|

Audit and Risk Committee - 12 June 2020 - Attachments

|

Item 2 Attachments a |

Audit and Risk Committee

Open Agenda

|

Meeting Date: |

Friday 12 June 2020 |

|

Time: |

1pm |

|

Venue: |

Large Exhibition Hall Napier War Memorial Centre Marine Parade Napier |

|

Committee Members |

John Palairet (In the Chair), Mayor Kirsten Wise, David Pearson, Councillor Nigel Simpson and Councillor Graeme Taylor |

|

Officer Responsible |

Director Corporate Services |

|

Administration |

Governance Team |

|

|

Next Audit and Risk Committee Meeting Friday 18 September 2020 |

Audit and Risk Committee - 12 June 2020 - Open Agenda

ORDER OF BUSINESS

Apologies

Nil

Conflicts of interest

Public forum

Nil

Announcements by the Mayor

Announcements by the Chairperson

Announcements by the management

Confirmation of minutes

That the Minutes of the Audit and Risk Committee meeting held on Friday, 20 March 2020 be taken as a true and accurate record of the meeting............................................................................................. 60

Agenda items

1 Wastewater Outfall Report.............................................................................................. 3

2 Summary of Napier Water Safety Plan's Risks.............................................................. 13

3 Health and Safety Report.............................................................................................. 19

4 Draft Annual Plan 2020/21............................................................................................ 24

5 Sensitive Expenditure - Mayor and Chief Executive...................................................... 36

6 External Accountability - Investment and Debt Report.................................................. 49

7 Risk Management Report June 2020............................................................................ 51

Public excluded ............................................................................................................. 58

Audit and Risk Committee - 12 June 2020 - Open Agenda Item 1

1. Wastewater Outfall Report

|

Type of Report: |

Legal and Operational |

|

Legal Reference: |

Resource Management Act 1991 |

|

Document ID: |

933764 |

|

Reporting Officer/s & Unit: |

Catherine Bayly, Manager Asset Strategy Cameron Burton, Manager Environmental Solutions |

1.1 Purpose of Report

To provide the Audit and Risk Committee with an update on the Wastewater Outfall, noting a similar report has gone to Council to:

· inform Council of an update to the status of the Awatoto Submarine Wastewater Outfall which conveys treated wastewater to the Pacific Ocean, and to;

· enable decisions to be made to bring forward funding for an expedited repair, renewal or replacement of the outfall structure.

|

The Audit and Risk Committee: a. Note the current status of the submarine wastewater outfall: i. There remains some seepage of wastewater from sealing gaskets which form part of a bespoke fibreglass joint section of the subsurface outfall pipe structure; ii. Despite efforts, staff have not been able to identify a way to quickly fix this seepage without putting the fibreglass joint at risk of rupturing; iii. That frequent testing of the coastal waters surrounding the area of seepage continues to show de minimus environmental effect of those waters, caused by this seepage; iv. That

Hawkes Bay Regional Council (HBRC) have recently indicated (on 25 March 2020)

that Council must take the following actions: v. That HBRC have informally notified Council of their intention to pursue enforcement action against Napier City Council to cease the discharge at the joint if the timeframes above are not met. vi. That a further leak has been discovered within 100m of the fibreglass joint. Divers have been to the site with the aim to repair and have found that this is an old repair that has been damaged by an anchor, or other, and will need an additional repair. vii. Tight timeframes to effect a repair increases the risk associated with delivering a short-term fix, rather than facilitating long-term solutions which will provide better outcomes. b. Officers are seeking approval by Council to: i. Seek a variation to the current resource consent to authorise the discharge of wastewater via seepage at a position other than that currently authorised (at the fibreglass joint location); ii. Seek early provision of funding assigned for later financial years in the Long Term Plan (LTP) to enable the strategic and planned replacement of the wastewater outfall, including better treatment options to facilitate a more highly treated wastewater in the future. c. Note that funding to be released from Wastewater Reserves to attempt a fix of the two seepages and to start on investigation works for replacement of the outfall ($2m has been put forward in the 20/21 Annual Plan). d. Note attempt the lowest risk repair option of the fibreglass joint to address Regional Council’s repair timelines. e. Note the Beca Ltd Report entitled “Napier City Council – Wastewater Outfall – Issues and Options” dated 15 May 2020. f. Note the Audit and Risk Committee may request further information in relation to this issue that they may require in order to fully understand the risk to Council and the community if not already provided in the report. This committee has the ability to provide any feedback on the risk assessment based on the preferred options presented as part of this paper and/or may any recommendation to Council.

|

· The 1.54km long wastewater sea outfall pipe was installed in the 1970s. The outfall pipe had issues from early stages due to poor construction methodology and design. The pipe has been installed in two sections and connected with an in-situ joint approximately 700m offshore. Due to a misalignment of the pipe ends at the joint, a fibreglass joint was installed in 1984. This joint is the weakest point of the outfall pipe.

· According to available information, the designed vertical alignment of the pipe was not met during construction. The seaward end of the diffuser settled below the seabed at an early stage after construction, causing issues with performance of the diffuser. Inspection of the pipe has revealed several historical leak repairs to the pipe. Overall, there have been many issues with the outfall pipe and diffuser from the beginning.

· Historically the submarine outfall has not been regularly inspected. As part of recent improvements to planned maintenance, divers inspect the pipeline and diffusers annually. During these inspections, ports of the diffusers are cleaned. However, not all the diffuser ports are functioning due to blockages, missing diffuser parts (damaged by fishing trawlers or logs rolling on the sea bed) or they are buried under an ever-changing seabed.

· In 2018 specialist diving contractors were engaged to undertake a condition assessment over the full length of the outfall pipeline.

· In August 2018, diving investigations found several sticks, pine cones, fishing net and weed inside the outfall.

· The specialist divers found a small leak coming from the pipeline approximately 70 metres from the shore. This leak was subsequently fixed using stainless clamps and rubber sheaths and subsequent assessments have found this to be in good condition.

· The divers also found an area of more significant seepage discharging from rubberised gaskets between a one-of-a-kind custom-built fibreglass joint section, 700m from shore. The seepage has been calculated at approximately 10 litres per second, when normal flow is in the order of 300-400 litres per second.

· Visibility is zero at the site, due to coastal interaction with the river sediment in the area.

· In late April 2020 an additional plume slightly closer to shore from the joint was discovered during a drone monitoring inspection. This seepage is from a previous repair that has now failed. The dive team believe that the pipeline at this point has sustained a significant impact. Divers were mobilised at the start of May and have identified an old repair with a steel clamp and cement bags. There are longitudinal and radial cracks in the pipe under the clamped section and there has been some displacement of the pipe. Although it was intended that a repair be made at that time, this was not possible as the required repair was deemed to be more complex than anticipated.

· HBRC were notified of the second seepage by phone and email on the 5th May 2020.

· Work is underway to legally protect the outfall under the Submarine Cables and Pipelines Protection Act 1996, (the same piece of legislation that protects the power cables under Cook Strait). This allows much larger penalties for those who are found to have caused damage, than what is currently available.

· The consent for the Outfall expires in 2037

· The capacity of the outfall is currently constrained due to the integrity of the historical repairs. The Wastewater Treatment and Outfall Master Plan that is currently being developed and produced later this year will help to determine future requirements for the full replacement of the outfall.

Systematic seepage detection:

· There is no formal process for seepage detection and for such a challenging coastal environment. It is very difficult to detect small seepages.

· Pressure monitoring is undertaken and recorded, but the nature of the system is such that the operation of the pump and air valve along with the tide and wave action are likely to mask any small seepages.

· There are frequently large movements of sediment in the bay (up to 1.5m) following storms which can bury the pipeline which can also have an effect on monitoring.

Offshore Environmental Monitoring:

As well as monitoring the quality of the raw and treated wastewaters being discharged to the outfall and subsequently the ocean, the Environmental Solutions Team carry out environmental effects monitoring by boat at the authorised discharge site.

Since the discovery of the seepage from the joint in 2018 the Environmental Solutions Team have increased surveillance of the site, including:

· review of footage from the specialist divers;

· scheduled deployment of our drone to provide aerial imagery of any visible plumes;

· additional environmental effects monitoring by boat in set positions immediately above and in a series of positions surrounding the joint;

· bacteriological nearshore sampling along the coast from East Clive to Town Reef to ascertain trends and effects;

· installed cages of mussels which after a period of saturation were analysed for viruses to ascertain impacts of the wastewater outfall and seepage upon human health of those collecting kai moana;

· initiated a variation to the current resource consent to authorise the additional seepage from the joint.

It is this proactive monitoring that has ascertained the second area of seepage, further towards the shore from the joint.

To date, the laboratory analysis of samples collected have shown very little impact caused by the seepage at the joint. Results are variable due to multiple factors at the site, but the following table provides a summary of findings of Faecal coliforms:

|

Date |

Faecal coliforms at diffuser |

Faecal coliforms at the joint |

|

27 Aug 2018 |

N/A |

<1 cfu/100mL |

|

12 Nov 2018 |

700 cfu/100mL |

<1 cfu/100mL |

|

12 Mar 2019 |

500 cfu/100mL |

38 cfu/100mL |

|

09 May 2019 |

3,500 cfu/100mL |

30 cfu/100mL |

|

16 Aug 2019 |

2,100 cfu/100mL |

<1 cfu/100mL |

|

06 Nov 2019 |

<1 cfu/100mL |

<1 cfu/100ml |

|

13 Jan 2020 |

8,100 cfu/100mL |

<1 cfu/100mL |

|

29 Jan 2020 |

11 cfu/100mL |

6 cfu/100mL |

|

18 May 2020 |

Samples still being analysed at time of writing |

|

In addition to this ocean surface monitoring, we have had the divers conduct sampling of waters surrounding the joint to ascertain levels of dilution at the joint, and at 2 metres and 5 metres above and 2 metres and 5 metres away on North, South, East, West headings.

Again, results are variable depending upon ocean swells, currents and pumping rates at the time of the sampling, but do not show significant impacts.

For the nearshore coastal waters monitoring since 2018 the highest recorded levels of Faecal coliforms were 130 cfu/100mL at Short Groyne (adjacent the Hastings wastewater discharge), and 38 cfu/100mL at the joint (as shown above). From a public health perspective, through the possible collection of kai moana at Town Reef, the highest reading to date is 4 cfu/100mL.

The Environmental Solutions Team will continue required monitoring and additional monitoring, and will soon carry out another virus assessment using mussel cages and will continue to build on data including additional subsurface dispersion sampling from the divers when next engaged.

