Finance

Committee - 20 March 2018

- Open Agenda Item

1

Agenda Items

1. Hawkes

Bay Local Authority Shared Services - Structure change

|

Type of Report:

|

Legal

|

|

Legal Reference:

|

Local Government Official Information and

Meetings Act 1987

|

|

Document ID:

|

447078

|

|

Reporting Officer/s & Unit:

|

Adele Henderson, Director Corporate Services

|

1.1 Purpose of Report

To propose the legal structure of

Hawke’s Bay Local Authority Shared Services Limited (HBLASS) become

dormant in order to focus attention and resources on the purpose of HBLASS and

reduce compliance costs for all the councils.

|

Officer’s

Recommendation

That the Council:

a. Agree

HBLASS, as a legal entity will be dormant in the short term; with the ability

for the legal entity able to be reactivated in the future.

b. Note

that the dormant status of HBLASS is effective on receipt of agreement by all

members of the Board.

c. Note

that the decision on the dormant status of HBLASS will be determined by the

majority of councils.

d. Note

that each Council will continue its participation in a Collaborative approach

that has proven effective in a pilot: Hawke’s Bay Councils delivering

Service and Value.

e. That

the Councils approve the exemption of HBLASS from the Council Controlled

Organisation requirements (Local Government Act Section 7(3))

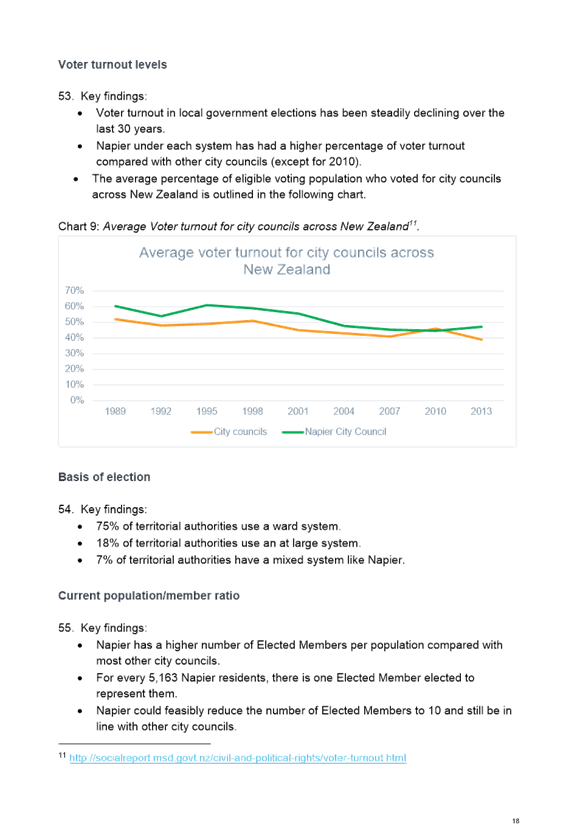

f. Note

that each Council will actively support shared and common goal setting,

decision-making, resourcing including financial contribution, staff and

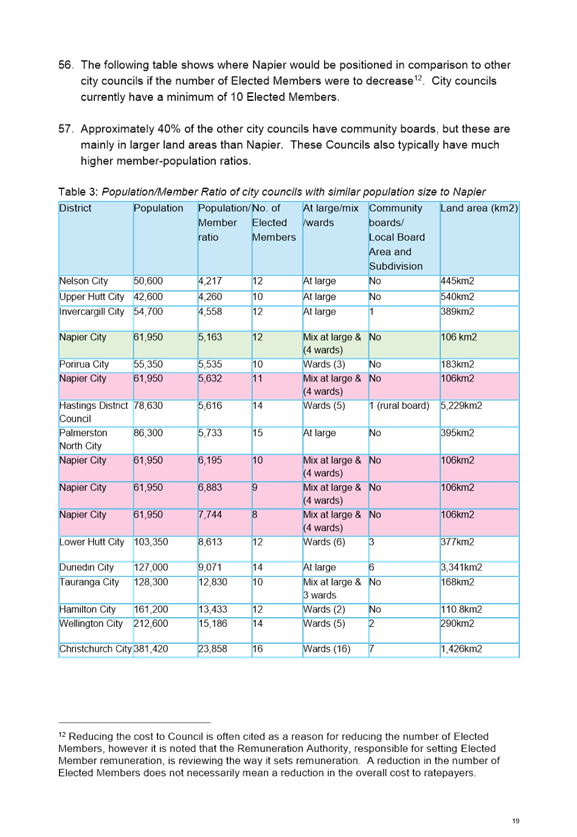

communication.

|

|

Chairperson’s

Recommendation

That the Chairperson resolve that

the officer’s recommendation be adopted.

|

1.2 Background Summary

Since 2012, when HBLASS was

incorporated as a legal entity (see the Constitution at Attachment A),

there has been significant effort to identify functions and analyse

opportunities for shared services and joint procurement across the

Hawke’s Bay Councils.

The effort and the results,

through HBLASS have been focused largely on procurement and the development of

shared IT services. HBLASS funded a Chairperson for IT shared services,

minutes, and governance as well as selective consulting studies and plans.

Because structural change and cost reduction are implicit in Shared Services,

an “all in” model was met with resistance when timing and

opportunities didn’t align with councils direction at a particular point

in time.

In early 2017, there was a review

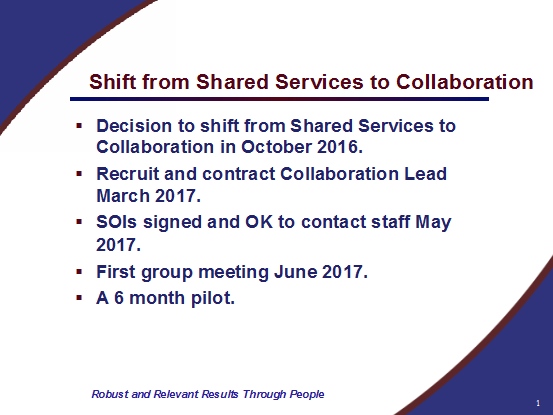

leading to a recommitment to HBLASS efforts with Collaboration as an approach

to improving Hawke’s Bay wide Service and Value. As part of the review, a

new wider role of HBLASS Collaborator was introduced on a 6 month

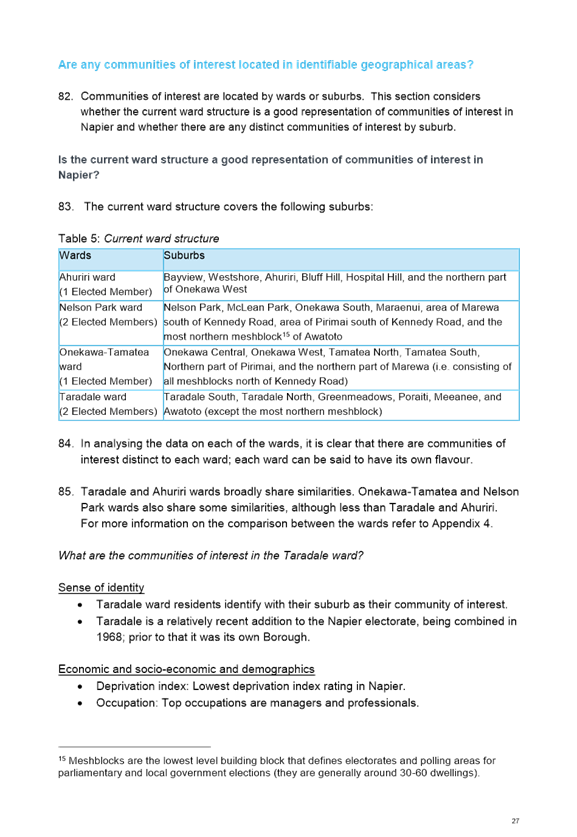

contract.

The principles of

Collaboration are:

§ Discover who is doing what

§ Connect with others that share the

same objective

§ Collaborate to delivery more for

less.

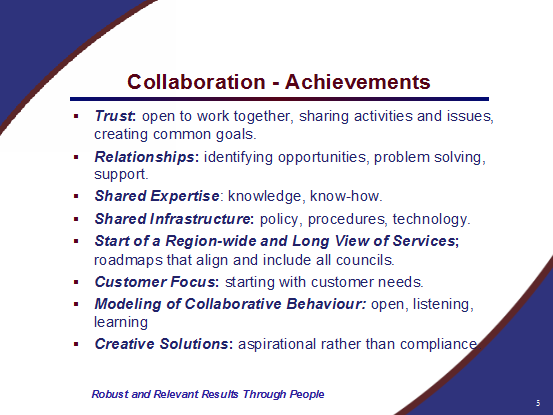

The following summarises the

Collaboration and outcomes in 2017:

The focus on collaboration versus

Shared Services is consistent with the direction that a number of the Councils

are taking in other regions. Bay of Plenty for example has a

collaboration portal that has resulted in improved knowledge sharing and

efficiencies been delivered within projects and service delivery. This portal

is now widely used by local Councils.

Staff involved have delivered

improved Service and Value across Hawke’s Bay in the following areas:

§ IT: Shared Infrastructure Services

including Wide Area Network, Desktop and Web Services.

§ GIS: Shared Aerial Photography.

§ Open Spaces: Opportunities for One

View of Information and Shared approaches to operations.

§ Animal Control: Opportunities for

Shared Education and License Data.

§ Training and Development: Common

Requirements and Shared Onsite Training.

§ Shared Internal Audit Services.

Improved quality, value and efficiency.

§ Records Management: Common

approaches.

1.3 Proposed Structure

The Chief Executive (CE) Forum,

will replace the HBLASS board structure with the same five Council CEOs and

independent chair – the function of HBLASS will continue but without the

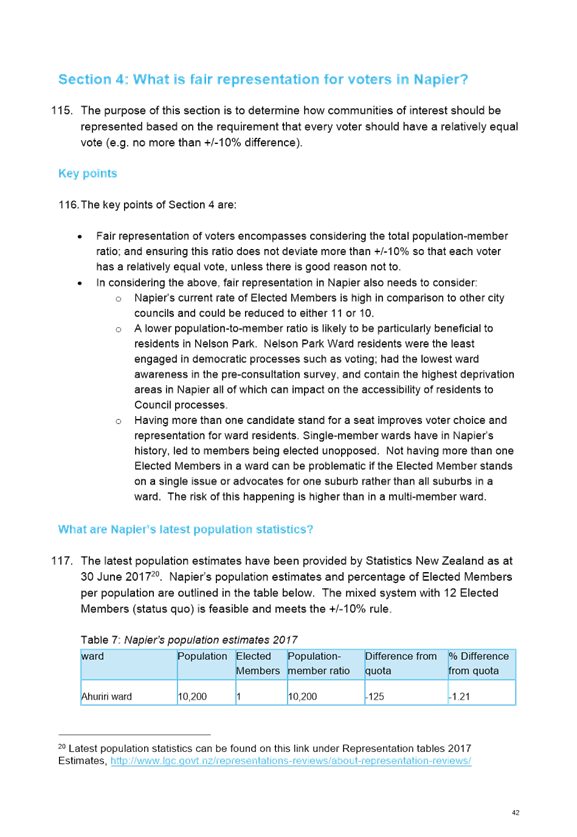

legislative requirements of operating a Company. The CE Forum group is fully

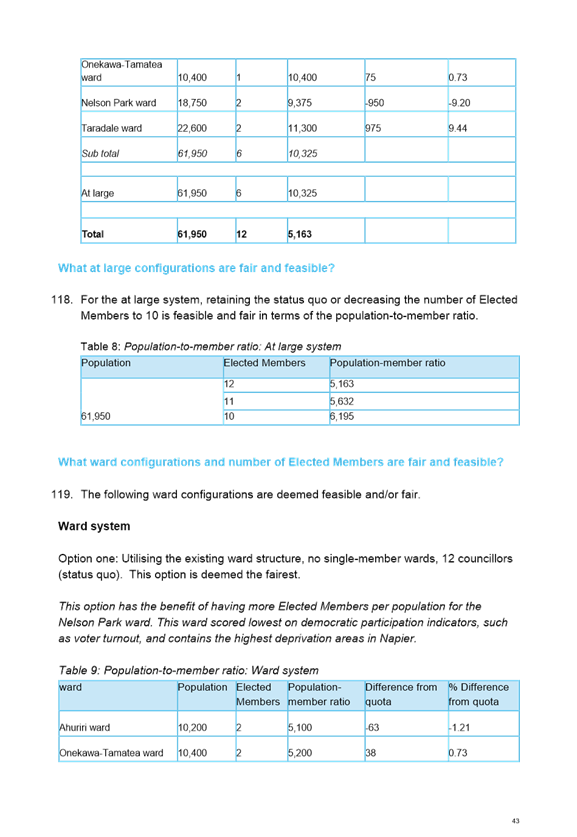

committed to working together focusing on improving Service and Value for the

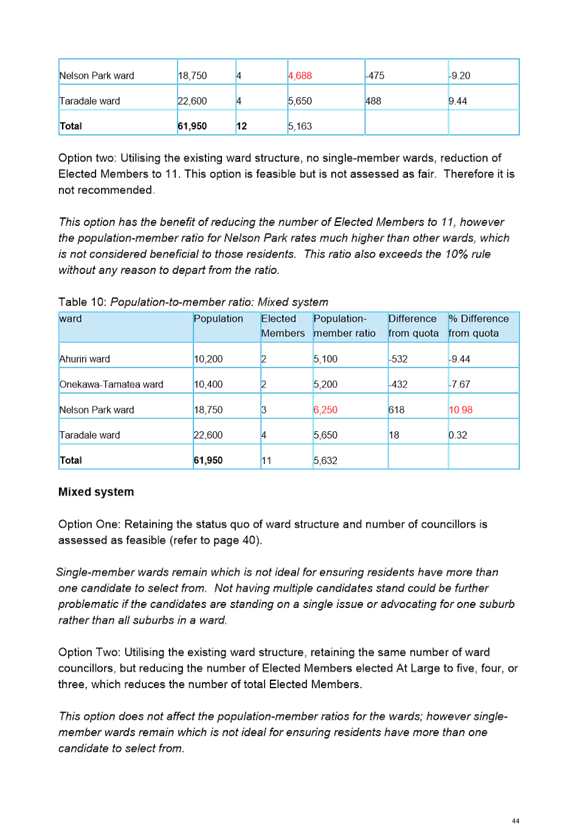

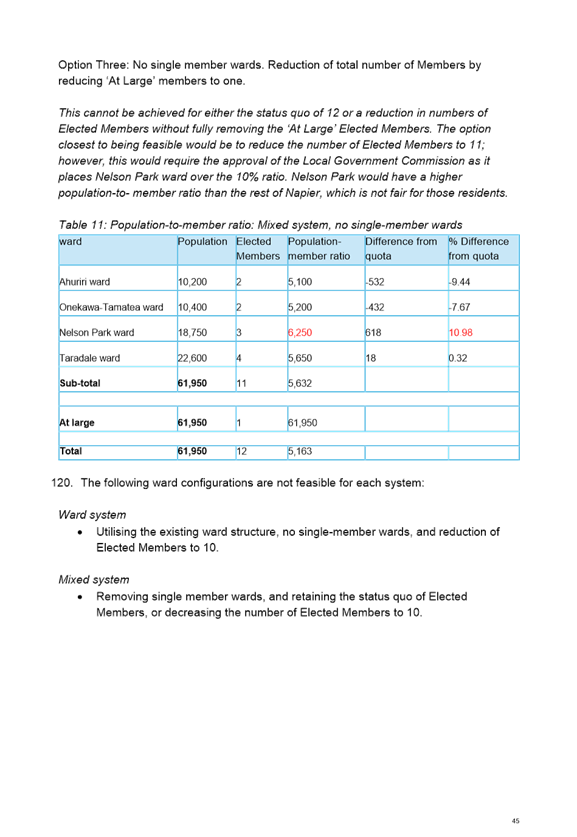

Hawke’s Bay region through collaboration. The primary difference in the

structure change is less time and resource spent on the requirements for an

active Council-owned, legal entity and more focus on setting direction and

enabling staff to achieve Service and Value. At the same time, the CE Forum

provides an umbrella and common way of operating for the many collaborative

initiatives across Hawke’s Bay, beyond HBLASS.

