Appoint

Cr Brosnan as the third Napier City Council representative to the Committee.

CARRIED

|

4. Hawke's Bay Crematorium Committee -

Minutes of Meeting 10 April 2017

|

Type of Report:

|

Information

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

350013

|

|

Reporting Officer/s & Unit:

|

Deborah Smith, Governance Advisor

|

4.1 Purpose

of Report

To

provide the minutes from the Hawke’s Bay Crematorium Committee to

Council.

5. Coastal Hazards Joint Committee - draft

minutes 28 February 2017

|

Type of Report:

|

Procedural

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

350014

|

|

Reporting Officer/s & Unit:

|

Deborah Smith, Governance Advisor

|

5.1 Purpose

of Report

To

provide Council with the draft minutes from the meeting of the Coastal Hazards

Joint committee on 28 February 2017.

PUBLIC

EXCLUDED ITEMS

|

Councillor Wright / Councillor Hague

That

the public be excluded from the following parts of the proceedings of this

meeting, namely:

1. Risk

Update

CARRIED

|

The

general subject of each matter to be considered while the public was excluded,

the reasons for passing this resolution in relation to each matter, and the specific

grounds under Section 48(1) of the Local Government Official Information and

Meetings Act 1987 for the passing of this resolution were as follows:

|

GENERAL SUBJECT OF

EACH MATTER TO BE

CONSIDERED

|

REASON FOR PASSING THIS

RESOLUTION IN RELATION TO EACH MATTER

|

GROUND(S) UNDER SECTION

48(1) TO THE PASSING OF THIS RESOLUTION

|

|

1. Risk

Update

|

7(2)(f)(ii) Maintain

the effective conduct of public affairs through the protection of such

members, officers, employees and persons from improper pressure or harassment

|

48(1)A That the

public conduct of the whole or the relevant part of the proceedings of the

meeting would be likely to result in the disclosure of information for which

good reason for withholding would exist:

(i) Where the local authority is named or specified in Schedule 1 of this

Act, under Section 6 or 7 (except 7(2)(f)(i)) of the Local Government

Official Information and Meetings Act 1987.

|

The

meeting concluded at 3.20pm.

|

APPROVED

AND ADOPTED AS A TRUE AND ACCURATE RECORD OF THE MEETING

CHAIRPERSON:_____________________________

DATE

OF APPROVAL:____________________

|