Possible Repair Option:

NCC engaged Beca Ltd to provide an “Issues and Options” report for the main leak on the outfall. All of the options have similar risks, with the most notable being the potential to damage the joint to the point where a large volume of wastewater is discharged at 700m offshore instead of the consented discharge point, 1.5km offshore.

Repairing the fibreglass joint leak has a number of constraints. The main constraints are:

· Available storage at the treatment plant for a shutdown of the plant is enough only for approximately 4 hours at normal dry weather flows. There is a risk of not completing the repair within this time period, only simple repairs can be completed without having additional storage at the plant.

· The fibreglass joint is fragile and any disturbance to the fibreglass or pipe supports during the repair may disjoint the pipe making it difficult to re-joint / re-attach the fibreglass joint.

· This is a pre-stressed pipeline and maintaining the continuity of structural integrity of the pipe during the repair is not easy in a soft, changing seabed.

· Site conditions: Working on the seabed in often zero visibility, weather and sea state.

Council’s Infrastructure team, and the Beca team have identified a number of repair options, these are summarised in the following table:

|

Repair Option |

Indicative cost ($) |

Comments |

|

Inserting a caulking cord or hemp into the flanged joints. Recommended |

$200,000 plus 1 week to undertake

|

Medium risk. Cost is relatively low. The success of this option is unknown and may be limited. This option can be actioned prior to HBRC’s deadline. |

|

Grout encasement of whole joint including supports Not Recommended |

$500,000 Specialist Construction. 2 months |

Medium to high risk. May take a longer time to repair causing storage issues at the plant. This places a large deadweight at two pipe sections, potential for settlement and further damage to the surrounding concrete pipe. Additional storage at the treatment plant would be required. |

|

Grout filling of the fibreglass box Not Recommended |

$500,000 1 week |

High to Extreme risk. Grout may block the pipe and diffusers partially or fully. The structure inside of the fibreglass box has not been confirmed. |

|

Install a PE sleeve liner Not Recommended

|

Not costed 3 months Not currently feasible |

Outfall might have to be taken out of service for up to 8 weeks. This option is not viable given the unknown internal pipe condition and obstructions, miss alignment at the fibreglass joint, no storage, and a reduction in internal diameter impacting flow rates. |

|

Install a chamber and new seaward half of the outfall Not Preferred |

$12m estimate Several Months |

It is not advisable to replace half of the outfall without the results of the WW Treatment and Outfall and Master plan. It would be more cost effective to undertake a full planned replacement. |

|

Consent Variation Underway |

$100,000 |

Enable the fibreglass joint leak to continue until the assets is replaced if the repair is not effective. |

|

Early Replacement of the Outfall Preferred |

$33-$40 million (requires investigation) 12 months plus investigation and consenting period |

Investigation works can be started to get the replacement project underway. The value of the replacement could be $20-$40m, more work is required to develop a reasonable cost estimate. |

The lowest risk option for the repair of the fibreglass joint section and associated o-ring seals and bolted sections would be:

· Diving on the pipeline at a time where tidal action, wave action and availability of specialist divers aligned;

· Cessation of discharge of wastewater by shutting down the wastewater treatment plant for a period of time;

· Unbolting the top part of the fibreglass joint section;

· Scraping detritus build-up to enable a smooth working area;

· Inserting greased rope and o-ring seals;

· Re-installing the top part of the fibreglass joint section.

There are significant risks associated with any repair option. Risks associated with the proposed option are identified in section 1.5.

Variation to Resource Consent

· A variation to the current resource consent is nearing completion which seeks to authorise the discharge of treated wastewater at an additional position, being the joint.

· The intention is to conditionally authorise the seepage discharger of treated wastewater at the joint, as Council are not currently legally authorised to do so. This will be a short-term consent to relieve some pressure until a permanent solution to the outfall pipe is implemented.

· An Environmental Effects Assessment has been developed by the Environmental Solutions Team, and this is awaiting an external peer review from a marine ecotoxicologist to enable independence prior to lodging with Hawkes Bay Regional Council.

· This application will proffer under the Augier Principle an emergency response plan which is to be developed both to address any sudden break in the outfall pipe (in any position), but also to address concerns of a breakage caused by the expeditiousness imposed upon Council to enable a short-term repair attempt. The choice of repair type and the methods of said repair, will mean the emergency response plan has to be dynamic enough to address the implications of a failure due to that repair.

· It is likely that lodgement of this application for variation to the resource consent could be made as soon as the week of the presentation of this paper.

Outfall Renewal

The Wastewater Outfall is nearly 50 years old. The recently identified seepage at an old joint is indicative of the condition of the structure and highlights that Council will need to increase expenditure to keep the outfall operational and operating within its consent conditions. This additional seepage also highlights the increasing risk of failure of the asset.

With escalating maintenance costs, current capacity constraints and increased risk of failure, it is recommended that Council start preparing for the replacement of the outfall and identify required funding to start this process prior to the consent renewal.

1.3 Issues

· Pre 2003 there have been 8 significant leaks that have been repaired.

· 2018 Small seepage at 70m – repaired.

· 2018 Larger seepage at 700m.

· End of diffuser is plugged as it is 1-5m below seabed, full length not used.

· Diffuser 120m long, including pre-tensioned structure.

· News smaller seepage discovered at 600m offshore in May 2020.

· The outfall is constrained and does not meet the required levels of service.

· Difficult repair conditions with no visibility and dangerous conditions for divers in a contaminated environment.

· Undertaking a repair on the outfall could result in further damage to the outfall.

· There is the likelihood of enforcement action if we do not undertake a repair on the fibreglass joint by October 2020.

· The outfall is nearing end of life and the costs to maintain it and repair leaks is escalating.

1.4 Significance and Engagement

The work proposed in both the short term and longer term to repair and replace the outfall represents a significant level of investment. The proposed repair cost is included in the draft annual plan to be consulted on in May/June of this year. Investment for the renewal of the outfall will need to be consulted upon in the 2021-31 LTP.

1.5 Implications

Financial

Council’s specialist consultants have provided a quotation to undertake repairs on both of the existing leaks. While the cost of these repairs is estimated at around $250,000, Council officers recommend that Council provide $400,000 for repair attempts. This will allow for poor weather conditions or issues with repairs.

The consent variation process is estimated at around $100,000.

In the 20/21 Annual Plan, Council officers have put forward $2,000,000 for rehabilitation works for the outfall. This funding would be able to cover the costs of the two leaks repairs to rehabilitate the asset. The additional funding can be used to commence investigation and design works for the outfall replacement.

With increased risks around failures, Council will need to increase expenditure on maintenance of the outfall pipeline and will need to allow for additional leaks. These annual costs are escalating and during the next LTP period staff will be forecasting $400,000 per year to inspect and maintain the outfall.

Due to the issues with the outfall, Officers would like to bring forward the replacement of this asset. In the current Long Term Plan, a total of $11,650,000 of funding was forecast, with the majority of this occurring between 2024 to 2028 for the assets replacement.

The total cost of the replacement is estimated to be significantly more than that identified in the last LTP. Council staff recommend that the replacement of the Outfall Pipeline be brought forward, with planning works starting in 2020 and replacement provided for in the next LTP.

Social & Policy

N/A

Risk

There are significant risks associated with any repair option. Risks associated with the lowest risk option include:

· There is limited storage capacity at the treatment plant, the wastewater system wet wells and pipework which could cause an overflow to a more sensitive environment than the area at the ocean outfall;

· Time pressure because of the lack of storage being put on the specialist divers;

· High risk diving work;

· The top part of the fibreglass joint section could warp, leaving that part unable to be replaced meaning most or all wastewater would then be discharged at the 700 metre offshore position for the foreseeable future;

· Due to the top part of the fibreglass joint section being constructed in a bespoke fashion and off-alignment of the pipes, it is not able to be readily replaced;

· The removal of the top part of the fibreglass joint section could release pressure on the concrete block below the structure and cause rupture of the remaining part of the structure also meaning that all wastewater would then be discharged at the 700 metre offshore position for the foreseeable future;

· The structural capacity of the fibreglass joint section and its resilience to the removal of the top section is unknown.

The Audit and Risk Committee have the ability to further discuss the risks associated with the outfall, and to make inquiry into any line of investigation they deem appropriate and to make recommendations to Council.

It is noted that the timing of the Council meeting falls before the Audit and Risk Committee meeting, so the Committee can raise matters to the Chief Executive in advance of the Council meeting if required. There will still be the opportunity to make the views of the Committee known to Council as a result of any discussion held as part of this meeting.

1.6 Options

The options available to Council are as follows:

a. Option 1 – Do nothing. It is unlikely that the Regional Council will not agree with this option, resulting in taking enforcement action against the Council. This can also cause damage to the Council’s reputation. This option is not recommended.

b. Option 2 – Applying for a variation to the existing consent to allow discharge from the existing leak as mentioned above. Sampling results suggest that the environmental impact may be minor. There is also a risk of worsening the leak resulting in larger discharge from this location over time. A proper contingency plan has to be in place as a precaution. This option is worth proceeding with.

c. Option 3 – Repairing the damaged leak by caulking method as this is the lowest risk and least cost option. There is a risk of an incomplete seal. Careful execution of work will reduce this leak. There is still the potential that the pipeline could be damaged.

d. Option 4 – Repairing the leak by grout encasement of the whole joint. There is a high risk with this option by damaging the joint further due to weight of the repair material, which may cause further damage. This option has not been recommended by the consultant or officers.

e. Option 5 – Repairing the leak by grout filling of the fibreglass box. The repair is easier, but there is a high risk of blocking the pipe and diffusers. This option is not recommended.

f. Option 6 – replace the seaward half of the outfall and install a joint chamber – this may cost around $12m, will not address other issues around the outfall’s capacity, and does not address the risks associated with the other half of the outfall.

g. Option 7 – Replacement with a new outfall. The recent failures point to the need to expedite the renewal of the outfall and note that Council spending on maintaining the outfall is starting to increase significantly.

1.7 Development of Preferred Option

The preferred options for managing our risks of failure and enforcement actions by Regional Council are b and c above, and will involve the following:

1. Apply for a consent variation for the leakage at 700m to enable an ongoing discharge at this point until the joint is fully repaired or the outfall is replaced.