The administrative function is

also significantly reduced. A lead council would be identified to maintain a

ledger with invoicing to each council to recover agreed and shared costs for

the Collaboration Program and any project expenses.

To deactivate a councils-owned

company requires the following steps to be undertaken:

1. Obtain

a special resolution of shareholders (in writing and signed) stating the

shareholders agree to shelve the company.

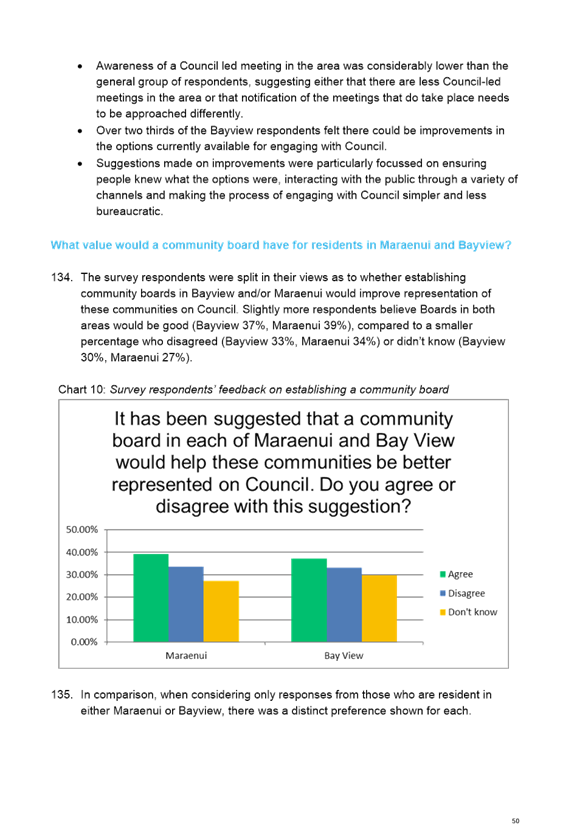

2. Pay

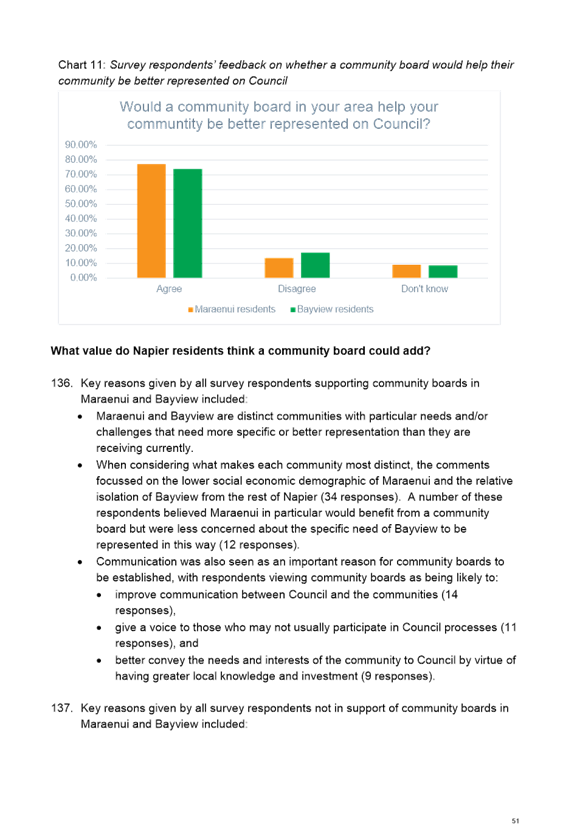

final GST return to Inland Revenue (HBLASS is not registered for FBT but this

would apply if it were).

3. Make

final payouts as determined by above resolution (if applicable) to clear the

bank accounts.

4. Close

bank accounts with Westpac.

5. Deregister

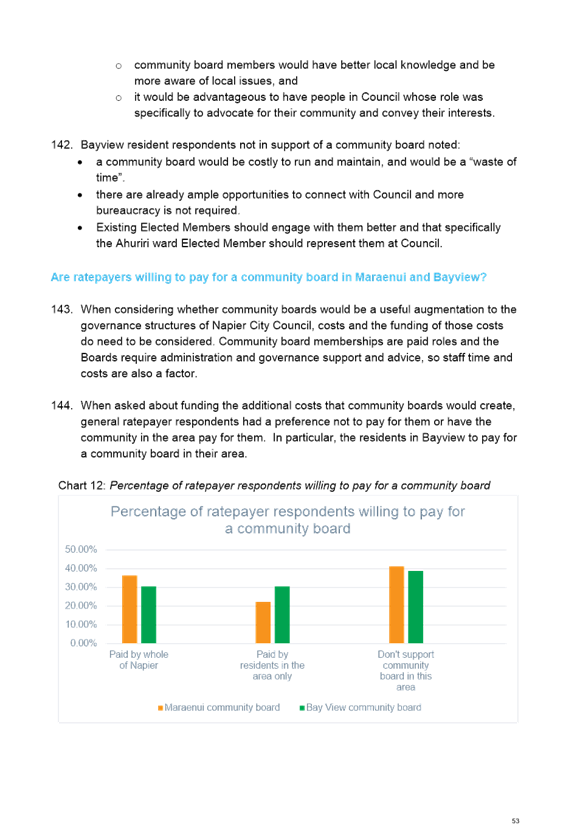

for GST with Inland Revenue.

6. File

the final income tax return (IR4) for the tax year (includes company accounts

up to the point when business ceased, but note this cannot be filed early and

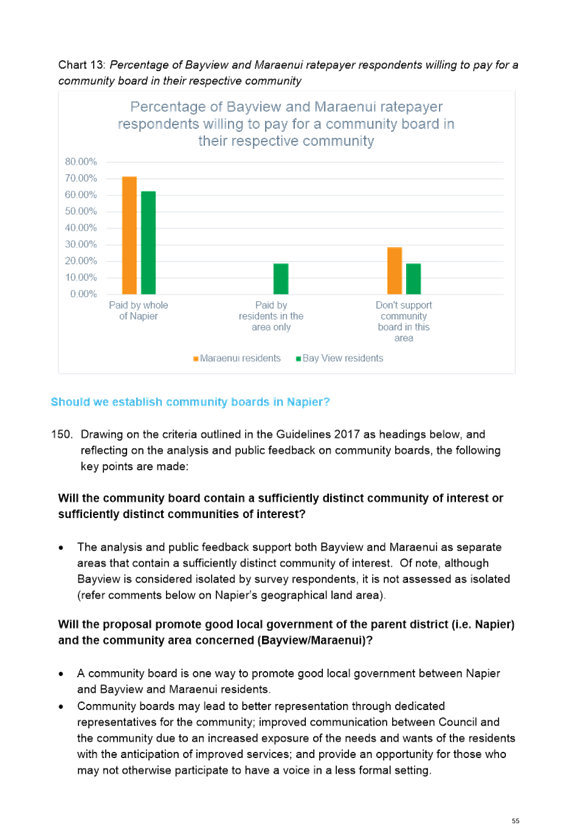

is due after the end of the financial year in which HBLASS closed).

7. File

the IR433 Non-Active Company Declaration form with Inland Revenue.

The HBLASS Limited legal entity can

be reactivated in the future if business models, organisational, contract or

procurement changes require a separate legal entity

1.4 Issues

There are no foreseen issues or

risks at this time. This structural change will cost less and focus attention

on the purpose of the LASS.

1.5 Significance and

Consultation

The Board is comprised of the

five Chief Executives of the Hawke’s Bay Councils. All Chief

Executives agree with the recommendation to make the HBLASS company dormant and

have approved a motion at their meeting on December 8, 2017.

Each Council is now being

consulted with a recommendation to make the HBLASS company dormant. The

Chief Executives intend to still refer to their activities and undertaking as a

group as HBLASS, but not as a separate legal entity. The Councils are

requested to provide a response to this proposal by the end of March 2018.

1.6 Implications

Financial

There will be residual funding from the current

years subscription, and it is proposed to transfer this to Napier City Council,

where it will provide an accountability report. The residual fund will be

to pay for the continued services of the Chairman and Collaborator roles.

Social & Policy

Through the Collaboration pilot

in 2017, there has been a significant interest shown by staff in the

opportunities for improved Service and Value across Hawke’s Bay that will

contribute to the outcome of health and prosperity of the region.

Risk

The requirements of being a CCO will still

need to be met if the Councils wish to continue with the Company in its current

format, including the preparation of a Statement of Intent. This work has

currently been put on hold.

Councils may decide not to

continue to fund the Chairperson and Collaborator role and further

opportunities on effective and efficient services may be missed.

1.7 Options

The options available to Council

are as follows:

a. Approve

the recommendation to make dormant HB Local Authority Shared Services Limited.

b. Not

approve the recommendation with HBLASS Limited to continue in its current form.

c. Recommend

that all shared service/collaboration activities cease immediately.

1.8 Development of

Preferred Option

Option A – Make the HBLASS

legal entity dormant as this will result in a lower financial and

administration burden to the councils while improving the focus to meet Service

and Value outcomes.

As

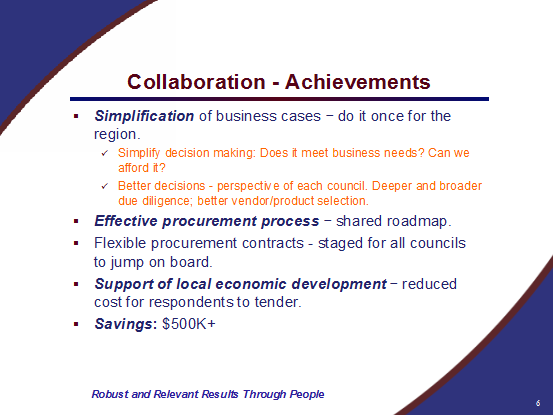

noted above during the review of HBLASS in 2017, LASS organizations around New

Zealand were approached to share their experience. Success was linked directly

with a collaborative approach. Other LASS organizations that have taken the traditional

structural/cost reduction approach with services being operated and contracts

run through the LASS, are currently assessing the change to a collaborative

approach for more robust and relevant solutions.

HBLASS has taken the initiative to test collaboration

in the Hawke’s Bay environment during 2017. There has been considerable

success over the six months of this pilot to test collaboration. In order for

further improvement, there must be greater engagement, client focus, leadership

accountability and strengthening of a collaborative culture.

1.3 Attachments

a HBLass

Constitution 2012 ⇩

Finance Committee - 20 March 2018 - Open Agenda Item

2

2. Representation

Review

|

Type of Report:

|

Legal

|

|

Legal Reference:

|

Local Electoral Act 2001

|

|

Document ID:

|

441536

|

|

Reporting Officer/s & Unit:

|

Jane McLoughlin, Team Leader Governance

Rachael Horton, Manager Business Excellence &

Transformation

|

2.1 Purpose

of Report

To determine Council’s initial

proposal for representation arrangements for the 2019 and 2022 elections.

|

Officer’s

Recommendation

That Council:

Approve the initial proposal for

representation arrangements for the 2019 and 2022 elections, and that the proposal

be distributed for public consultation, that initial proposal being:

a. the

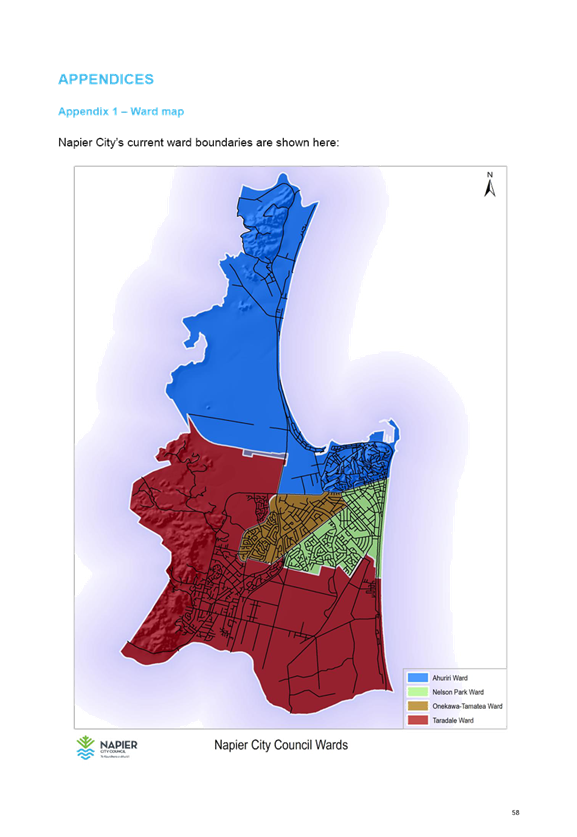

basis of election is Ward-only based on the current Ward structure:

i. that

two Elected Members be elected by the electors of the Ahuriri Ward

ii. that

two Elected Members be elected by the electors of the Onekawa-Tamatea Ward

iii. that

four Elected Members be elected by the electors of the Nelson Park Ward

iv. that four

Elected Members be elected by the electors of the Taradale Ward

b. the

total number of Elected Members is 12 and the Mayor

c. that

there be no community boards within Napier City.

|

|

Chairperson’s

Recommendation

That the Council discuss the paper

and vote on the preferred option of Council.

|

2.2 Background

Summary

What are representation

arrangements?

Representation arrangements are

the way the public are represented for local government elections for a Local

Authority such as Napier City Council, including the following options:

· The basis of election; that is, whether the election of members

(also known as councillors, other than the Mayor) is by:

o the

entire electoral district (called ‘at large’),

o the

division of the district into wards for electoral purposes, or

o a

mix of ‘at large’ and ward representation.

· If wards are used, the boundaries of wards, the names of the wards,

and the number of members that will represent each ward.

· The total number of members that are elected to the governing body

of the Council (the legal requirement is no less than 6 and no more than 30

members, including the Mayor), and

· Whether to have community boards, and if so, how many, and what

their boundaries and membership will look like.

What are the benefits of

undertaking a representation review?

Quality democratic processes are

important and foster a richer form of citizenship and civic engagement.

Electoral arrangements need to be representative and fair so that communities

feel that they have influence and can effect change.

Both the Local Government Act

2002 (Act 2002) and the Local Electoral Act 2001 (Act 2001) highlight that

diversity of communities’ matters in local government decision-making

(see sections 3, 10(1), 14(1), of the Act 2002 and section 4, (1), of the Act

2001).

As outlined above, there are

different options for representation arrangements, and the Act 2001, section

3(c) enshrines a review of these options to allow diversity in local

decision-making.

Principles outlined in the Act

2001 that govern the requirement to undertake a representation review include:

· Fair

and effective representation for individuals and communities,

· Reasonable

and equal opportunity:

o to vote

o nominate, or be nominated as

candidates, and

· Public

confidence in, and public understanding of local electoral processes.

A key outcome of undertaking a

representation review is that communities of interest within a district are

well represented on the governing body of Council and that voters have an equal

vote.

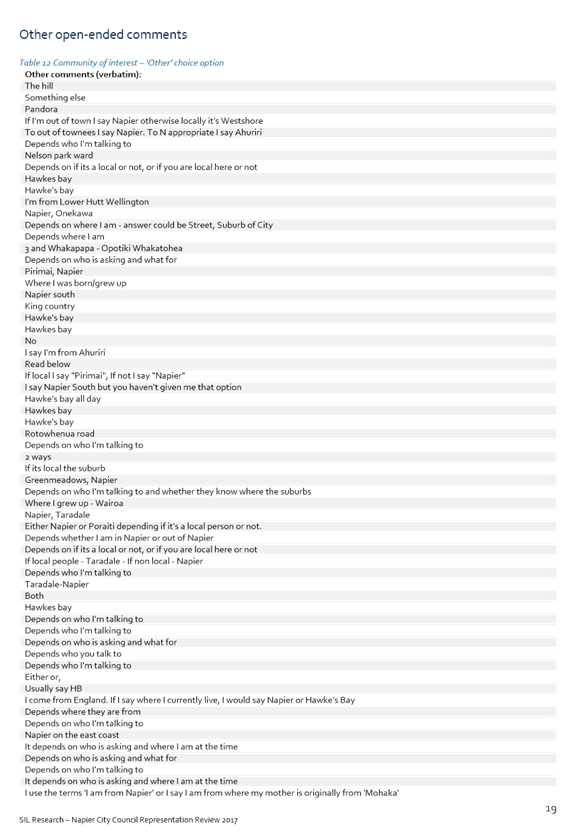

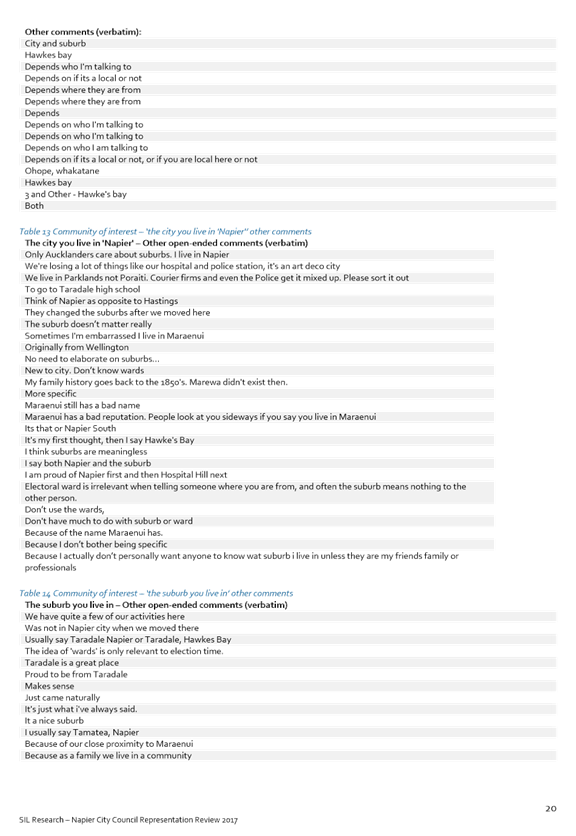

What is the process officers

have undertaken to inform this representation review?

At least every six years, a Local

Authority must review its arrangements. Napier City Council last reviewed its

arrangements in 2012 and therefore was required to review in 2018 and decide on

any changes.

For this review, Officers have

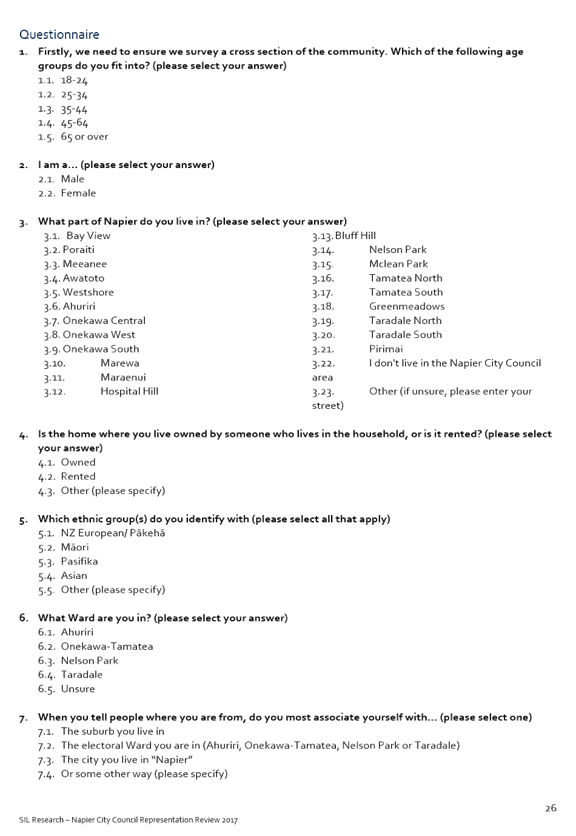

undertaken data-gathering and pre-consultation with Napier residents, and

analysis of fair and effective representation, resulting in the Representation

Review Analysis Paper (Attachment A). For more information on the

process refer to the methodology section of the Analysis

paper.

The process undertaken reflects

the Local Government Commission’s best practice guidelines that state

that Councils should undertake pre-consultation with the public and undertake

analysis on fair and effective representation. This is because the

decision on representation arrangements must not be limited to reflecting

community views, but must seek to achieve fair and effective representation for

all individuals and communities.

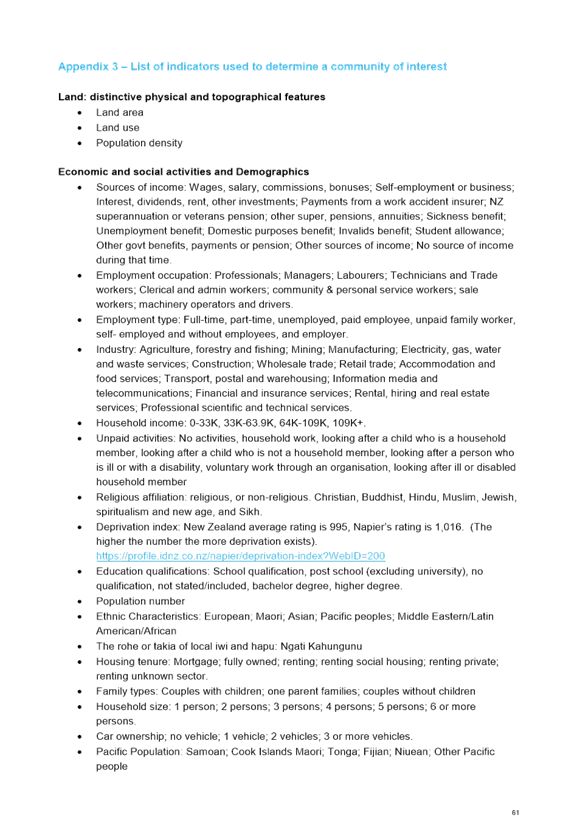

A key part of the analysis is to

identify communities of interest within Napier, and then identify how these

communities could be most effectively and fairly represented.