2. Develop an emergency response plan to manage additional damage or failure of the pipeline

3. Engage our specialist dive team to undertake the lowest risk repairs possible for both leaks.

4. Start planning the early replacement of the outfall to minimise risks, increase levels of service and tie in with improvements to the Wastewater Treatment Plant

a Beca Ltd "Napier City Council - Wastewater Outfall - Issues and Options" 15 May 2020 (Under Separate Cover)

Audit and Risk Committee - 12 June 2020 - Open Agenda Item 2

2. Summary of Napier Water Safety Plan's Risks

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |

|

Document ID: |

933756 |

|

Reporting Officer/s & Unit: |

Catherine Bayly, Manager Asset Strategy |

2.1 Purpose of Report

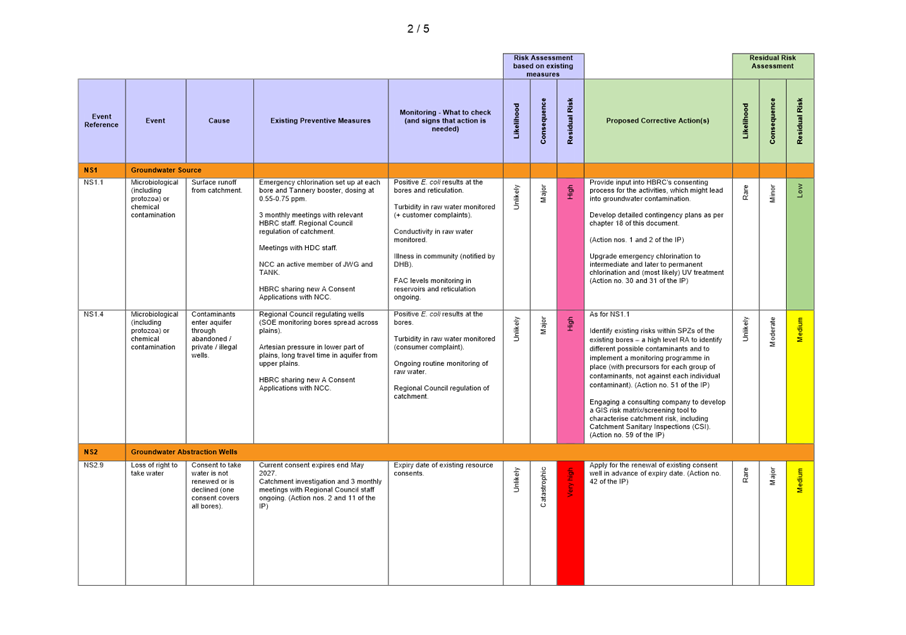

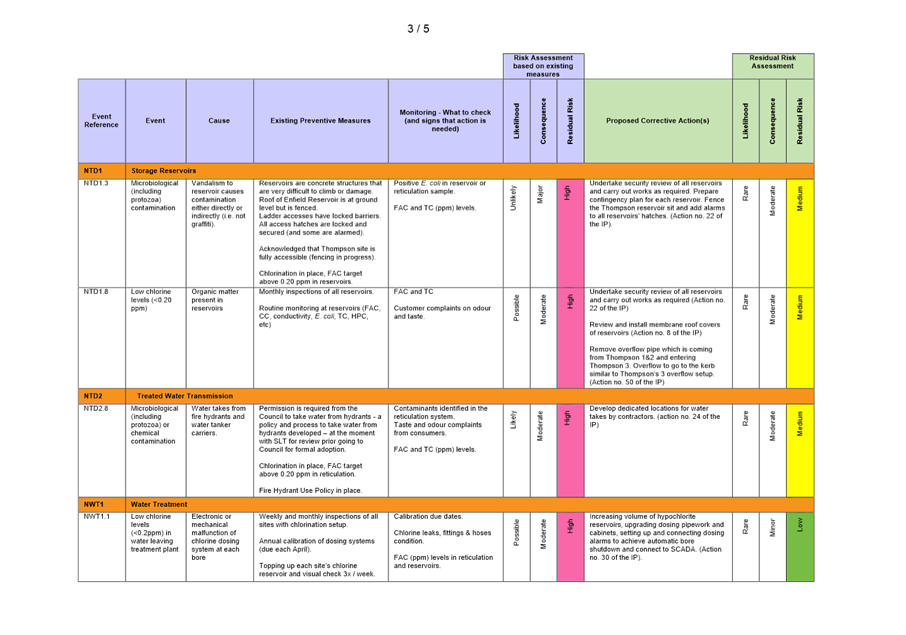

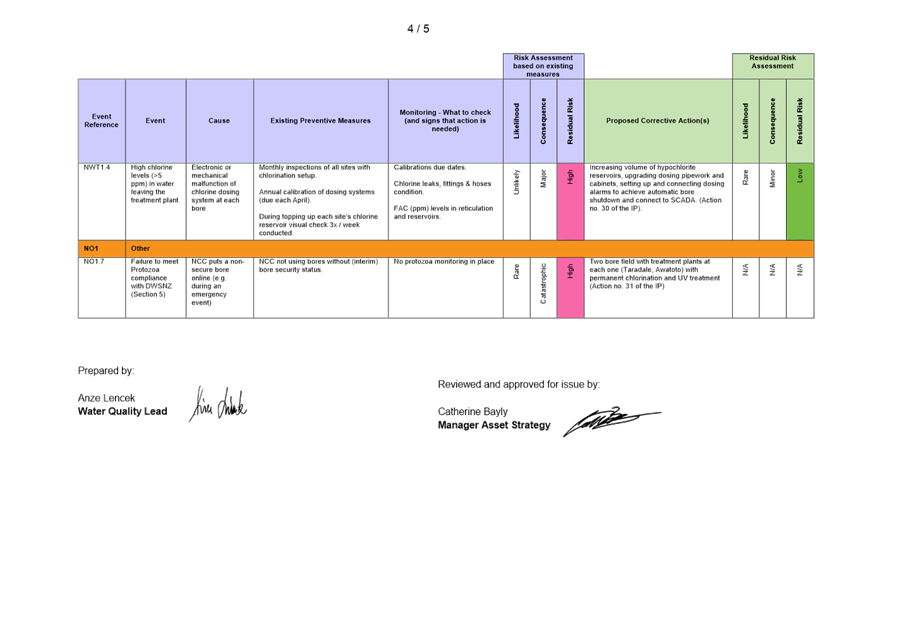

Purpose of this report is to bring ‘high’ and ‘very high’ risks as identified in NCC’s current version of Water Safety Plan (v4.3, updated August 2019) to Audit and Risk Committee attention and for Committee to acknowledge those risks.

|

The Audit and Risk Committee: a. Endorse the report. b. Note the risks identified.

|

The Havelock North Drinking Water Inquiry Stage 2 report identified six fundamental principles of drinking water safety for New Zealand. Water suppliers need to take the six principles into consideration as part of supplying safe drinking water to their customers. This Report and attached Memo relates mainly to Principle 5: Suppliers must own the safety of drinking water: Drinking water suppliers must maintain a personal sense of responsibility and dedication to providing consumers with safe water. Knowledgeable, experienced, committed and responsive personnel provide the best assurance of safe drinking water. The personnel, and drinking water supply system, must be able to respond quickly and effectively to adverse monitoring signals. This requires commitment from the highest level of the organisation and accountability by all those with responsibility for drinking water.

2.3 Issues

The risks identified within current Napier Water Safety Plan (WSP) on drinking-water supply elements, have not been reported and brought to Council’s attention to date. This issue has also been identified by our Drinking Water Assessor last September during his Implementation Visit.

2.4 Significance and Engagement

As a water supplier providing drinking-water to a large Napier and Bay View community, we have to make sure all management levels within NCC are involved and informed regularly on this essential service activity.

NCC employees have already establish good records sharing and updating processes around keeping asset and infrastructure managers, operational managers and some SLT members updated with drinking-water supply status and current affairs. This report and all next to come upon any change to the risks within WSP will also engage Council into our water supply management and provide insight on WSP risks.

‘High’ and ‘Very high’ risks are presented in the attached Memo ‘Summary of Napier Water Safety Plan’s Risks’.

2.5 Implications

Financial

N/A

Social & Policy

N/A

Risk

Risks presented in this report or its appendix are already being addressed and actions to mitigate them are in progress.

2.6 Options

The options available to Council are as follows:

a. Status Quo – do not acknowledge the outlined WSP risks presented in the appendix of this Report.

b. Acknowledge the outlined WSP risks presented in the appendix of this Report

2.7 Development of Preferred Option

N/A

a Memo ‘Summary of Napier Water Safety Plan’s Risks’, File Ref: 933753 ⇩

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |

|

Document ID: |

933568 |

|

Reporting Officer/s & Unit: |

Sue Matkin, Manager People & Capability |

3.1 Purpose of Report

The purpose of the report is to provide the Audit and Risk Committee with an overview of the health and safety performance as at 30 April 2020.

|

The Audit and Risk Committee: a. Receive the Health and Safety report as at 30 April 2020

|

The Health and Safety report as at 30 April 2020 is shown at Attachment A

a Heath and Safety Report 30 April 2020 ⇩

|

Audit and Risk Committee - 12 June 2020 - Attachments

|

Item 3 Attachments a |

|

TO: |

NCC Staff |

|

REPORT DATE: |

1 May 2020 |

|

PREPARED BY: |

Michelle Warren |

|

SUBJECT: |

Health & Safety Statistics |

|

AGENDA ITEM |

APRIL H&S REPORTING |

PURPOSE

The purpose of this report is to provide all NCC Staff, Council and Risk & Audit with an overview of the health and safety performance as at 30 April 2020.