Officers have updated Elected

Members in Committee meetings in August and December 2017 on the process being

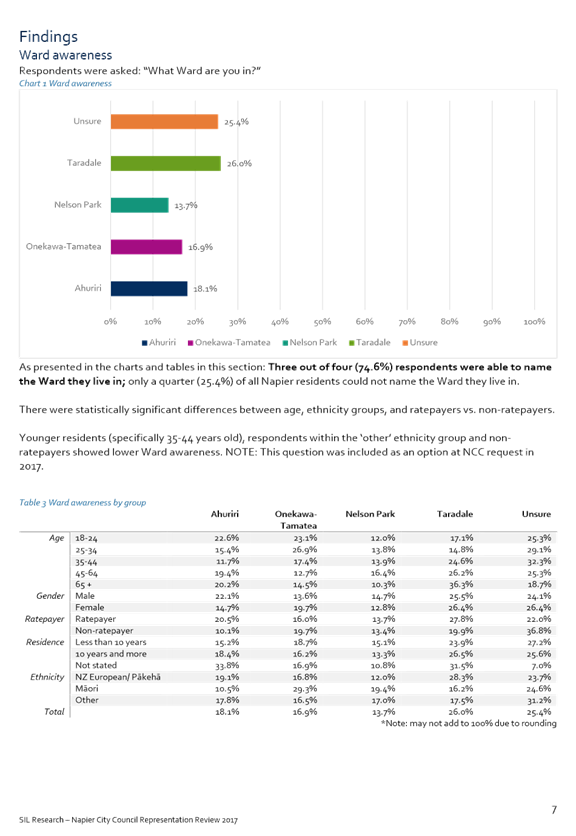

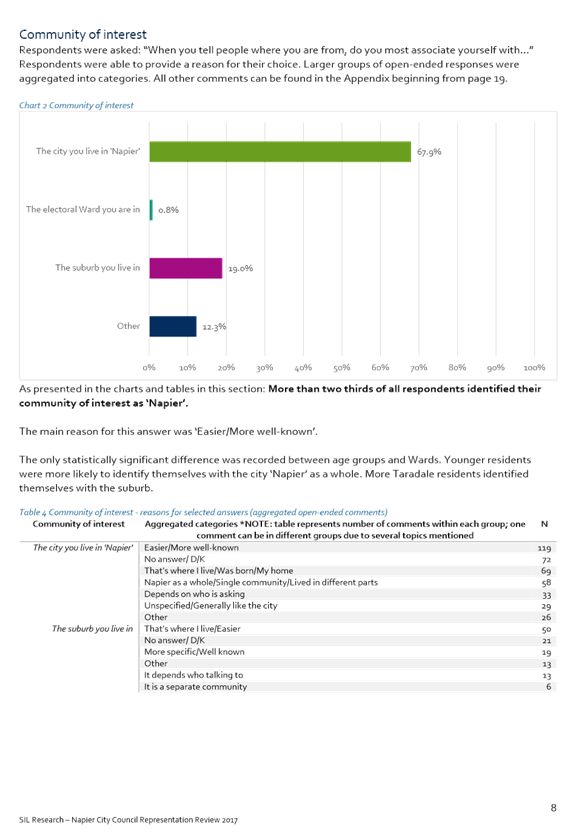

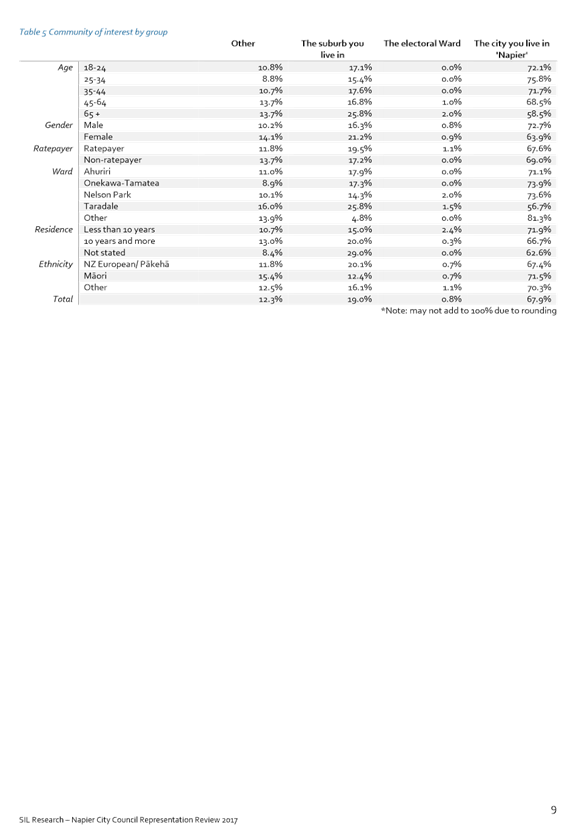

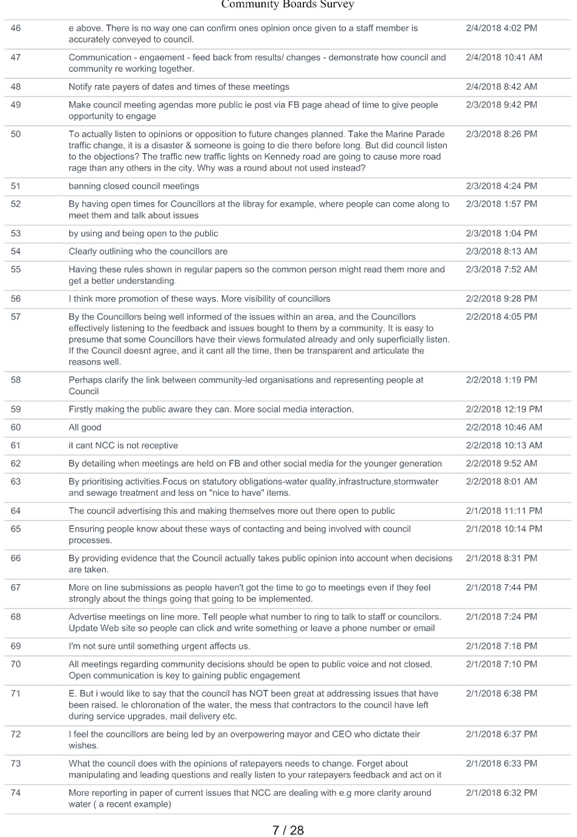

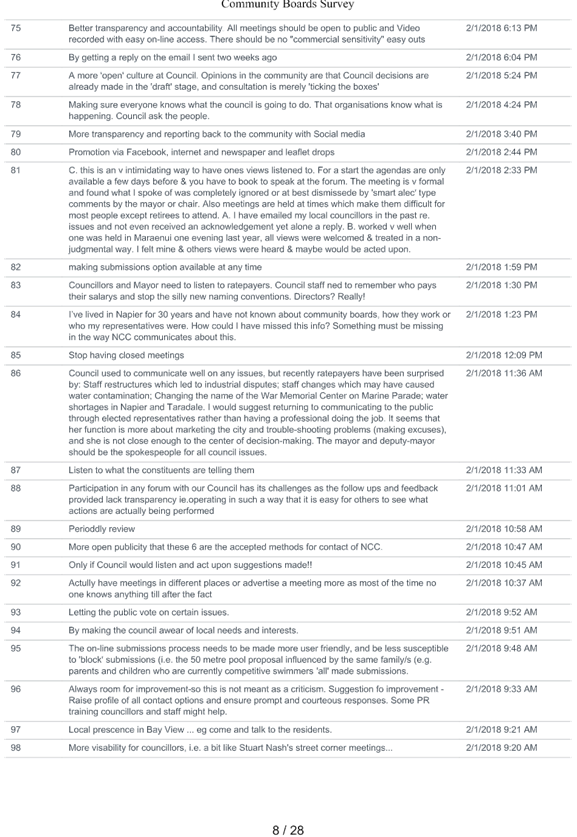

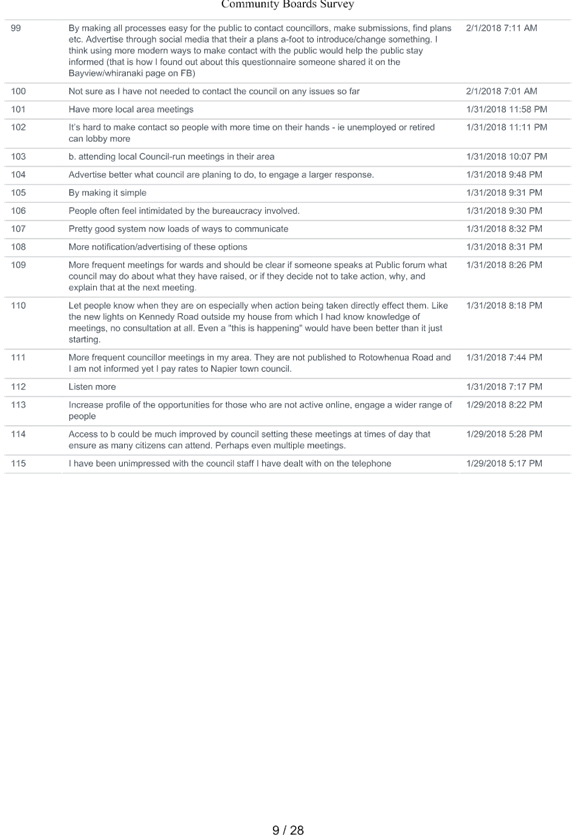

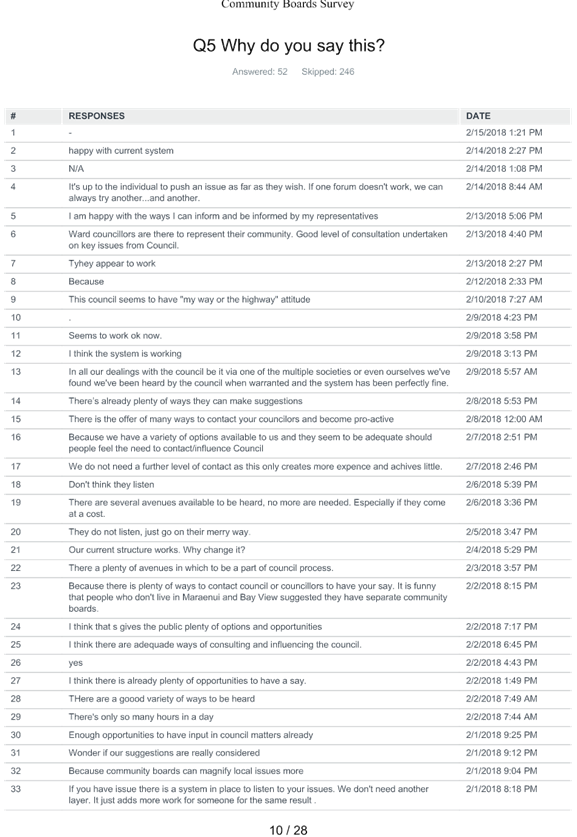

undertaken and the results of pre-consultation (Attachment B provides the

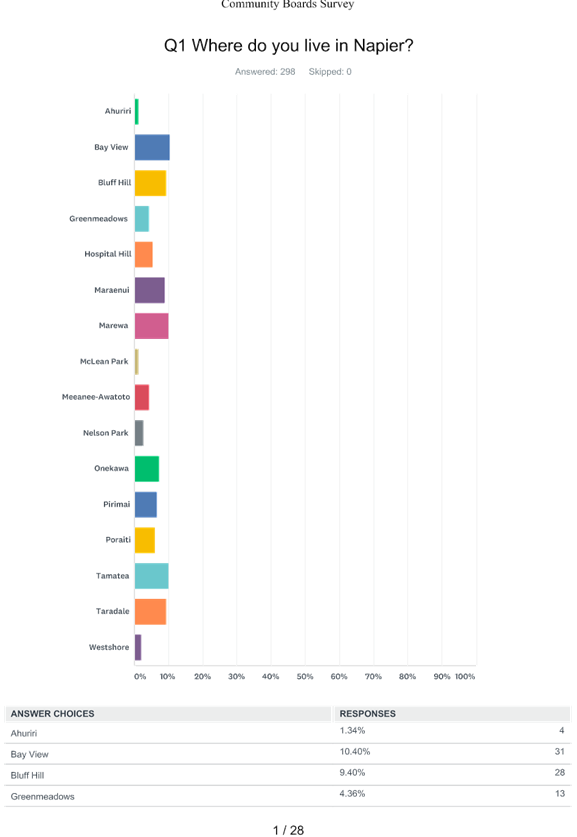

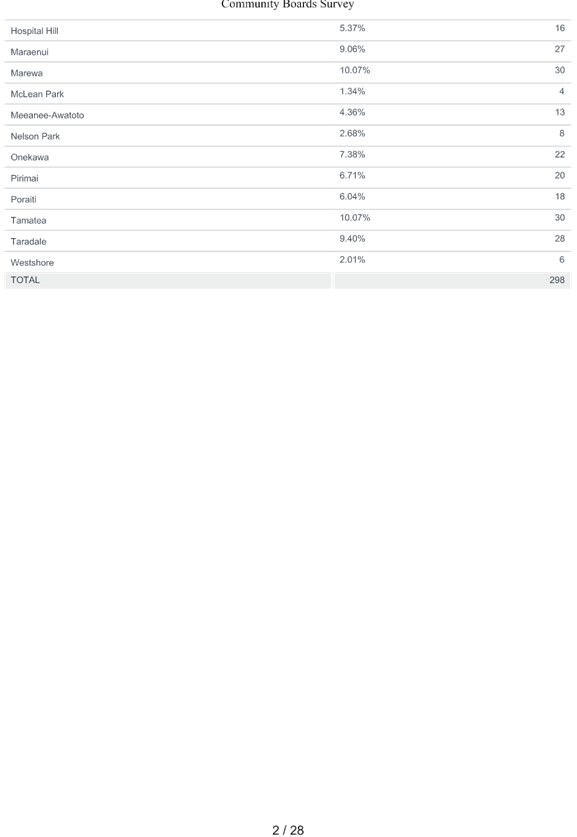

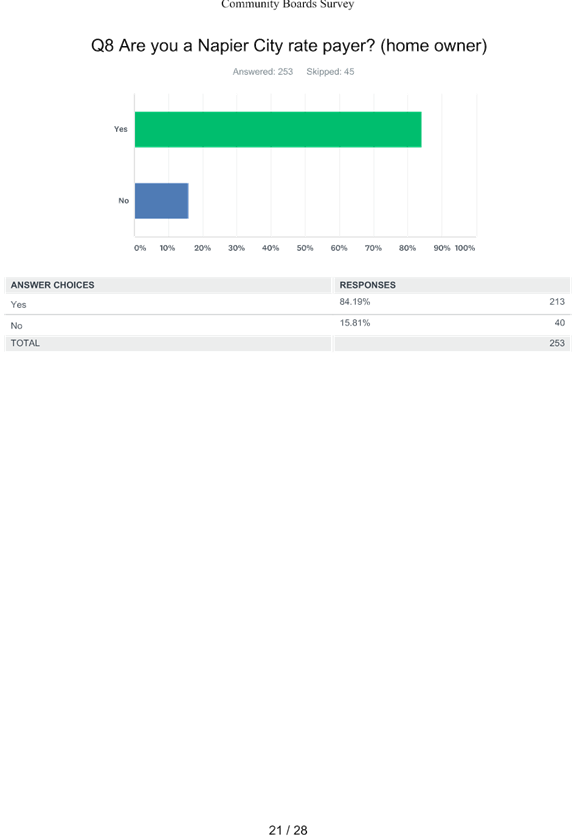

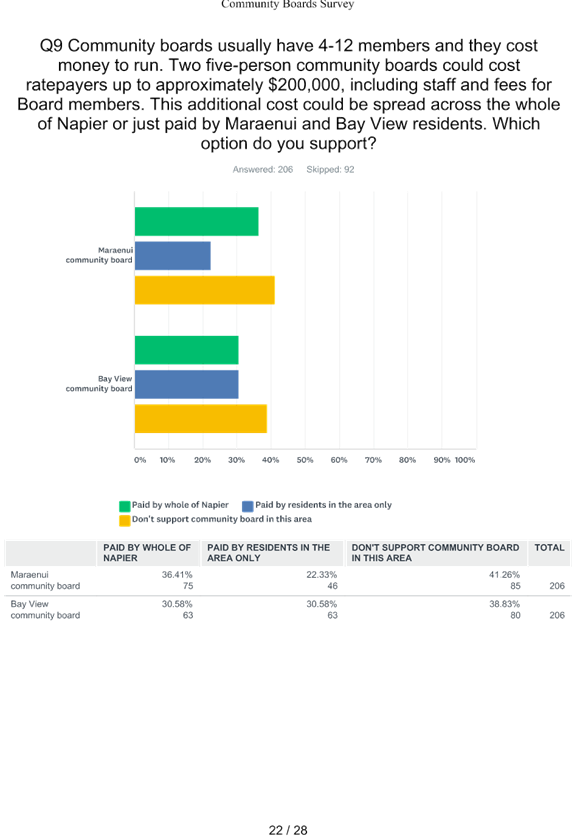

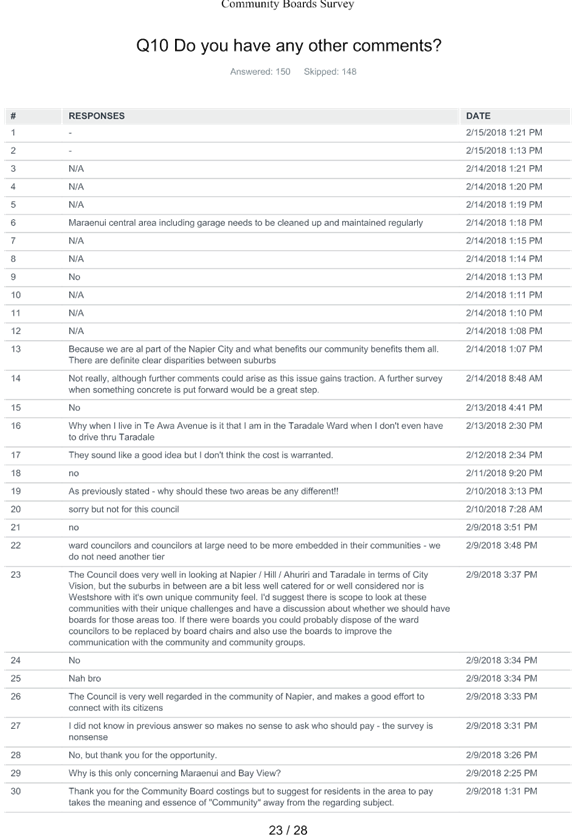

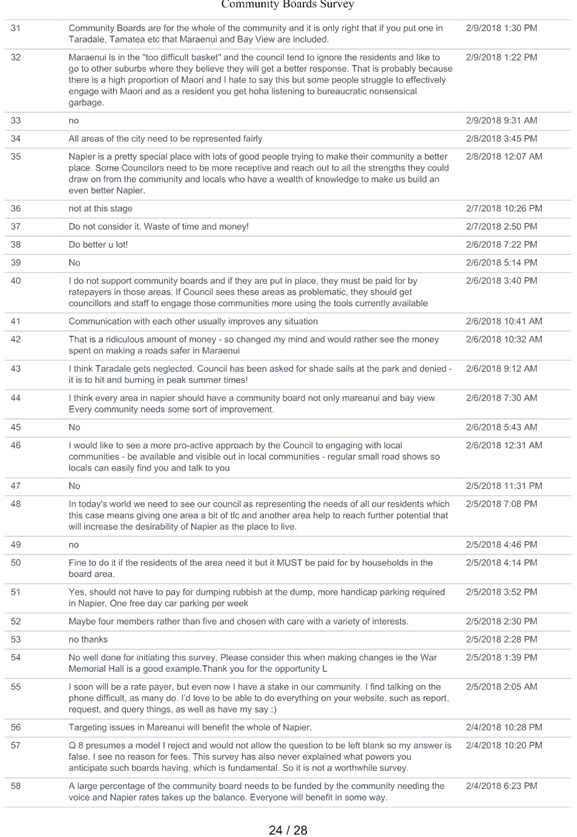

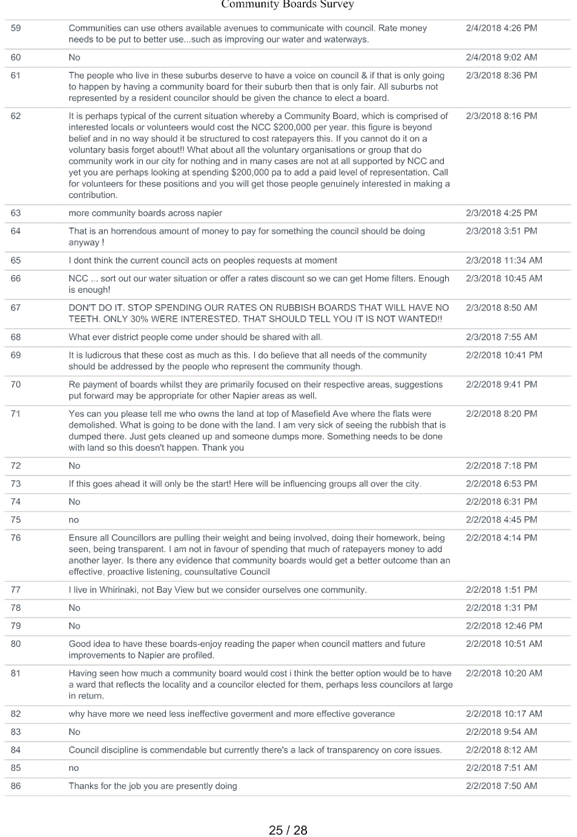

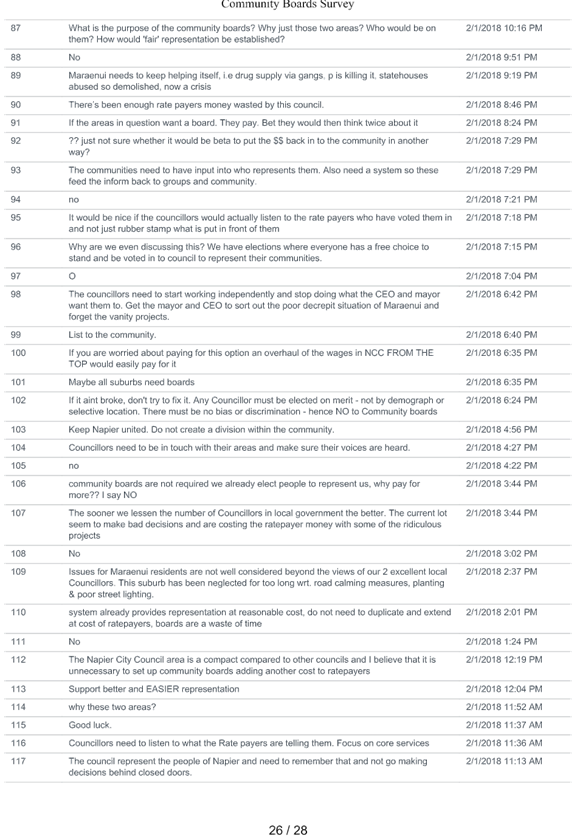

Representation Review survey report, Attachment C provides the survey responses

on Community Boards).