SUMMARY – KEY PERFORMANCE INDICATORS

April LTIs = 0

|

Reported Incidents (Total Company) |

Feb 2019 |

Feb 2020 |

Mar 2019 |

Mar 2020 |

Apr 2019 |

Apr 2020 |

YTD 2019 |

YTD 2020 |

Targets FY20 |

On Target |

|

Lost time injuries (LTIs): |

1 |

0 |

0 |

3 |

1 |

0 |

5 |

6 |

<=8 |

· |

|

Medically treated injuries (MTIs): |

1 |

1 |

1 |

2 |

2 |

0 |

19 |

11 |

<=40 |

· |

|

Total recordable injuries (MTIs + LTIs): |

2 |

1 |

1 |

5 |

3 |

0 |

24 |

17 |

<=48 |

· |

|

Near miss/hit & property damage reporting |

8 |

6 |

8 |

12 |

5 |

0 |

86 |

91 |

>=180 |

· |

|

Incidents Involving Public using our facilities |

8 |

10 |

13 |

5 |

17 |

1 |

105 |

85 |

<=200 |

· |

|

Significant Incidents or Accidents involving Contractors |

1 |

1 |

0 |

0 |

1 |

0 |

5 |

5 |

<=5 |

· |

|

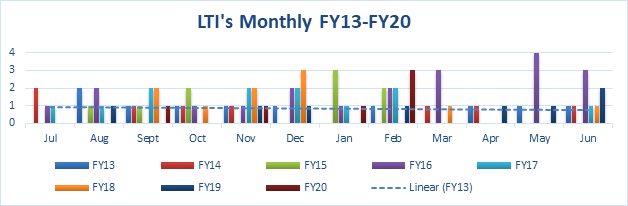

LTIs and MTIs YTD as at 30 April 2020 (Comparison between FY19 and FY20) · 20% increase in LTIs 43 days since last LTI · 42% decrease in MTIs · 29% decrease in TRIs |

|

|

Jul |

Aug |

Sept |

Oct |

Nov |

Dec |

Jan |

Feb |

Mar |

Apr |

May |

Jun |

Total |

|

FY13 |

0 |

2 |

1 |

1 |

1 |

1 |

0 |

1 |

0 |

1 |

1 |

1 |

10 |

|

FY14 |

2 |

0 |

1 |

1 |

1 |

0 |

0 |

0 |

1 |

1 |

0 |

1 |

8 |

|

FY15 |

0 |

1 |

1 |

2 |

0 |

0 |

3 |

2 |

0 |

0 |

0 |

0 |

9 |

|

FY16 |

1 |

2 |

0 |

1 |

1 |

2 |

1 |

2 |

3 |

0 |

4 |

3 |

20 |

|

FY17 |

1 |

1 |

2 |

0 |

2 |

2 |

1 |

2 |

0 |

0 |

0 |

1 |

12 |

|

FY18 |

0 |

0 |

2 |

1 |

2 |

3 |

0 |

0 |

1 |

0 |

0 |

1 |

10 |

|

FY19 |

0 |

1 |

0 |

0 |

1 |

1 |

0 |

1 |

0 |

1 |

1 |

2 |

8 |

|

FY20 |

0 |

0 |

1 |

0 |

1 |

0 |

1 |

3 |

0 |

0 |

|

|

6 |

Health and Safety Performance Lead Indicators as at 30 April 2020

|

Lead Indicators |

Detail |

Feb 20 |

Mar 20 |

Apr 20 |

YTD FY20 |

Full Year Target FY20 |

On Target |

|

|

Body discomfort reporting

(1 in 5 people) |

An early intervention programme to resolve the cause of the discomfort in the workplace and/or medical treatment before developing into chronic pain and an injury. Online e-learning videos are part of the programme. Resolutions:

|

3 |

1 |

0 |

22 |

=>50 |

· |

|

|

Work Station Assessments

(10 / 10) |

New employees receive workstation assessments and e-learning videos. Re assessments completed as required or where new areas or equipment set up. · New Employees · Existing Employees in different BU/Area/New desks or chairs

|

10 |

20

|

90 |

160

|

100% |

· |

|

|

Near miss incident reporting |

Near miss incidents reported

|

6 |

12 |

0 |

101 |

180 |

· |

|

|

Incident investigations |

All LTIs and MTIs investigations commenced within seven days of the event. · N/A |

0 |

3

|

0 |

5 |

100% |

· |

|

|

Health and Safety Meetings |

Health and safety meetings at each workplace. · Cancelled due to COVID |

2 |

2 |

0 |

20 |

30 |

· |

|

|

Internal Health and Safety Audits (1 per week) |

Health and safety audit of health and safety management system at nominated workplaces. · Cancelled due to COVID

|

7 |

2

|

0 |

20 |

48 |

· |

|

|

Contractor Health & Safety Audits and/or Safety Observations |

Contractor Audits / Safety Observations · Cancelled due to COVID

|

0 |

2 |

0 |

21 |

26 |

· |

|

|

Planned visible leadership - workplace health & safety observation &conversation

|

Workplace health and safety observations, including a conversation with staff during a workplace visit by a core management team member. Walk around chats HS safety observation 1 per quarter Attend HS mtgs e.g. toolbox 3 per year |

54

|

45

|

225 |

568

|

273

|

· |

|

|

Planned visible leadership – participating in a health and safety meeting |

SLT team member participating in a workplace or work group health and safety meeting at the workplace or joining a conference call.

|

44 |

87 |

325 |

645 |

250 |

· |

|

|

Inductions |

New Staff inducted to Napier City Council or staff who have moved business unit and re-inducted

|

9 |

8 |

4 |

96

|

100% |

· |

|

|

Safety Alerts |

Safety alerts published to educate and prevent the same or similar injury occurring again. · N/A |

0 |

0 |

0 |

0 |

6 |

· |

|

Health and Safety Other Reporting

|

Other |

Detail |

Feb 20 |

Mar 20 |

Apr 20

|

Full Year Target FY20 |

|

Significant incident |

An event in a different circumstance may result in a notifiable event (serious harm). · Public – cyclist hit barrier at cemetery · |

1 |

0 |

1 |

0 |

|

Significant Issues or Incidents Involving Contractors |

An event involving a Contractors causing significant concern. · N/A |

1

|

0 |

0 |

1 |

|

HSWA, Regulations, WorkSafe Updates and/or notifications |

Any updates communicated to management. · N/A |

0 |

0 |

0 |

N/A |

|

Return To Work in Progress |

Employees who are on a return to work programme. · MTG 1 · NAC 1

|

11 |

7 |

2 |

N/A

|

|

Training |

No Staff |

|

None due to COVID

Total trainings

(Numerous trainings postponed) |

|

Wellbeing

· Mental Health Awareness on Yammer

· Mental Health and EAP services on Yammer

· Workfit on Yammer

· Health Monitoring - Nil

· Flu Vaccines - for IMT and Essential services staff at depot 50 staff

· 90 online workplace assessments due to COVID with 7 follow ups

Updates

· COVID19

|

Audit and Risk Committee - 12 June 2020 - Attachments

|

Item 4 Attachments c |

|

Type of Report: |

Legal |

|

Legal Reference: |

Local Government Act 2002 |

|

Document ID: |

933816 |

|

Reporting Officer/s & Unit: |

Caroline Thomson, Chief Financial Officer Adele Henderson, Director Corporate Services Jane McLoughlin, Corporate Planner |

4.1 Purpose of Report

That the Committee review and provide feedback to Council on the Annual Plan 2020/21 underlying financial information prior to the final adoption of the reports.

|

The Audit and Risk Committee: a. Receive the underlying information as the basis for the Annual Plan 20/21: i. Financial information ii. 10 year revised capital plan iii. Rates remission policy iv. Rates postponement policy v. Statement of Proposal to join LGFA b. Provide feedback to Council by 9 June (via the Director of Corporate Services) to be tabled for consideration by Council at its meeting on 11 June 2020. c. Resolve that the use reserves to fund the one-off shortfall of $6.74m anticipated in 20/21 is financially prudent and does not impact unfairly on ratepayers in the future. d. Note that the Annual Plan 20/21 does not meet the section 100 (i) balanced budget provision of the Local Government Act, and that Council will be working towards a balanced budget for the LTP. e. Note that Council has notified DIA and Audit NZ that it will not meet the statutory deadline of 30 June 2020 for adoption of the Annual Plan 20/21. |

On 20 March 2020, at the Audit and Risk Committee meeting, the Annual Plan was discussed, and the Auditor directed Council to review the Annual Plan in light of Covid-19 impacts, particularly as Napier City Council receives only 51% of its total income from rates. It is a legislative requirement under the Local Government Act 2002 to have a balanced budget. The impact of Covid-19 on revenue will result in an unbalanced budget, and therefore Council must now revise its 2020/21 budget.

In the report to the Extraordinary Council meeting on 23 April, it was recommended that a new Annual Plan is developed that reflects the challenges ahead.

The average rates increase approved in the Long Term Plan 2018-28 was 5.1%.

The proposed rates increase for 2020/21 will be 4.8% average increase in rate requirement for existing ratepayers.

The approach and assumptions to guide the development of the revised Annual plan are outlined in this report.

4.3 Issues

The fast-changing events since the pandemic impacted on New Zealand, its borders, and being in lockdown has meant it has been difficult to prepare our Annual Plan for 2020/21 with any certainty. It is in effect, an emergency budget rather than a normal Annual Plan.

Council is committed to a programme and budget that supports the city to recover, but many of those details are based on several factors, including how long the Covid-19 pandemic lockdown lasts, what role Central government play in recovery, and the impact on the economy and on residents and businesses.

While it will be important to build a budget that recognises the current financial challenges that household and business face, it is also important to note that substantial support packages are available via government, banks and local government.

It is important to note that any costs that are deferred, or funded through different funding mechanisms, shift this year’s rates burden to future years and rates will be steeper in those years as a consequence.

The broad basis for setting the 2020/21 budget is finding the right balance between supporting those in need now and stimulating the local economy, while not over burdening ratepayers in the future.

Financial policy changes

Council are proposing some changes to both the Rates Remission policy and Rates Postponement policy to better define financial hardship resulting from an emergency event and to allow rates to be paid later than due dates. Consultation on the proposed changes to these policies will be undertaken separately and at the same time as the Annual Plan 20/21 consultation (refer Sections 82 to 83AA of the LGA 2002). These policies are attached as supporting information.

Statement of Proposal to join the Local Government Funding Agency (LGFA)

Council is forecasting external borrowing requirements of $33m for 20/21 (this is in line with year 3 of the LTP and assumes the capital programme will be fully completed).

Officers have explored borrowing from approved financial institutions. Several banks, whilst open to lending funds to NCC advised that the LGFA would be the better option. Approved lending institutions were contacted to establish the relative cost of borrowing. As the nature of Council borrowing may be variable and potentially short-term in nature, analysis was based on establishing a committed line of credit.

A bank commitment ensures that a line of credit is available should the borrower choose to draw. As the money is allocated to a particular borrower, it means that the funds can’t be used by the bank for another purpose. As such a commitment fee is charged. For NCC, commitment fees quoted range between 0.35% and 0.50%. On $33m the commitment fee could be up to $165,000 per annum even if no money is borrowed.

Funds could be borrowed from a bank at approximately 1.7%. For $33m, the annual interest cost would be $561,000.

To join the LGFA initial legal fees are expected to be approximately $26,000. Ongoing trustee fees are expected to be approximately $8,000 per annum. There is no membership fee or commitment fee to borrow from the LGFA.

As at the 23 April 2020, the 12 month borrowing rate (for an unrated council) was 0.91%. At $33m, the annual interest cost would be $300,300.

Comparing just the interest rate, with $33m of lending, Council would save $260,700 per annum by joining and borrowing from the LGFA. As the amount is over $20m, NCC would need to be an unrated guaranteeing local authority to borrow $33m.

Options, based on level of membership, with the LGFA were identified as follows:

|

Options – LGFA |

Additional Spend |

Impact on Rates |

Impact on Debt |

|

1) No change. Not join the LGFA. No other institutions are approached for lending. |

$0 |

Rates will need to be increased to fund revenue lost due to the pandemic. |

No debt |

|

2) Not join the LGFA. Borrowing sourced from an approved lending institution. |

Between $3,500 and $5,000 per $1m per annum to ensure facility is available. Approximately 1.7%pa for any utilised facility. |

No impact on rates |

Debt will increase by the amount borrowed (estimated at $33m total). |

|

3) Join the LGFA as a non-guaranteeing local authority. This allows NCC to borrow up to $20m through the LGFA. |

Associated legal fees. Ongoing trustee fees. |

Potential reduced rates due to savings in facility and interest rate costs. |

Debt will increase by the amount borrowed (up to $20m with LGFA and any balance sourced from an approved lending institution). |

|

4) Join the LGFA as an unrated guaranteeing local authority. This allows NCC to borrow more than $20m, but with higher risk. |

Associated legal fees. Ongoing trustee fees. |

Potential reduced rates due to savings in facility and interest rate costs. |

Debt will increase by the amount borrowed (estimated at $33m total). |

|

5) Join the LGFA as a principal shareholding local authority. This allows NCC to both borrow more than $20m and invest in LGFA shares, but with higher risk than option 4. |

Associated legal fees. Ongoing trustee fees. The cost of any shares purchased. |

Potential reduced rates due to savings in facility and interest rate costs. A modest return may be received from shares held in the LGFA. It is likely that any share purchase would be debt-funded. |

Debt will increase by the amount borrowed (estimated at $33m total) plus the cost of any shares purchased. |

Council at its meeting on 21 May 2020 approved proceeding with public consultation to join the LGFA as an unrated guaranteeing local authority (option 4 in the table above).

Consultation on the proposal to join the LGFA will be undertaken separately and at the same time as the Annual Plan 20/21 consultation (refer Sections 82 to 83AA of the LGA 2002). The Statement of Proposal to join LGFA is attached as supporting information.

4.4 Significance and Engagement

Council has assessed that there are material and significant changes from the 2018-28 Long Term Plan for the 2020/21 year and that these matters will be consulted on as per the Consultation Document (to be tabled separately due to timing of Council agenda).

The consultation and submission period for the Annual Plan 2020/21 is Thursday 18 June 2020 to noon Wednesday 15 July 2020. Submissions can be made online on the Council website. A flyer will be sent to all households outlining the process and how they can provide their feedback.

Due to Covid19, instead of community meetings, Council will host live chat sessions where the public can ask questions and give feedback before making a submission to the Annual Plan 20/21. Councillors will engage with the community via three live chat sessions on the Annual Plan 20/21.

The following table sets out the timeline for consultation and adoption of the Annual Plan 20/21:

|

Description |

Indicative Date(s) |

|

Financial content ready for Consultation Document preparation |

8 May 2020 |

|

Extraordinary Council meeting – Financial Policies |

21 May 2020 |

|

Extraordinary Council Meeting - Rates Remission Policy, Rates Postponement Policy, Consultation Document and supporting documents |

11 June 2020 |

|

Audit and Risk Committee meeting |

12 June 2020 |

|

Consultation |

18 June – 15 July 2020 |

|

Extraordinary Council meeting - Annual Plan & SCP Hearing |

12/13 August 2020 |

|

Extraordinary Council meeting - Annual Plan Adoption & Rates Setting |

27 August 2020 |

|

Issue rates notices |

10 September 2020 |

Council will not meet the statutory deadline of 30 June 2020 for adopting the Annual Plan 20/21 due to the additional time it has taken to revise budgets to reflect the impact of Covid-19. Advice provided by LGNZ, SOLGM and supported by Simpson Grierson confirms that an Annual Plan adopted after 30 June is lawful and if challenged is unlikely to be declared invalid provided the delay can be explained and the plan is not acted on until it is adopted. Audit NZ and the Department of Internal Affairs (DIA) have been advised of the late adoption date for the Annual Plan 20/21.

4.5 Implications

Financial

The original Annual Plan 20/21 proposed an increase of 6.5%, due to increases relating waste, recycling and water related projects.

Council officers assessed the financial impact from Covid19 had, including the significant reduction in income from tourism, sportsgrounds, halls, and regulatory services, the loss of income and the inability to match the offset with operating cost reductions has shown that Council will have an operating shortfall for 20/21 of $5.2m.

In addition to the operating shortfall of $5.2m Council is proposing to fund a recovery support programme of $1m and rates and rental relief packages of $543k resulting in a total funding requirement of $6.74m for 20/21.

Council has considered a number of funding options to achieve an average rates increase of 4.8%. The proposed option is to fund the gap of $6.74m from reserves ($4m from the parking reserve and $2.74m from the subdivision and urban growth fund). This option provides a pragmatic balance between managing the pressures on current ratepayers and ensuring the Council remains financially sustainable into the future, whereby the actions of today do not impact unfairly on ratepayers in the future. The borrowing proposed is for a specific purpose, in funding the one-off shortfall in operating revenue anticipated in 2020/21. While this does not meet the section 100 (i) balanced budget provision of the Local Government Act, it can be resolved that it is financially prudent due to the one off nature.

The options included in the Consultation Document are:

Option 1(proposed): reduced rates increase - $6.74m funded from reserve funds

Option 2: reduced rates increase - $6.74m funded from loans

Council also considered a zero rates increase for 20/21. However, this would require funding an additional $2.88m from either loans or reserves and would result in an increase in the following year’s rates of 5.36%. This decision would not be financially prudent and not consistent with Council’s Revenue and Financing Policy and passes a significant rates impost onto future ratepayers.

Council considered two other options, but these options were not considered appropriate to be taken further. These included:

· Continuing original Annual Plan increase of 6.5%, and funding the Covid19 impacts through the use of reserves. This was discounted as an option due to the hardship being faced by the community at this time and Council recognising that they should aim to bring the cost down as far as reasonably practicable through reducing rates in addition to the rates and recovery package.

· Recognising the full impact of Covid-19 to Council that was anticipated across the full year. This option required a 16% average rates increase, and was quickly discounted as a viable option, given the issues being faced by the community, hardship and the pressure to keep rates as low as possible at this time.

The significant reduction in revenue from the tourism activities has meant that Council will be setting an unbalanced budget for the 2020/21 year. Council has carefully considered the options of funding the operating shortfall for 20/21 and the future financial implications that will need to be managed in later years.

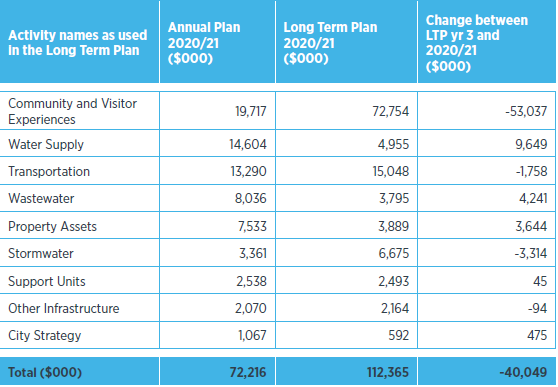

Capital expenditure

The capital plan for 20/21 includes some projects that have been brought forward, some have been re-scheduled to a later date and some have been cancelled as they are no longer required. The following table sets out the change between year 3 of the LTP and 20/21 by activity. More detail is contained in the Consultation Document (to be tabled).

The impact of any of the changes proposed in 20/21 on rates for 21/22 will be considered in the development of the 2021-31 Long Term Plan.

Social & Policy

Council are required to meet its obligations under the Local Government Act 2002, its Significance and Engagement Policy, and Revenue and Finance Policy, Liability Management, Investment Policy, Rates Postponement, Rates Remissions in relation to the preparation of the Annual Plan.

Risk

The risks to delivery of the Annual Plan are set out below:

|

Risk |

Likelihood |

Impact |

Rating |

Mitigation |

|

There is a threat is that the ability to deliver the Annual Plan is stymied due to: 1. The Capital Plan proposed for delivery is larger than council can achieve within the next 12 month period 2. Additional portfolios of work such as economic stimulus may divert resources from core delivery duties 3. Individual projects hit roadblocks or suffer unplanned delays 4. Lack of or missing regional coordination for delivery of programmes of work 5. Shortage of skilled labour or technical experts to deliver projects 6. Resources are redirected due to public health issue, judicial process, major unplanned failure, pandemic 7. Inadequate understanding or development of internal processes (risk management, governance) 8. Insufficient resources to plan and scope Capital projects due to an historical lack of investment in asset management processes, practices and support systems leading to diversion of staff into operational matters.

|

|

|

|

· Existing Project Management Reporting Software · Develop consistent project prioritisation processes (and training) for Annual Capital Plan development and programming · Increase reporting requirements to monitor Annual Plan Delivery · Moderate the proposed Annual Plan to reflect existing capability · Smooth delivery programme by identifying priority projects for delivery · Utilise carryovers to take a longer term view of short term delivery capability · Development of Council-specific policy and strategy for project, programme and portfolio management. · Develop robust risk management, project management and procurement processes and practices for consistency across the organisation. · Provide training and mentoring in risk, project management and procurement practices to improve capability across the organisation. · Invest in appropriate systems (EAM/ERP) to assist with decision making and streamline processes and free up existing staff

|

|

9. Prioritisation of capital expenditure over operational expenditure (due to rates impacts) leading to lack of investment in operational staff and operations improvements, and diversion of staff from planning activities.