What are the next steps in the

process?

This report presents the analysis

of the review to inform Council’s decision on the initial proposal; this

will then be publicly notified, and submissions invited.

Once Council makes a decision on

the initial proposal, the statutory process commences.

Napier residents will have an

opportunity to provide their thoughts on the proposal via submissions once the

initial proposal is released. A hearing will be held where Council can

consider feedback from Napier residents, and decide whether to modify their

initial proposal or not. The initial proposal then becomes the final

proposal.

The final proposal will be

publically notified, and Napier residents will have the opportunity to make an

appeal or objection on the final proposal to the Local Government

Commission. At this point, it is the Commission which makes a final

determination on Napier’s representation arrangements, and Council has no

further role in deciding.

Indicative timeframes for the

statutory process include:

· Council

decision 3 April and public notice (April)

· Submission

period and consideration (April/May)

· Public

notice of final proposal (June)

· Appeals and

objections to Local Government Commission (June-December)

· Local

Government Commission considers appeals and objections (January to April 2019)

· Implementation

of determination (April-June 2019).

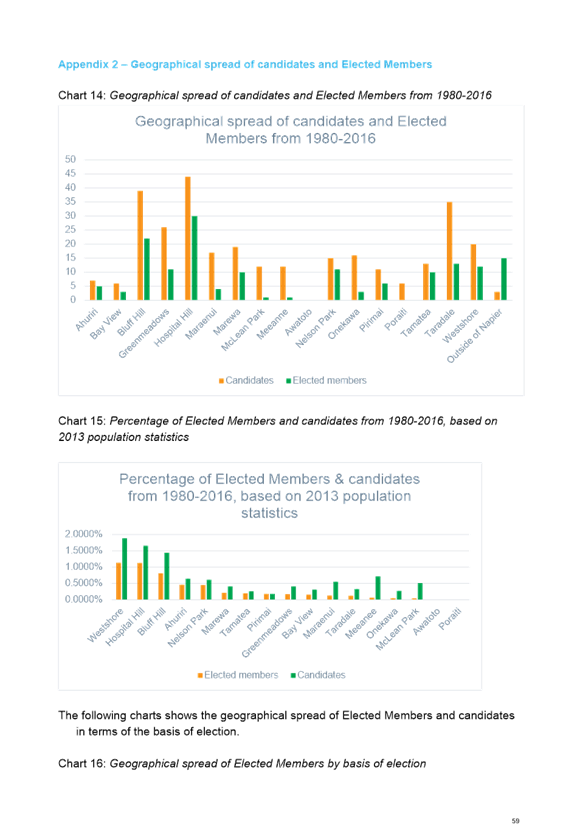

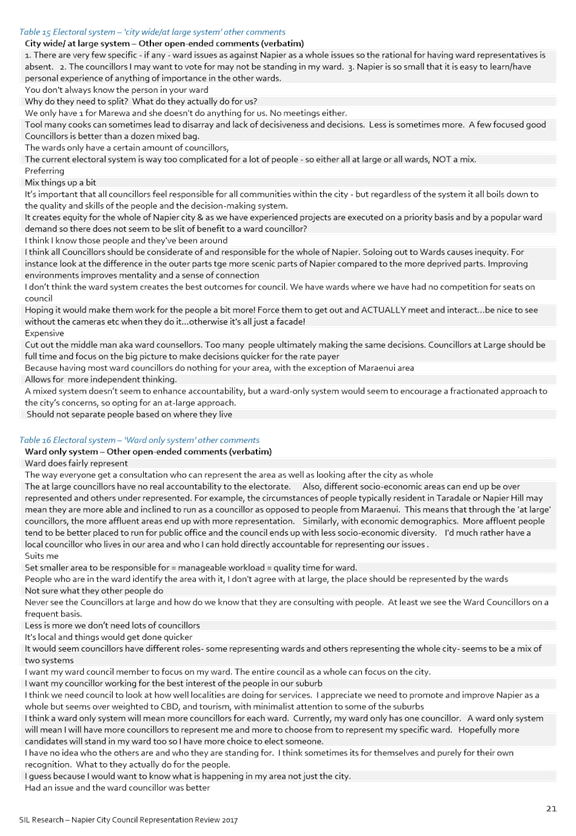

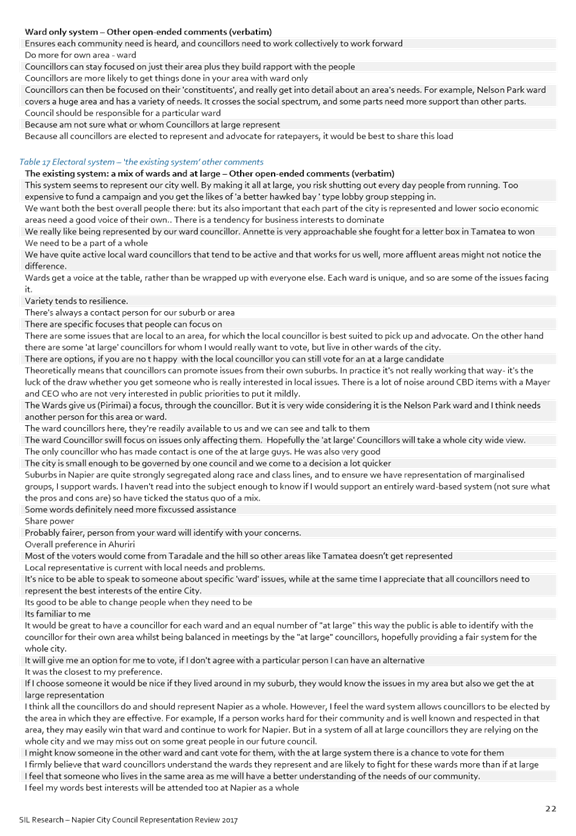

What were the key findings

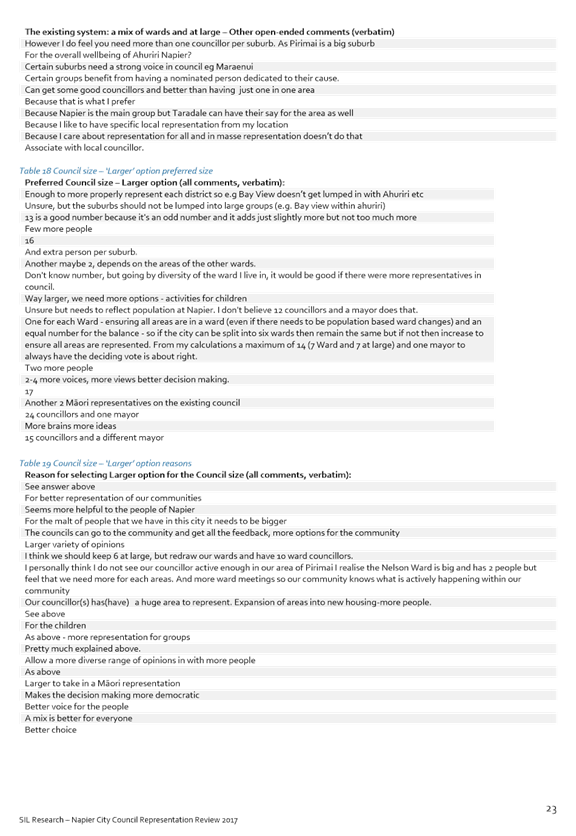

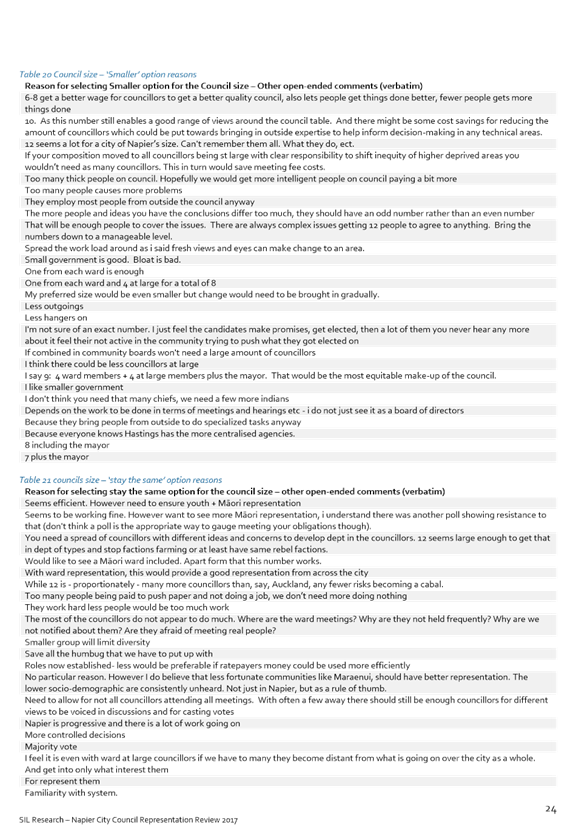

from the analysis report?

Key findings of the analysis

include:

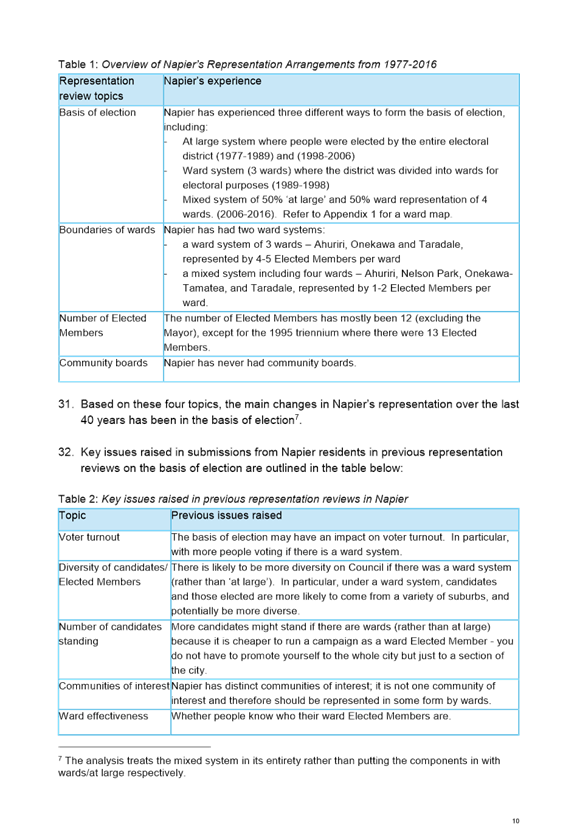

History of

Napier’s representation arrangements

· Strong local

democracy can be measured by high voter turnout, more than one candidate for each

seat, and diversity of candidates.

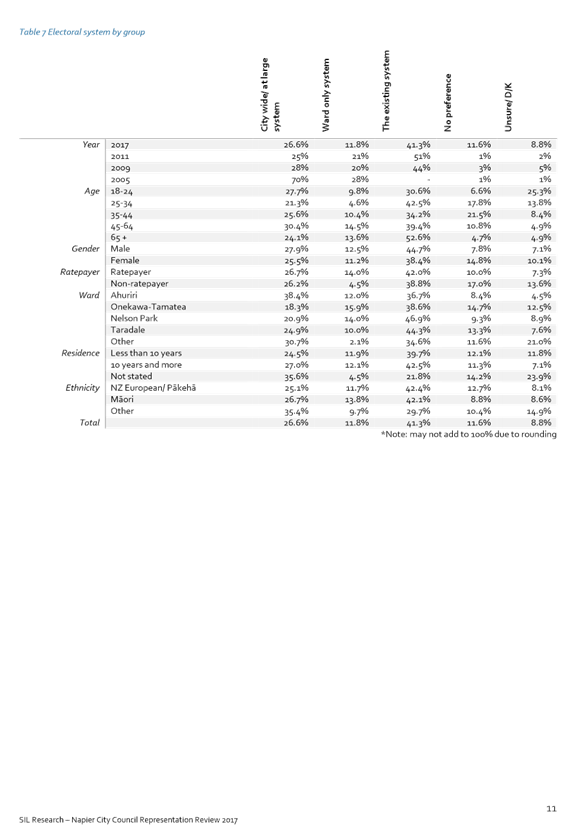

· Survey

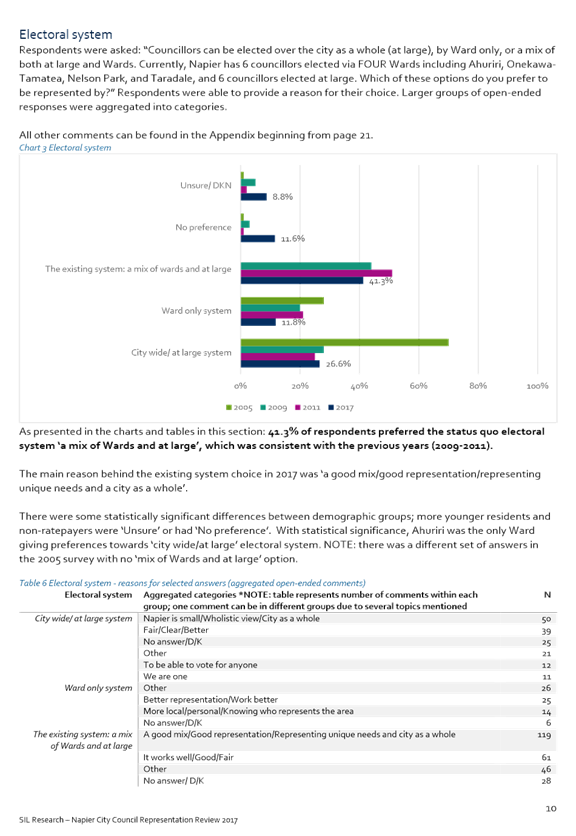

respondents prefer the current mixed election system made up of six at large

and six ward Elected Members.