Consequences: 1. The benefits of the planned investments are not realised 2. Our ability to progress towards the Council mission and community outcomes is delayed 3. Assets critical to the operation of Council’s core services are not enhanced as planned 4. Councillors lose confidence that Officers can plan and implement the Annual Plan programmed works 5. Operations and maintenance practices at minimum practice or below requirements, with associated risks. |

|

|

|

· Further develop the Capital Planning Tool to enable a more flexible programming process to enable costs and options development for community decision making and to forecast different scenarios |

|

There is a threat that the 20/21 budget is insufficient to deliver all projects identified due to: 1. The projects identified within the 20/21 Annual Plan are conservatively estimated during the development of annual plans 2. The projects identified within the 20/21 Annual Plan are poorly scoped, or not scoped. 3. Costs escalations have been ignored or not accounted for in multi-year projects 4. Market effects from the Covid-19 pandemic have a negative effect on procurement 5. Ineffective management of project phases identified in the annual plan 6. Change in Council strategic direction from elected members 7. Differing levels of robustness of cost estimates across teams. Consequences: 1. Projects are de-scoped, result in reduced quality of delivery, or progress is pushed out into future years as funds become available 2. Budgets are reallocated to deliver changes planned 3. Projects are suspended 4. The cost of the improvement outweighs the cost of the planned monetized benefits |

Likely |

Moderate |

Significant |

· Accept that cost estimates are generally required before investigations and design and therefore estimates are subject to change · Develop a consistent process for developing cost estimates that can be used across the organisation · Develop robust scopes for projects · Ensure project controls are managed during full project lifecycle so that scope, cost, schedule, and quality are monitored throughout project life cycle · Develop a consistent process for altering project budgets once more robust cost estimates have been developed · Ensure a scaled business case is completed for all projects delivered, and economic justifications are monitored appropriately accounting for the Net Present Value of each planned improvement. |

|

There is an opportunity that Central Government may fund projects that support regional economic stimulus. Consequences: 1. Council may not need to loan fund the delivery of projects funded by Central Government. 2. Key projects that would be delivered over multiple years, due to funding constraints, can be delivered more effectively. |

Likely |

Moderate |

Significant |

· Projects promoted to MBIE and the Crown Infrastructure Fund Annual Planning Processes · Re-baseline Annual Plan delivery programme once any Central Government announcements are made and elected members have considered if projects should be supported for delivery |

|

There is a threat is that the ability to procure necessary services to deliver the 20/21 Annual Plan is stymied due to: 1. Materials and plant sourced from overseas are not available due to Covid-19 pandemic restrictions 2. The construction market is saturated with new construction projects 3. Prolonged restriction periods from Covid-19 pandemic prevent projects from commencing

Consequences: 1. The benefits of the planned investments are not realised 2. Our ability to progress towards the Council mission and community outcomes is delayed 3. Assets critical to the operation of Council’s core services are not enhanced as planned 4. Inflated tender prices received from suppliers 5. Councillors lose confidence that Officers and plan and implement the Annual Plan programmed works |

Likely |

Moderate |

Significant |

· Moderation of Annual Plan Delivery NCC Procurement Improvements underway · Increase organisational procurement support by increasing resources in the procurement team · NCC Project Management Improvements underway · Existing Project Management Reporting Software · Monitor Annual Plan Programme of works via PMO to ensure engagement with industry supports meaningful and relevant works that will help appropriate sourcing opportunities for project delivery · Engage with the market to promote a pipeline of work, seek market input and package accordingly to support suppliers capabilities · Plan all procurement effectively and look at opportunities to streamline repetitive procurement tasks to add value · Smooth delivery programme by identifying bundling opportunities or more collaborative procurement opportunities |

|

There is a threat that the existing wastewater outfall pipe is damaged during the repair process due to the complexity of the repair, difficult working conditions and insufficient knowledge around the condition of the pipe in the repair locations. Consequences: 1. The outfall pipe condition deteriorates further resulting in prosecution by HBRC 2. Regulatory Enforcement by HBRC 3. Negative publicity received in local and national media 4. Perceived or actual environmental damage |

Moderate |

Major |

High |

· Work with a reputable contractor · Advance a low risk repair option that can be met within the HBRCs timeframe · Keep up communications with the regulator around progress and plans (including advancing the replacement of the outfall) · Develop an emergency response plan in the event of asset failure or additional damage · Plan for additional storage at the WWTP to enable more permanent future repairs · Attain a variation to consent to enable a small consented discharge at 700m offshore · Increase monitoring and maintenance of the outfall |

4.6 Options

a. Approve the supporting information and Consultation Document.

b. Do not approve the supporting information and Consultation Document.

c. Approve in part the supporting information and Consultation Document.

4.7 Development of Preferred Option

Approve the supporting information and Consultation Document. A robust process for budget development has been undertaken.

a Draft Annual Plan 20/21 - financial information (Under Separate Cover)

b Capital Plan for Remaining Years of 2018-28 LTP (Under Separate Cover)

c Consultation Document 20/21 - to be tabled ⇩

d Rates Remission policy (Under Separate Cover)

Audit and Risk Committee - 12 June 2020 - Open Agenda Item 5

5. Sensitive Expenditure - Mayor and Chief Executive

|

Type of Report: |

Procedural |

|

Legal Reference: |

N/A |

|

Document ID: |

933218 |

|

Reporting Officer/s & Unit: |

Caroline Thomson, Chief Financial Officer |

5.1 Purpose of Report

To provide the information required for the Committee to review Sensitive Expenditure of the Mayor and Chief Executive for compliance with Council’s Sensitive Expenditure Policy.

|

The Audit and Risk Committee: a. Receive the report of Sensitive Expenditure for the Mayor and Chief Executive and review for compliance with the Sensitive Expenditure Policy.

|

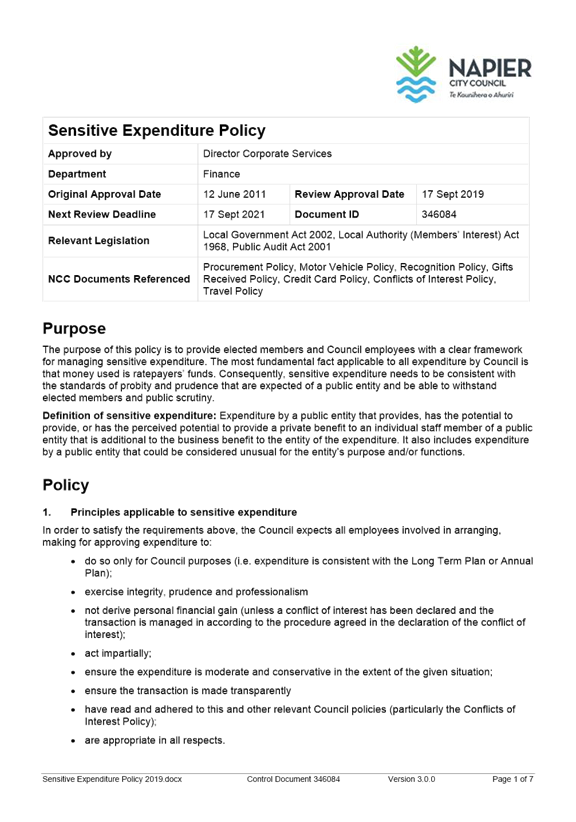

The Sensitive Expenditure Policy approved by the Senior Leadership Team on 17 September 2019 requires a report of all sensitive expenditure by the Chief Executive and by the Mayor to Audit and Risk Committee meetings (clauses 6.3 and 6.4). The policy also states that the expenditure items will be reviewed by the Chairperson or the Deputy Chairperson of the Audit and Risk Committee for compliance with this policy.

5.3 Issues

No issues.