· Of the three

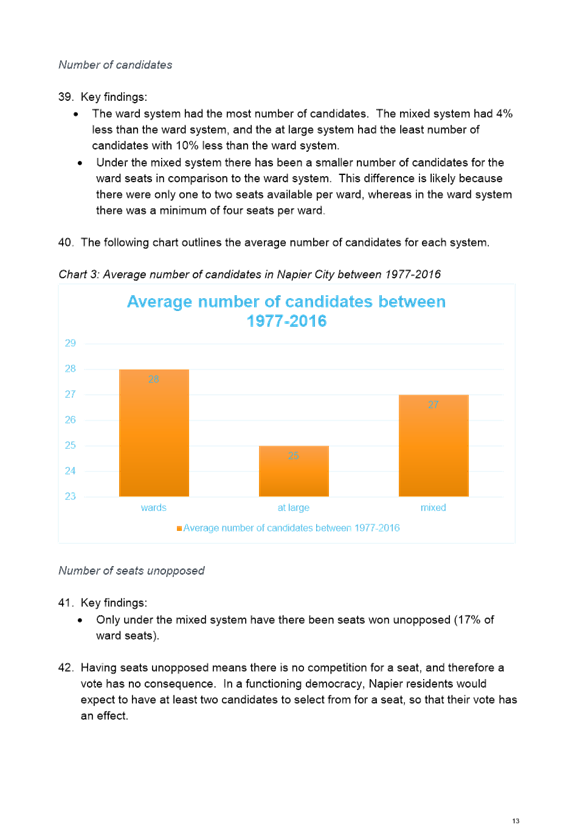

election systems Napier has had over the last 40 years, the ward system

followed by the mixed system created more fair and effective representation

than the at large system.

· Napier’s

mixed system is unusual; most councils have a ward system.

Communities of

interest

· Napier is

made up of diverse communities.

· Napier’s

suburbs have their own community characteristics.

· The current

ward system mostly caters for suburbs that share community characteristics.

· Suburbs that

are distinct have sufficient commonality among other suburbs within the current

ward structure.

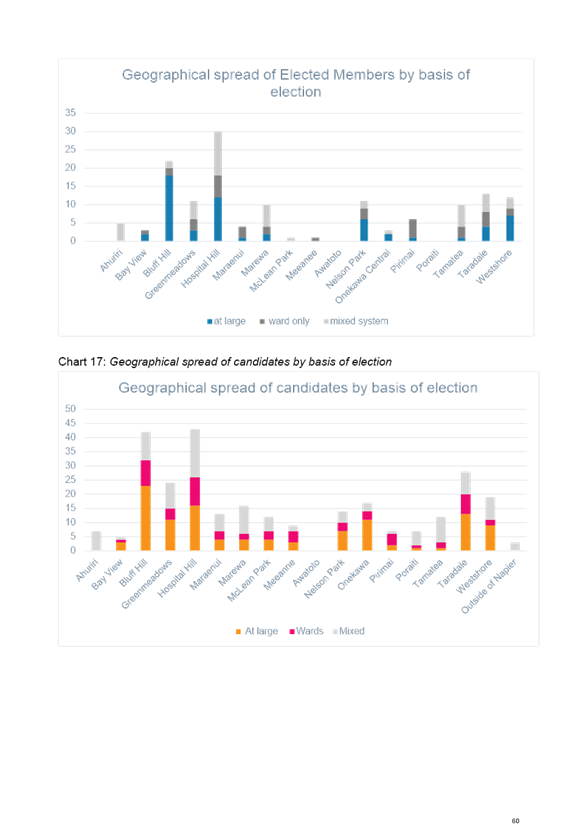

Effective representation

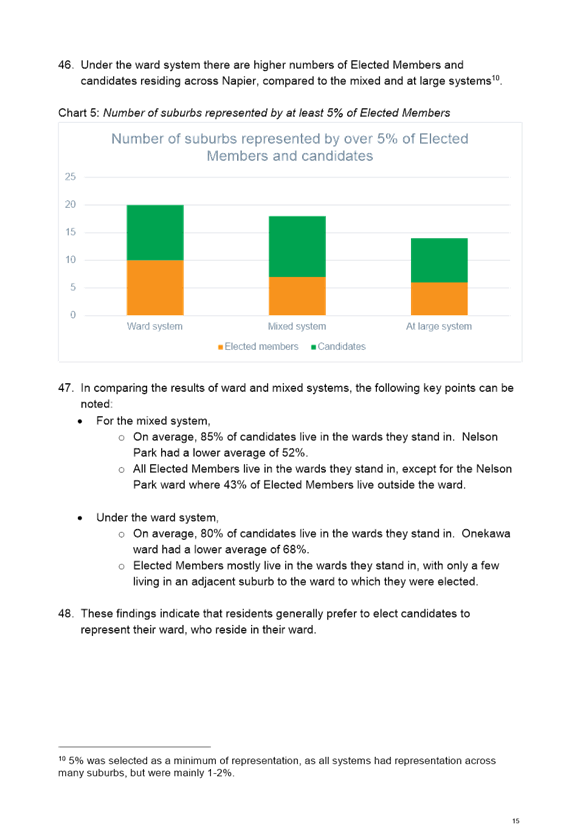

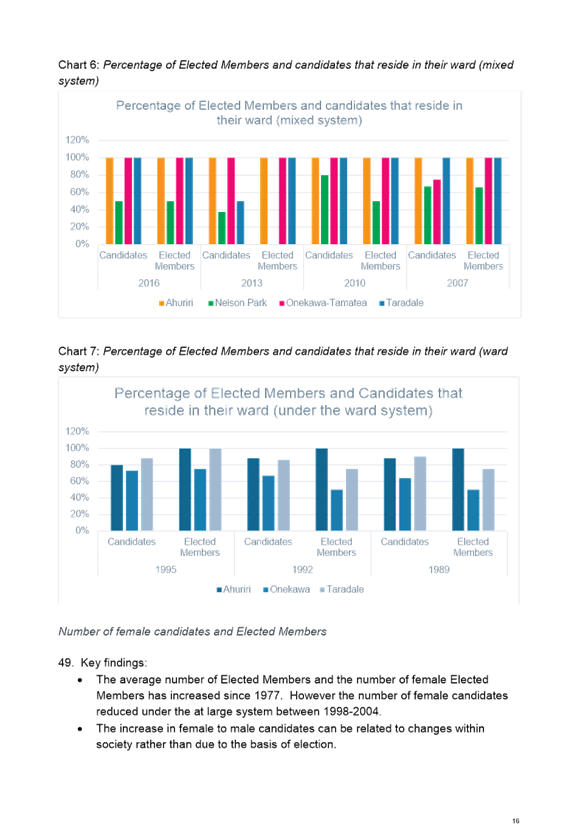

· Using the

existing ward structure, the most effective system for representing communities

of interest is the ward system, followed by the mixed system.

· The at large

system best reflects Napier residents’ feedback that their community of

interest is “Napier”, but has in the past led to less candidates,

less diversity among candidates, and lower voter turnout.

· The mixed

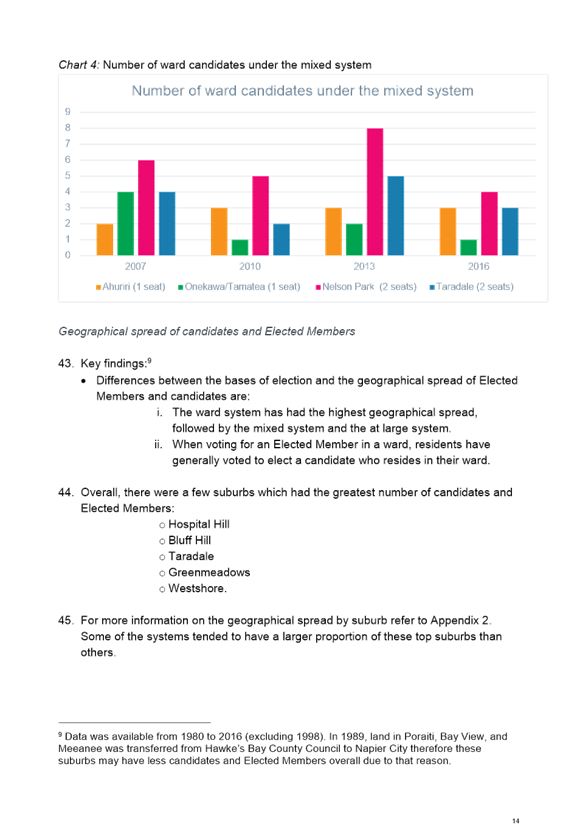

system has in the past led to single candidates for a ward seat being elected

unopposed; giving no choice to voters.

· The ward

system has in the past provided higher number of candidates and more diverse

candidates.

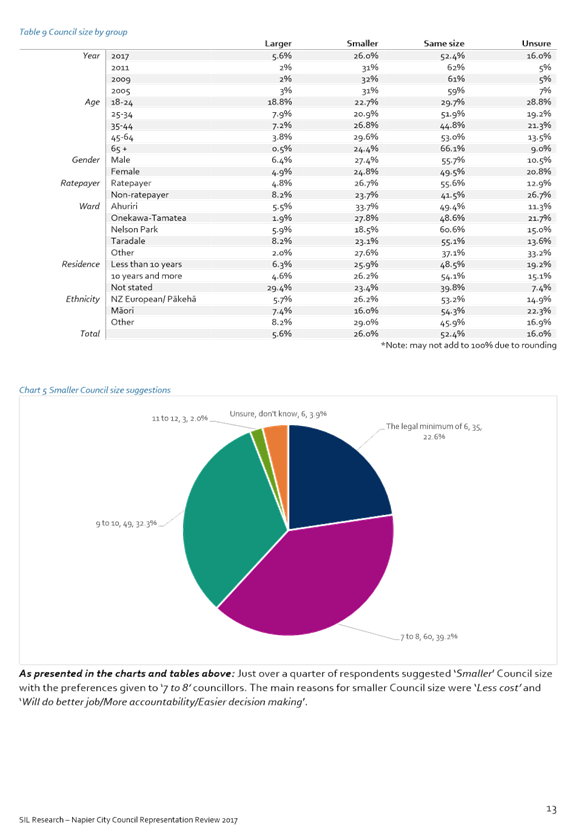

· Napier could

feasibly reduce the number of Elected Members to 10 and still be in line with

other city councils for representation ratios.

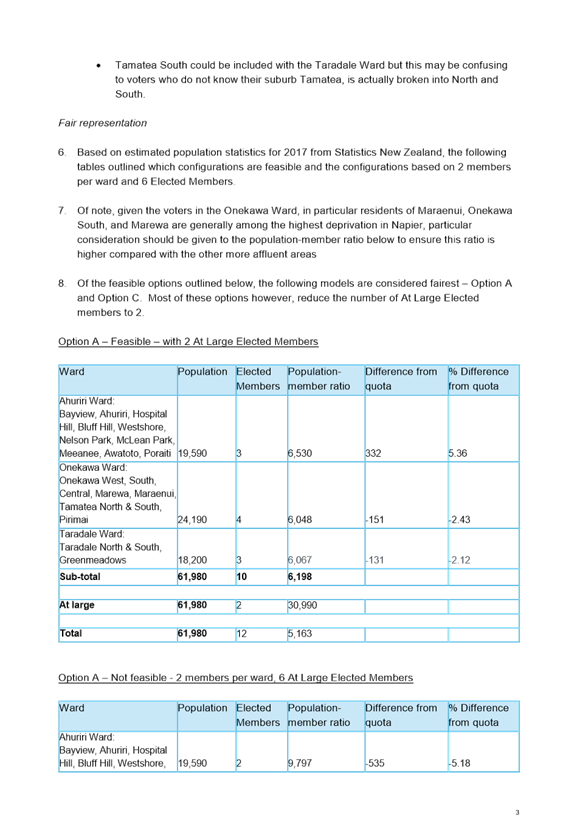

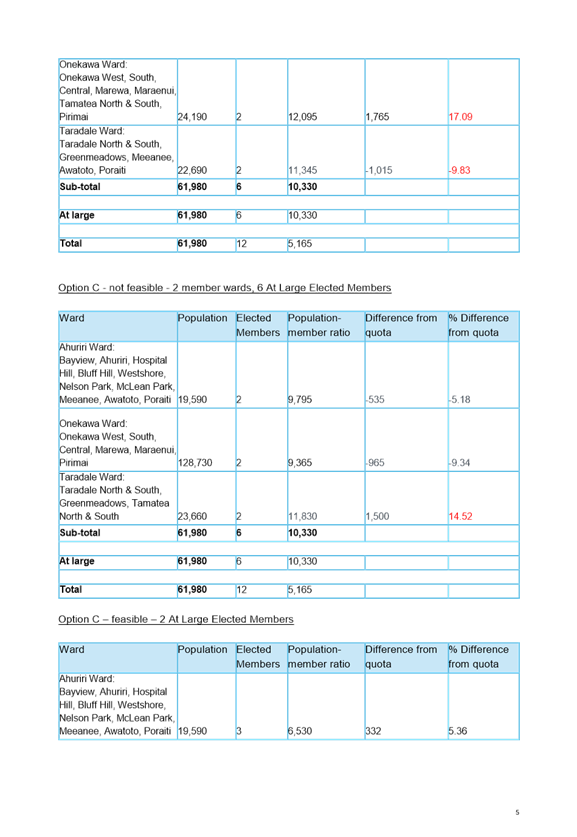

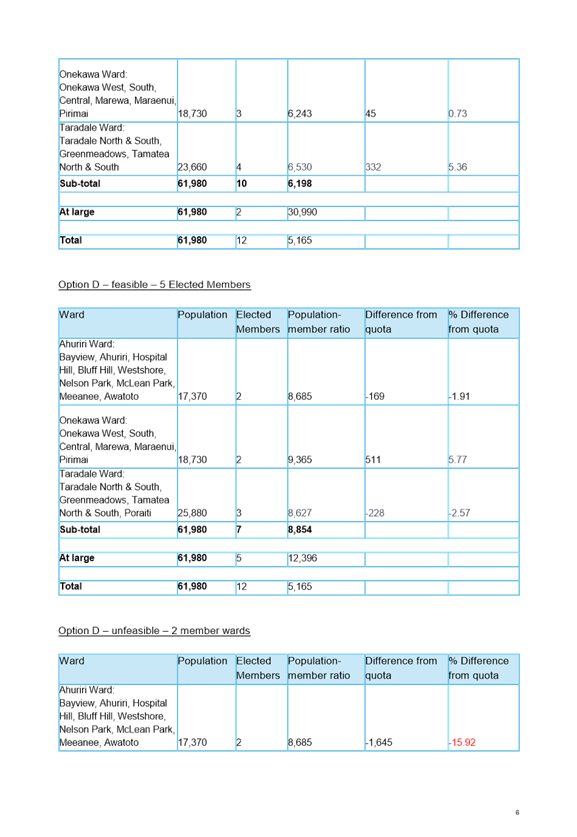

Fair representation

· Napier’s

current rate of elected members is higher in comparison to other city councils.