5.4 Significance and Engagement

N/A

5.5 Implications

Financial

N/A

Social & Policy

N/A

Risk

N/A

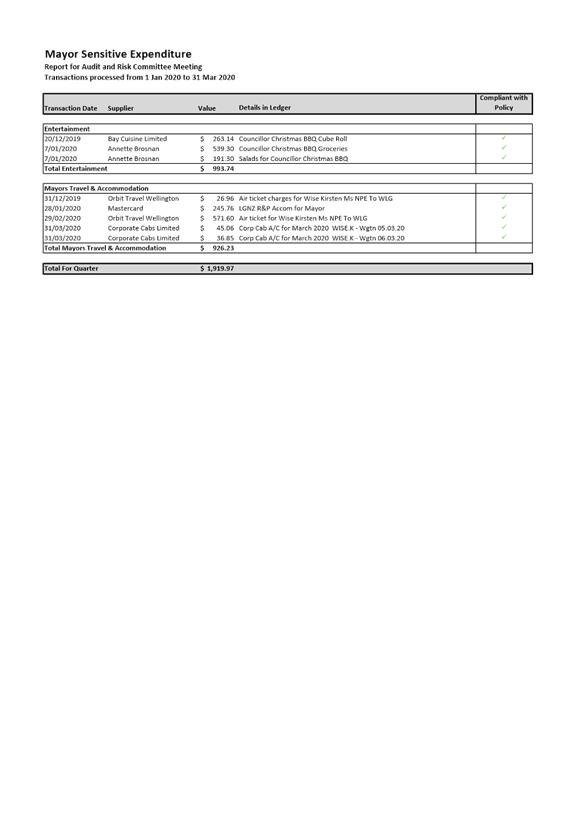

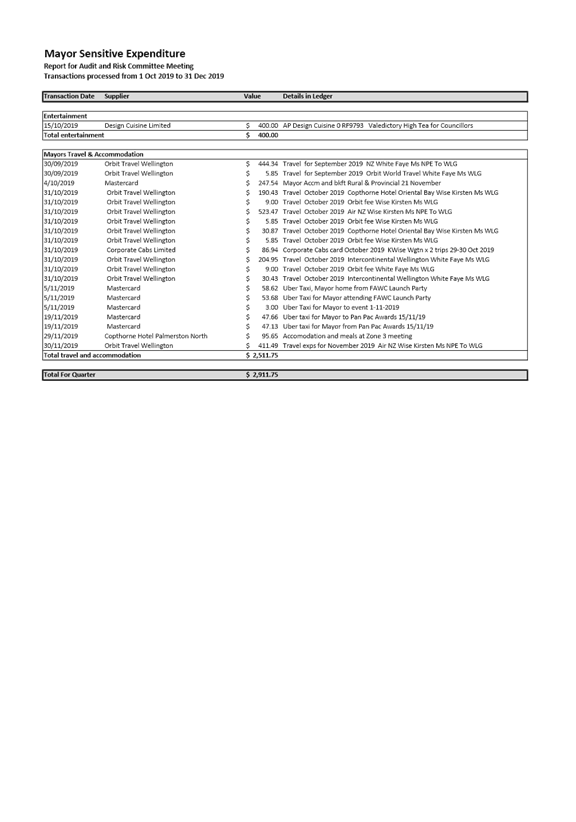

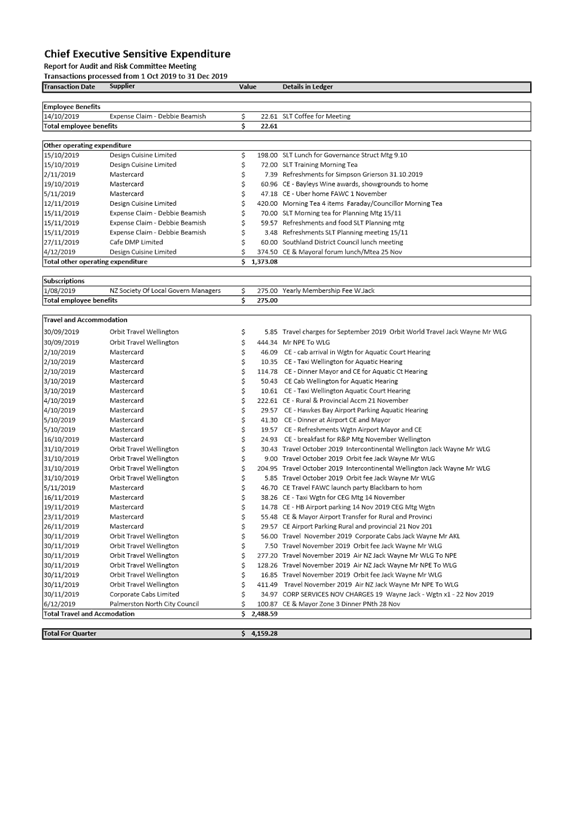

a Mayor Sensitive Expenditure Report Q3 ⇩

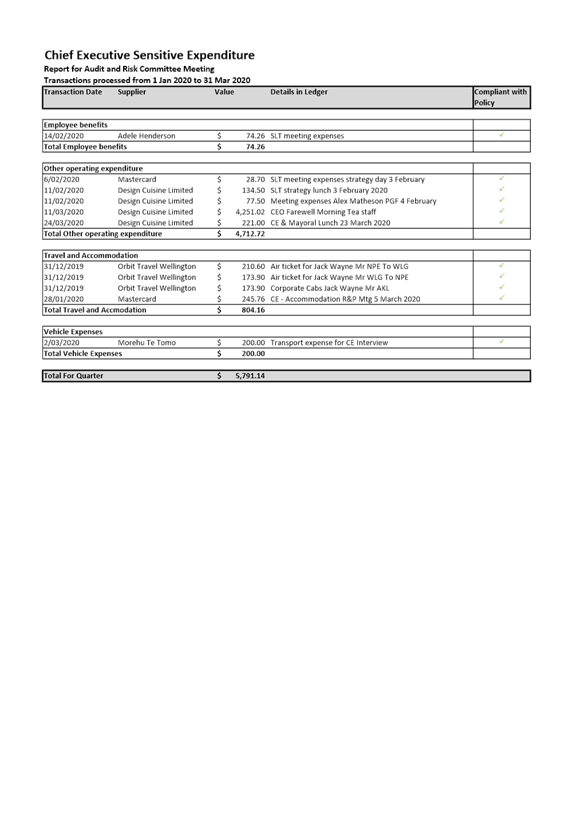

b CE Sensitive Expenditure Report Q3 ⇩

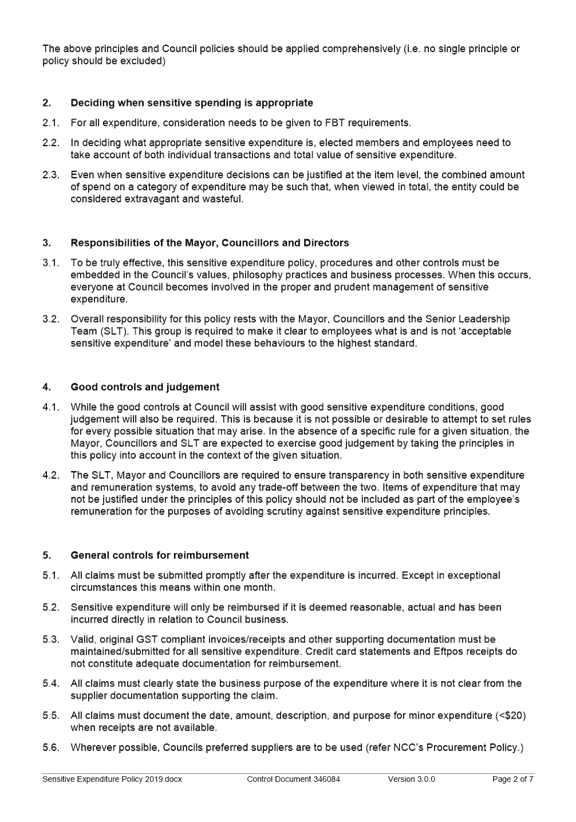

c Sensitive Expenditure Policy ⇩

d Mayor Report Sensitive Expenditure Q2 ⇩

6. External Accountability - Investment and Debt Report

|

Type of Report: |

Information |

|

Legal Reference: |

N/A |

|

Document ID: |

933511 |

|

Reporting Officer/s & Unit: |

Caroline Thomson, Chief Financial Officer |

6.1 Purpose of Report

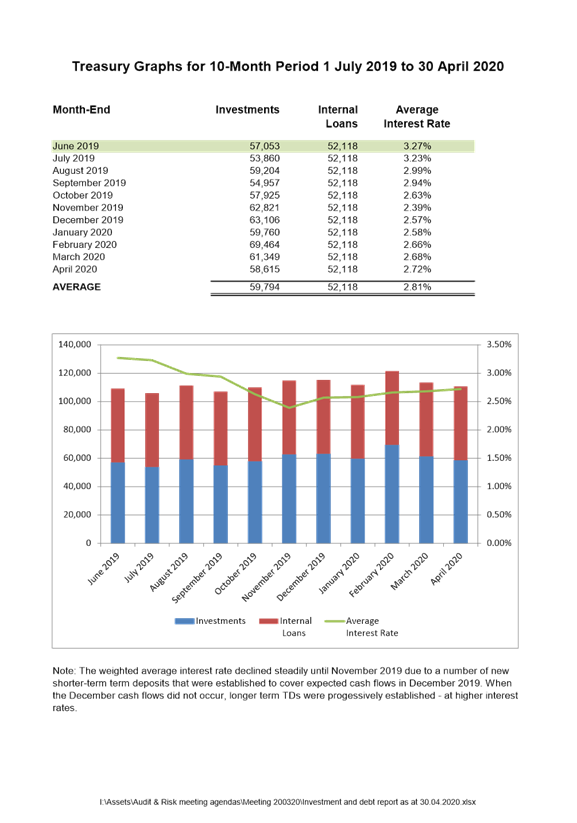

To consider the snapshot report on Napier City Council’s Investment and Debt as at 30 April 2020.

|

The Audit and Risk Committee: a. Receive the snapshot report on Napier City Council’s Investment and Debt as at 30 April 2020.

|

The snapshot report on Napier City Council’s Investment and Debt as at 30 April 2020 is shown at Attachment A.

a Investment and Debt Report as at 30 April 2020 ⇩

Audit and Risk Committee - 12 June 2020 - Open Agenda Item 7

7. Risk Management Report

June 2020

|

Type of Report: |

Information |

|

Legal Reference: |

N/A |

|

Document ID: |

934363 |

|

Reporting Officer/s & Unit: |

Adele Henderson, Director Corporate Services |

7.1 Purpose of Report

To provide the Audit and Risk Committee with an update on progress with risk management work and to report on the highest paid risks.

|

The Audit and Risk Committee: a. Note the Risk Management Work being undertaken by Napier City Council staff and management. b. Note the current High risks. c. Receive the Risk Report dated 29th May 2020

|

Napier City Council (NCC) has a programme of work to develop and mature its enterprise risk capability. A risk maturity roadmap has been developed to guide this work.

The Committee supports this work by acting in a monitoring and advisory role. This report provides an update to the Committee on progress against the roadmap and reports the highest rated risks to ensure they are being actively managed.

NCC has a Risk Management Framework document together with a Risk Management Strategy. These document set out the NCC risk appetite and the risk management roles, responsibilities and reporting requirements. The Risk Management Framework is due for review and will be bought back to this committee at the next meeting.

NCC risks are recorded in a risk management software solution known as “Sycle”. Each risk is assigned a risk owner and the risk is rated based on an assessment against the NCC risk matrix and based on the level of residual risk once any control measures and actions (or work programmes) designed to prevent or mitigate the risk have been identified and implemented.

NCC has an internal Risk Committee made up of officers from different areas of the organisation. The role of the risk committee is to coordinate the risk management process; monitor the risk profile, risk appetite and effectiveness of controls; monitor & review high and extreme risks and report extreme and high risks to Council’s senior leadership team. The committee is chaired by the Manager Business Excellence & Transformation.

The Risk Management Strategy requires high and extreme risks to be reported to the Audit & Risk Committee. Recognising the level or NCC risk maturity all high\extreme strategic risks and extreme operational risks are reported to each Audit & Risk Committee meeting.

7.3 Issues

The following are specific items on the work programme:-

· Development of the Sycle Projects module

· Continuation of a Business Continuity Management programme of work

· Review risk processes, systems and of the risk register

Sycle Projects Module

Work continues to progress on the implementation of the projects module in Sycle.

Business Continuity Management

A Pandemic Policy was written along with working guidelines for staff as part of the Pandemic.

Risk Management at NCC

A placement has been made anddd will start in the role of Risk and Assurance Lead on 22 June.

7.4 Significance and Engagement

There are no external consultation requirements for this report.