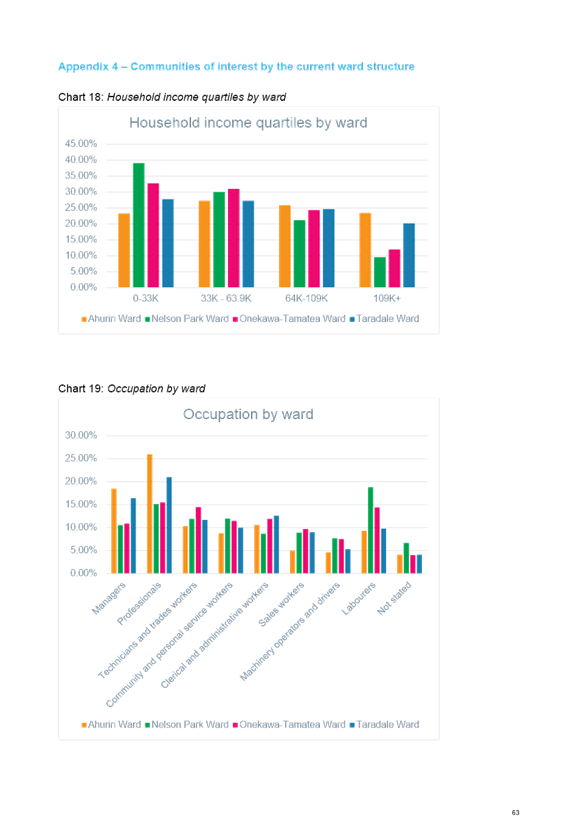

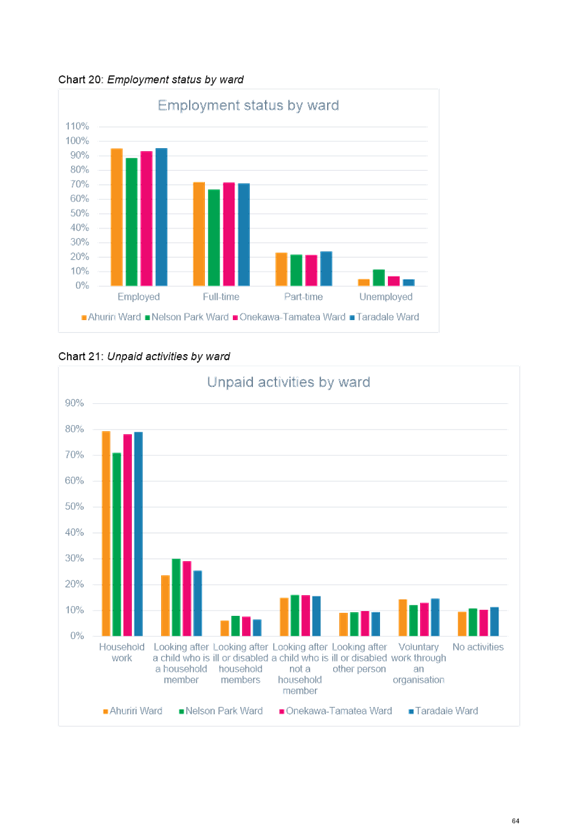

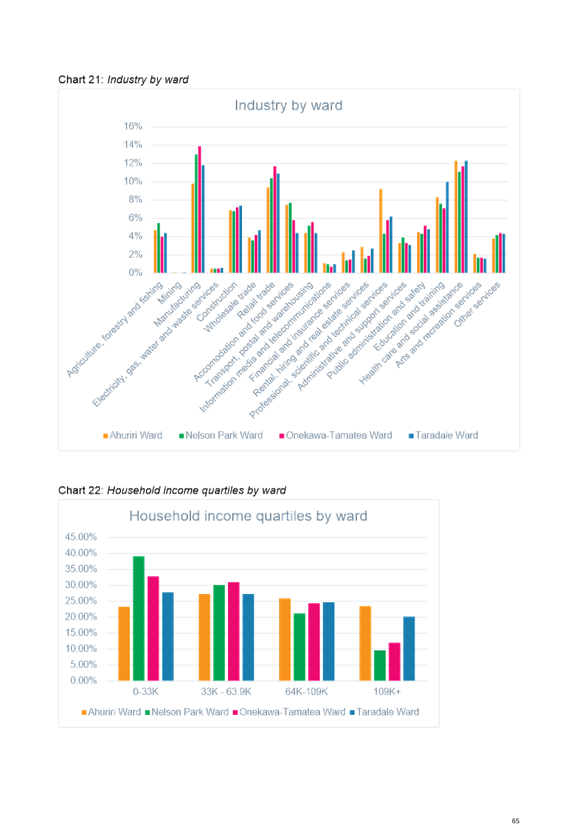

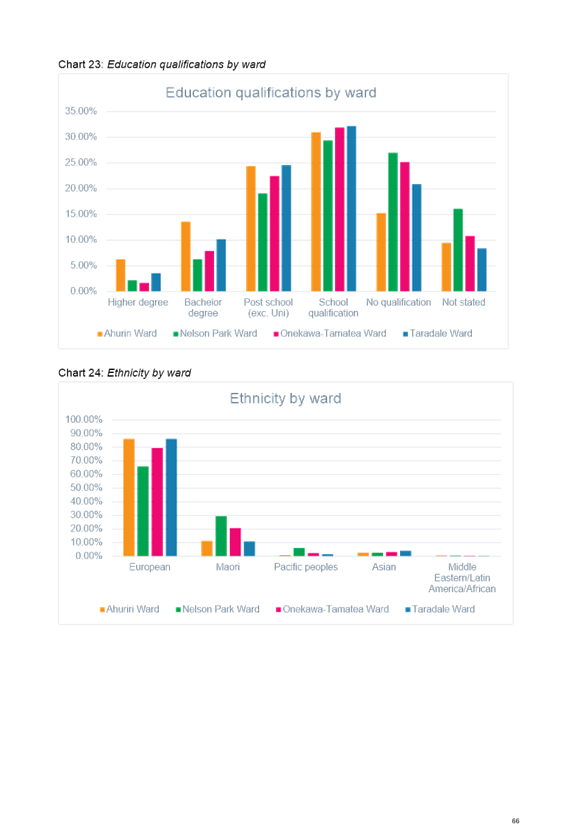

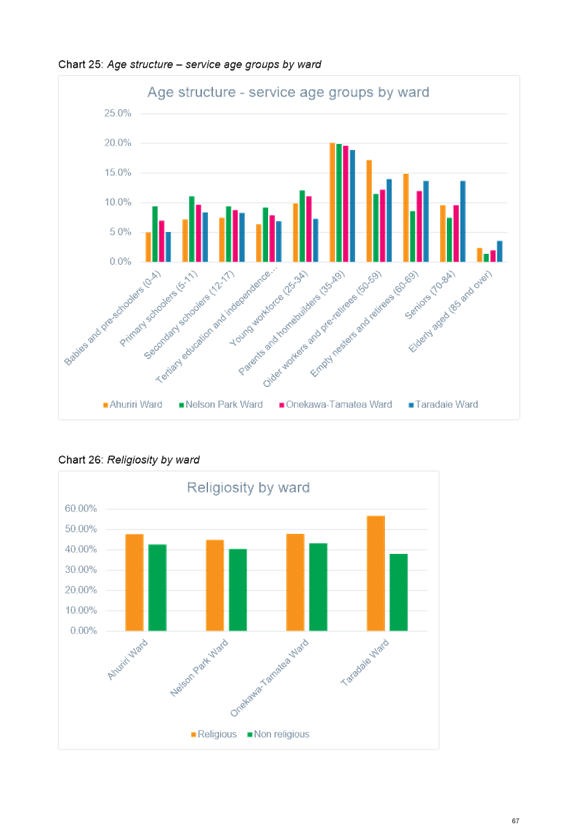

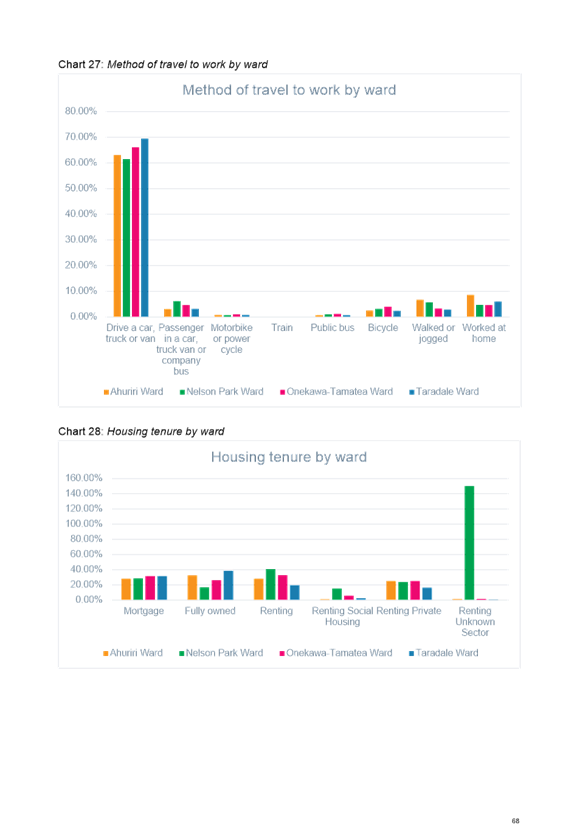

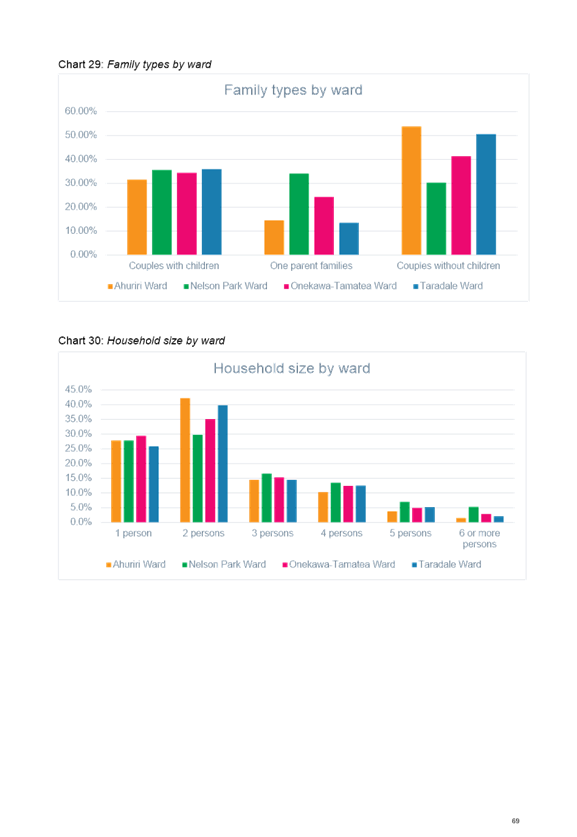

· Nelson Park

Ward residents are the least engaged in local democracy and have the highest

deprivation levels which can be a barrier to their engagement.

· Avoiding

single member wards helps to improve voter choice and representation for ward

residents.

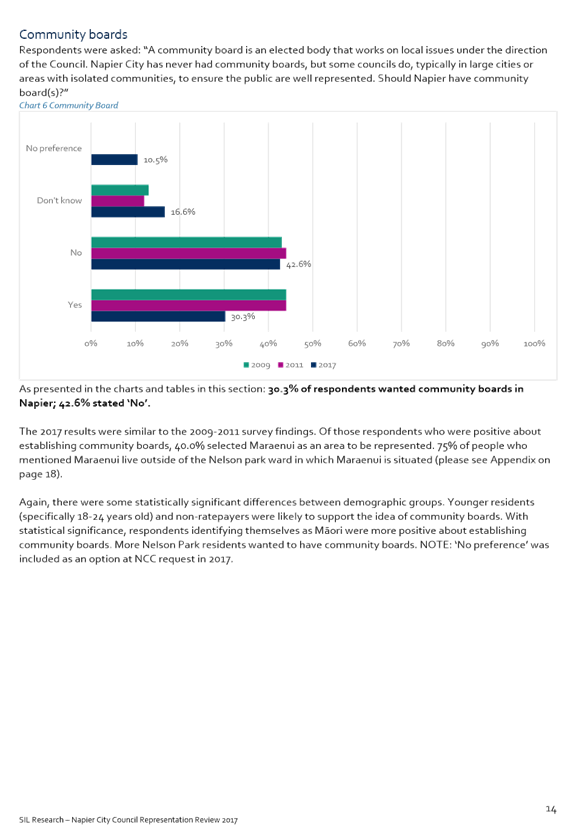

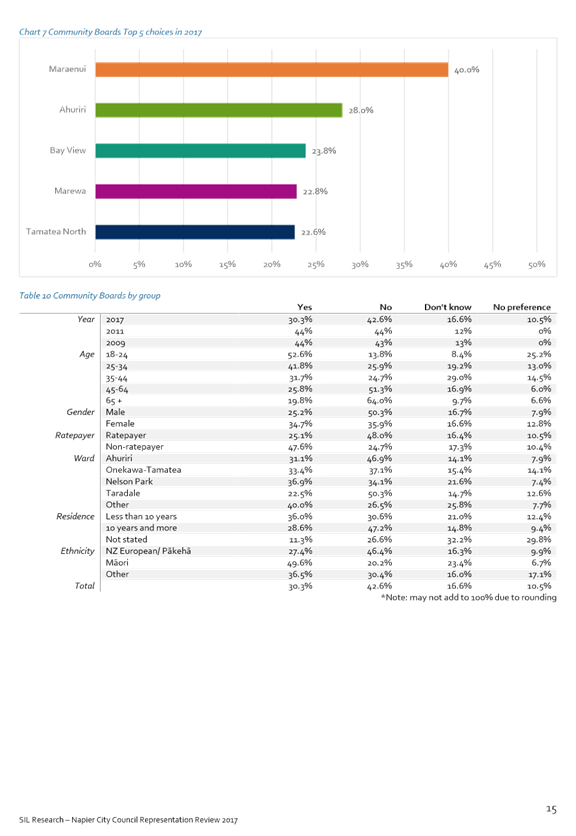

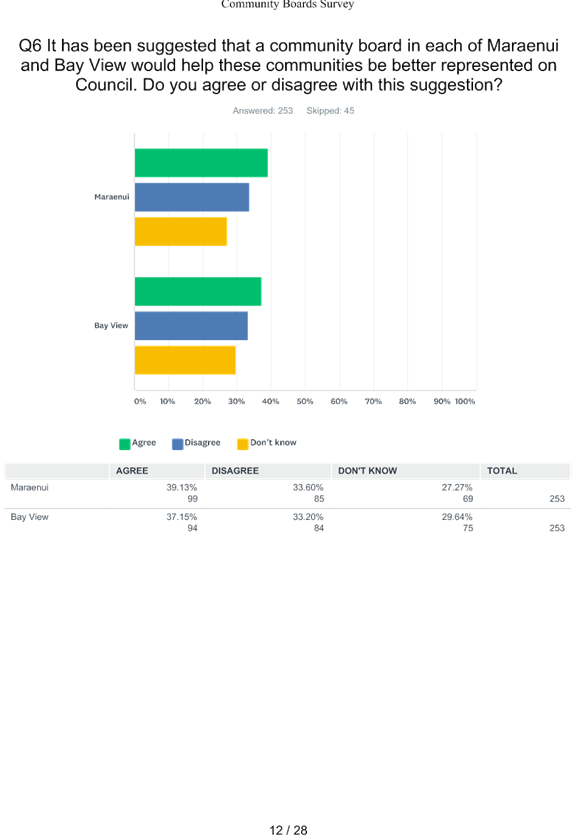

Community Boards

· Bayview and

Maraenui are distinct communities of interest for a community board.

· Survey

respondents do not have a strong preference to establish community boards, and

there is even less appetite by ratepayers to pay for them.

· Survey

respondents have identified they are seeking an improved council to community

connection.

· Improvements

to existing mechanisms can achieve the same outcomes for better

representation as a

community board might do.

The analysis paper contains

detailed information to support the key findings, and provides feasible options

for consideration.

2.3 Issues

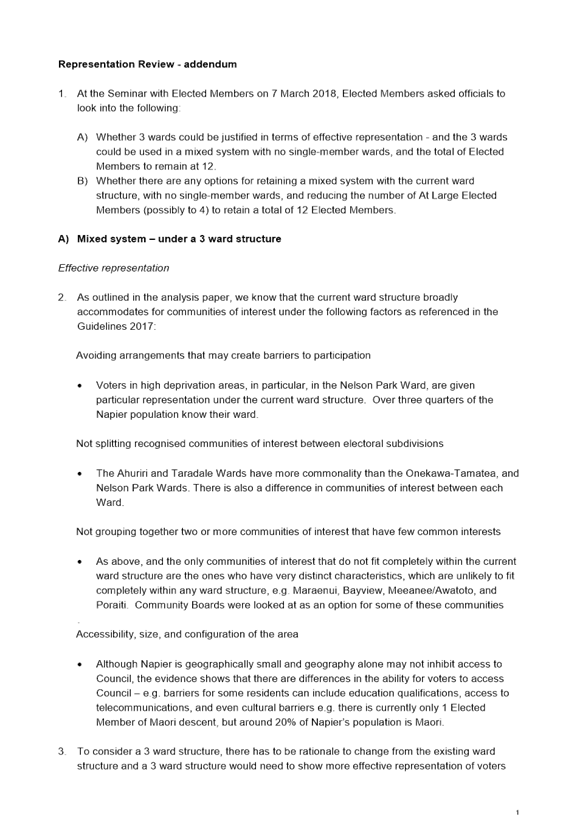

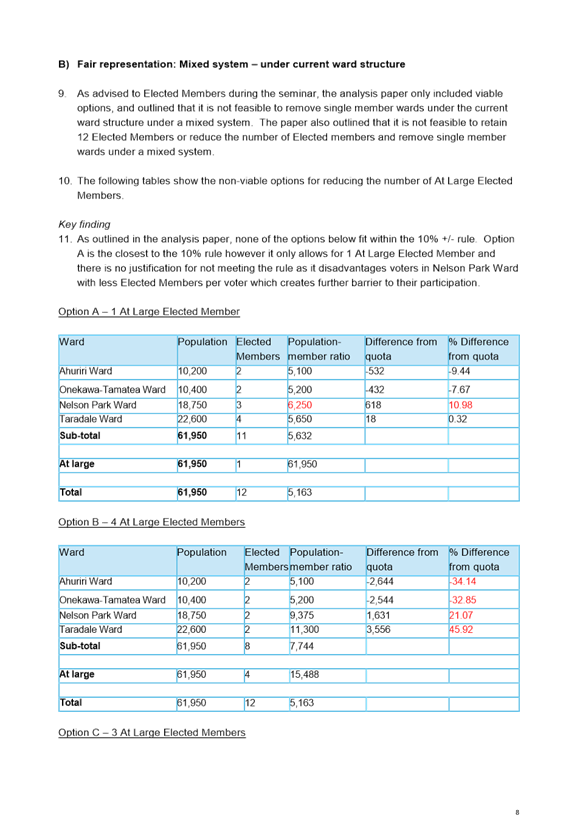

At a seminar with Elected Members

on 7 March 2018, Elected Members asked officials to look into the following:

A) Whether three wards could be justified in

terms of fair and effective representation, used in a mixed system with no

single-member wards, and the total of Elected Members remaining at 12.

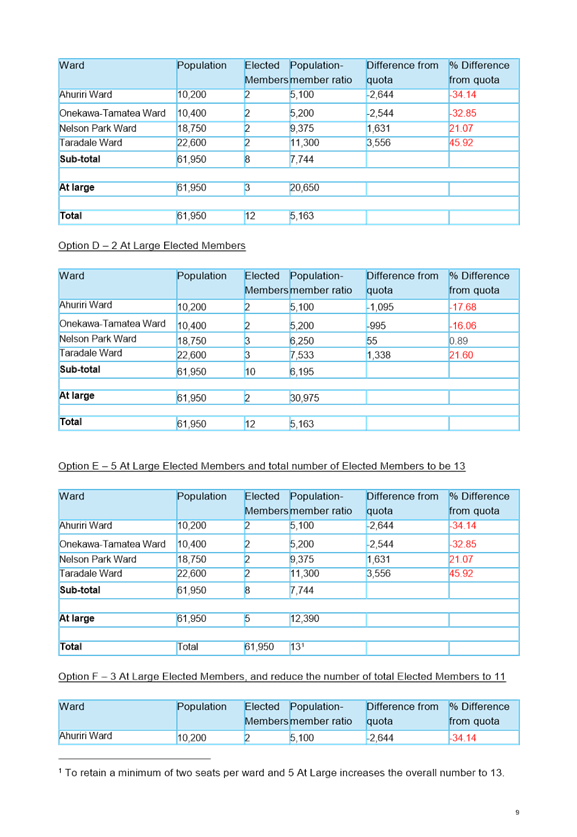

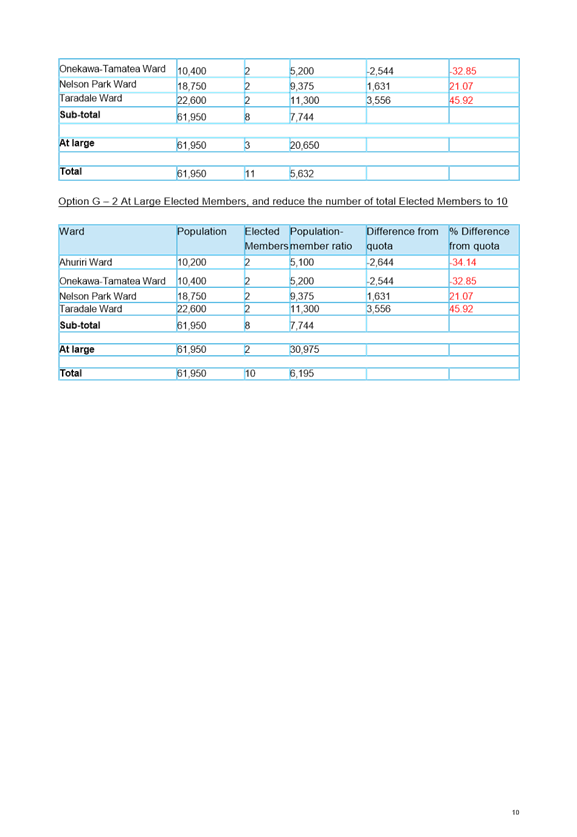

B) Whether there are any options for

retaining a mixed system with the current ward structure, with no single-member

wards, and reducing the number of At Large Elected Members (possibly to four)

to retain a total of 12 Elected Members.

Officials considered both A and B

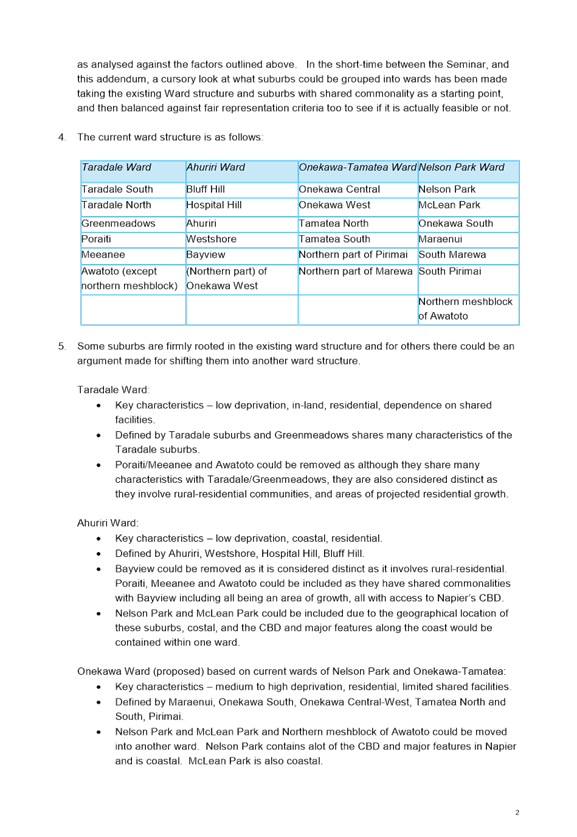

and presented the analysis to these in Attachment D.

2.4 Significance

and Consultation

Representation arrangements

affect all Napier residents and have a high degree of significance. As

outlined earlier, pre-consultation was undertaken with all of Napier’s

residents, firstly via a commissioned survey covering all representation

arrangements, and secondly via a survey undertaken by Officers on community

boards.

The statutory process under the

Act 2001 and Act 2002 includes a high level of community engagement in it, as

already outlined in this report. The statutory process will commence following

Council’s decision on the initial proposal.

2.5 Implications

Financial

There are no financial

implications with the Officer’s recommendation.

It is estimated that the cost to

establish community boards for options d ii – iv, would add up to $200,000

to rates per annum.

Social &

Policy

N/A

Risk

There is a risk that residents in

higher deprivation areas may end up with lower population-member ratios than

those residents from low deprivation areas. To mitigate this risk, the

analysis report clearly states that consideration should be given when calculating

options for fair representation to ensuring that residents from high

deprivation areas are given an adequate voice.

2.6 Options

The options available to Council

are as follows:

a. (preferred

option) Retain the current ward structure and total number of Elected Members

and move to a ward only system. No community boards are

established. Under this option:

i. current

ward structure is retained which gives particular representation to voters in

high deprivation areas, does not split recognised communities of interest

between electoral sub-divisions, and does not group together two or more

communities of interest that have few common interests.

ii. it

is more likely there will be a choice of candidates for each seat, avoid single

member wards, and provide more diverse candidates.

iii. the

number of Elected Members would remain at 12.

b. Status

Quo - Retain the status quo of representation arrangements as they currently

stand; 12 Elected Members, current ward structure, mixed system of six Elected

Members elected at large, and six Elected Members elected via wards. No

community boards.

Under this option:

i. it

is likely that there will be Elected Members who stand unopposed, thus giving

no choice for voters.

c. Retain

status quo, except for reducing the total number of Elected Members to 10 or 11

by reducing at large Elected Members to four or five. No community boards are

established. Under this option:

i. Population-member

ratios would be more in line with other city councils.

d. Community

Boards are either:

i. Not

established (preferred option).

Under this option, improvements to

existing mechanisms for the public to engage with Council, and a full ward

system with actively engaged Elected Members would provide the types of improvements

to Council/community connection that are being looked for in community

boards.

ii. Established

in Bayview.

iii. Established

in Maraenui.

iv. Established

in Maraenui and Bayview.

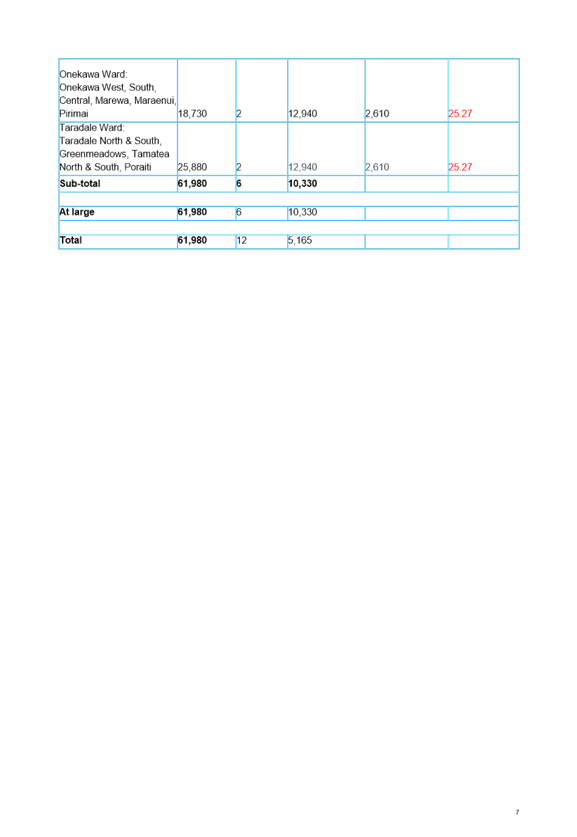

e. Three

ward system, based on:

i. Ward

configurations:

1. Ahuriri

Ward: Bayview, Ahuriri, Hospital Hill, Bluff Hill,

Westshore, Nelson Park, McLean Park, Meeanee, Awatoto, Poraiti (three Elected

Members)

2. Onekawa Ward: Onekawa West, South, Central, Marewa,

Maraenui, Tamatea North & South, Pirimai (four Elected Members)

3. Taradale Ward: Taradale North & South, Greenmeadows.

(three Elected Members)

ii. 12

Elected Members in total, including two at large Elected Members.

iii. No

community boards.

Under

this option: two at large Elected Members are retained which all voters can

vote for, so gives them a choice beyond the candidates standing for their ward;

it avoids single-member wards. It is a new ward configuration, and

therefore voters would need to become aware of it.

f. Three

ward system, based on:

i. Ward

configurations:

1. Ahuriri

Ward: Bayview, Ahuriri, Hospital Hill, Bluff Hill,

Westshore, Nelson Park, McLean Park, Meeanee, Awatoto, Poraiti (three Elected

Members)

2. Onekawa Ward: Onekawa West, South, Central, Marewa,

Maraenui, Pirimai (three Elected Members)

3. Taradale Ward: Taradale North & South, Greenmeadows,

Tamatea North & South (four Elected Members)

ii. 12

Elected Members in total, including two at large Elected Members.

iii. No

community boards.

Under

this option: two at large Elected Members are retained which all voters can

vote for, so gives them a choice beyond the candidates standing for their ward;

it avoids single-member wards. It is a new ward configuration, and

therefore voters would need to become aware of it.

For the particular sections in the

Analysis Report that support the options as outlined above, the following pages

refer:

· Pages 35-36:

Based on effective representation, the key advantages and disadvantages of each

system (e.g. at large, mixed, and wards). The two most effective options

are considered to be to retain the mixed system, or move to a ward system.

· Pages 37-38:

For Council size, the two most effective options are considered to retain the

status quo of 12 or reduce to 11 or 10.

· Pages 41-43:

For fair representation, the two options are to retain the mixed system and

current ward configuration and number of Elected Members per wards, and reduce

the number of at large Elected Members to 11, or to move to a ward only

system based on the current ward configuration.

· Pages 53-54:

For analysis on Community Boards.

Pages 1-7:

Addendum (Attachment D) for analysis on three ward configuration.

2.7 Development

of Preferred Option

Option A is the preferred option due

to the benefits as outlined above.

2.8 Attachments

a Representation

Review: Analysis Report ⇩

b Representation

Review survey report ⇩

c Community

Board survey responses ⇩

d Representation

Review addendum ⇩