7.5 Implications

Risk Register

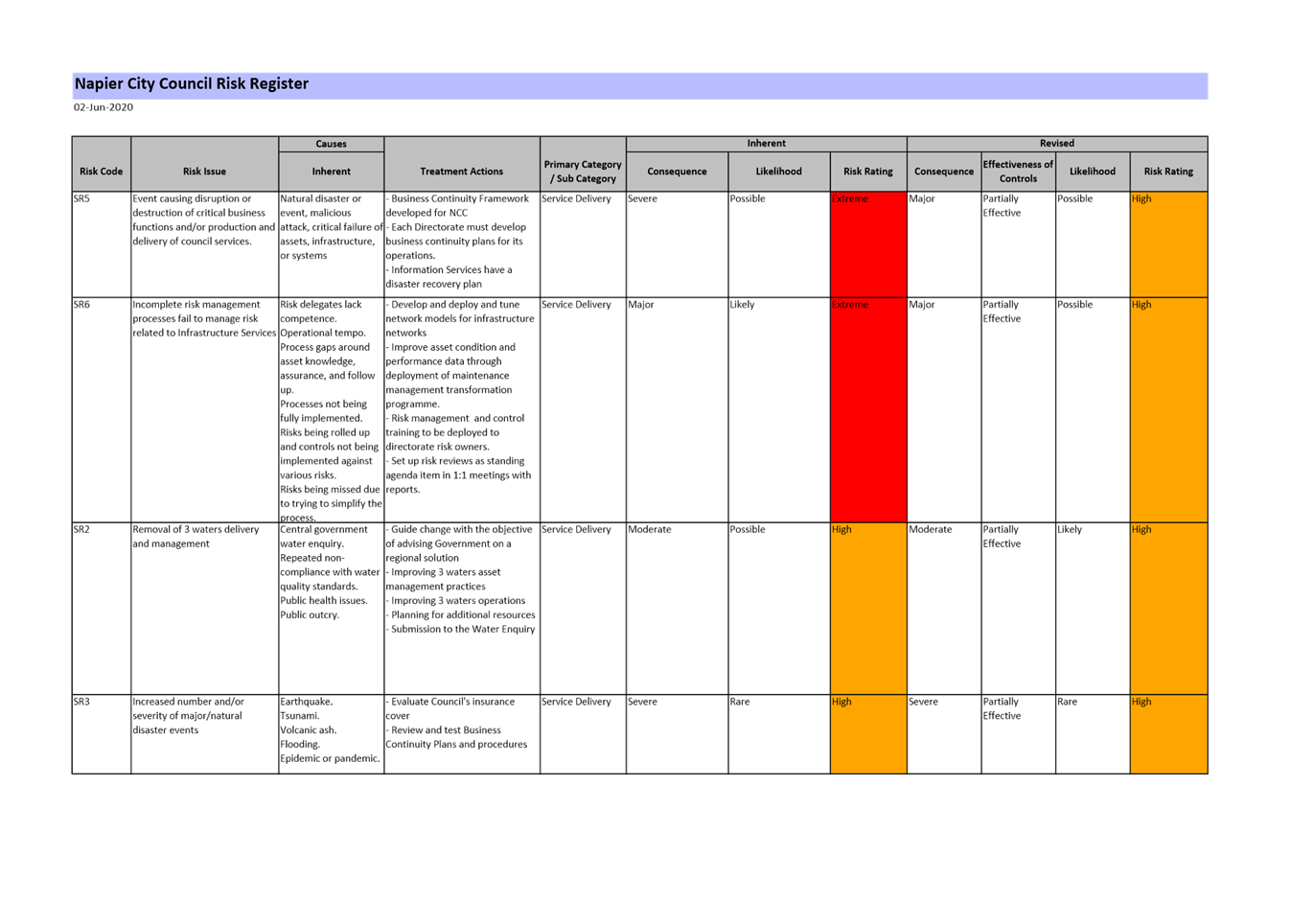

There are currently 4 strategic and 149 operational risks in the risk register. (Project risks have been excluded from reporting). Two new operational risks have been added to the registers since the last meeting of the Committee.

There are four risks to report to the Committee as the highest rated risks;

High (SR2, SR3, SR5 and SR6).

These risks are reported in the attached spreadsheet. (Attachment A).

All five risks have treatment actions to further manage the causes or consequences of each risk.

High Risks

The four high risks in the strategic register are:

· SR2 Removal of three waters delivery and management

· SR3 Increased number and/or severity of major/natural disaster events

· SR 6 Risk management practices

· SR5 Event causing disruption or destruction of critical business functions and/or production and delivery of council services. – we were very pleased with Councils ability to respond the impacts of Covid19 (pandemic) which has the potential to impact Councils ability to deliver services including online.

These risks were previously reported to you at the last meeting and they have not changed. The risks are outside the control of NCC. The risks treatments listed against these risks are ongoing.

Other Topical Current, New and Emerging Risks

In addition to the risks reported as a matter of course we have identified some current topical risks of relevance to the organisation. These all impact on the organisation’s ability to deliver high quality services to the community. These include:-

Covid19 and Impacts:

· Establishment of the Incident Management Team in Napier as part of its Emergency Management Response

· Group Emergency Management Response

· Pandemic Plan implementation

· Remote desktop capacity increased to provide for staff to work from home

· Review of stock of protective gear for Council staff

· Impact from Covic19 across Council business (particularly Tourism) – currently forecasting an unplanned rating loss of $3m

· Managing Council operations with increased level of cleaning and contact tracing

· Increasing need to provide cybersecurity for staff working from home

· Council services such as Chlorine Free taps – and appropriate time to open

· Park closure and opening management

· Transfer station operations in a Covid19 environment

· Impacts on the Long Term Plan from a decrease in Tourism

Other topical Risks:

· Legal action such as the leaky building claims. These are impacting on both the management resource (time that is not spent delivering other projects etc.) and the Councils finances (cost).

· Provincial Growth Fund/CIPs funding requests may not be successful

· Drinking Water – OR26 “Contamination of Water Supply resulting in death and or widespread illness”

o OR26 has an inherent risk rating of extreme with a revised (current) risk rating of high as a result of many actions and controls that all go into the make up of the Water Safety Plan (WSP). The only fully effective control is chlorination of source water resulting in the provision of residual disinfection throughout the network. All other actions and controls do not reduce the extreme risk rating.

7.6 Options

N/A

7.7 Development of Preferred Option

N/A

a Schedule of Strategic High and Extreme Risks as at 2 June 2020 ⇩

Audit and Risk Committee - 12 June 2020 - Open Agenda

That the public be excluded from the following parts of the proceedings of this meeting, namely:

AGENDA ITEMS

1. Insurance Update

2. Cybersecurity Strategy

3. Revera Lead Agency IaaS Close Out Report

4. Legal Update

The general subject of each matter to be considered while the public was excluded, the reasons for passing this resolution in relation to each matter, and the specific grounds under Section 48(1) of the Local Government Official Information and Meetings Act 1987 for the passing of this resolution were as follows:

|

General subject of each matter to be considered.

|

Reason for passing this resolution in relation to each matter.

|

Ground(s) under section 48(1) to the passing of this resolution.

|

|

1. Insurance Update |

7(2)(i) Enable the local authority to carry on, without prejudice or disadvantage, negotiations (including commercial and industrial negotiations) |

48(1)A That

the public conduct of the whole or the relevant part of the proceedings of

the meeting would be likely to result in the disclosure of information for

which good reason for withholding would exist: |

|

2. Cybersecurity Strategy |

7(2)(h) Enable the local authority to carry out, without prejudice or disadvantage, commercial activities |

48(1)A That

the public conduct of the whole or the relevant part of the proceedings of

the meeting would be likely to result in the disclosure of information for

which good reason for withholding would exist: |

|

3. Revera Lead Agency IaaS Close Out Report |

7(2)(h) Enable the local authority to carry out, without prejudice or disadvantage, commercial activities |

48(1)A That

the public conduct of the whole or the relevant part of the proceedings of

the meeting would be likely to result in the disclosure of information for

which good reason for withholding would exist: |

|

4. Legal Update |

7(2)(b)(ii) Protect information where the making available of the information would be likely unreasonably to prejudice the commercial position of the person who supplied or who is the subject of the information 7(2)(g) Maintain legal professional privilege 7(2)(i) Enable the local authority to carry on, without prejudice or disadvantage, negotiations (including commercial and industrial negotiations) |

48(1)A That

the public conduct of the whole or the relevant part of the proceedings of

the meeting would be likely to result in the disclosure of information for

which good reason for withholding would exist: |

Audit and Risk Committee - 12 June 2020 - Open Agenda

Audit and Risk Committee

Open Minutes

|

Meeting Date: |

Friday 20 March 2020 |

|

Time: |

1.02pm-2.09pm |

|

Venue |

Council Chamber |

|

Present |

John Palairet (In the Chair), Mayor Kirsten Wise, Councillor Nigel Simpson and Councillor Graeme Taylor

|

|

In Attendance |

Acting Chief Executive, Director Corporate Services, Director Community Services, Manager People and Capability, Manager Communications and Marketing, Chief Financial Officer, Accounting Manager Karen Young – Audit New Zealand |

|

Administration |

Governance Team |

Apologies

|

J Palairet / Councillor Simpson That the apology from David Pearson be accepted. Carried |

Conflicts of interest

Nil

Public forum

Nil

Announcements by the Mayor

The Mayor thanked everyone for making themselves available for the meeting, considering the changing situation in relation to Covid-19.

Announcements by the Chairperson

Nil

Announcements by the management

Nil

Confirmation of minutes

|

Councillors Simpson / Taylor That the Minutes of the meeting held on 5 December 2019 were taken as a true and accurate record of the meeting.

Carried |

Agenda Items

1. Audit and Risk Charter Review

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |

|

Document ID: |

898773 |

|

Reporting Officer/s & Unit: |

Caroline Thomson, Chief Financial Officer |

1.1 Purpose of Report

As set out in the Audit and Risk Committee Charter, the Committee will review this Charter in consultation with the Council at least once a year. Any substantive changes to the Charter will be recommended by the Committee, and formally approved by the Council. The last review of the Charter was undertaken July 2018.

|

At the Meeting The Chief Financial Officer spoke to the report, noting that the Committee’s responsibilities are now included in the Risk Charter, as previously requested. It was also noted that the Standing Committee names have now been updated. |

|

Committee's recommendation Mayor Wise / Councillor Taylor The Audit and Risk Committee: a. Review the Audit and Risk Committee Charter b. Provide any recommended changes for Council approval Carried |

2. Health and Safety Report

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |

|

Document ID: |

908475 |

|

Reporting Officer/s & Unit: |

Sue Matkin, Manager People & Capability |

2.1 Purpose of Report

The purpose of the report is to provide the Audit and Risk Committee with an overview of the health and safety performance as at 31 January 2020.

|

At the Meeting The Manager People and Capability provided a brief overview of the Health and Safety report for the period to 31 January 2002. In response to questions from members, it was noted that officers have attempted to bring the staff flu vaccine date forward; however, this has not been possible. It was noted that Council does not prioritise the flu vaccine by age. A notification has been sent to all staff asking them to register their interest in receiving the flu vaccine. At the time of the meeting, numbers had not been confirmed and officers advised they would have a better indication of how many staff will be taking up the offer in a week or so. Committee members felt strongly that all staff should be encouraged to have the vaccine. |

|

Committee's recommendation Councillors Simpson / Taylor The Audit and Risk Committee: a. Receive the Health and Safety report as at 31 January 2020

Carried |

3. Insurance arrangements

|

Type of Report: |

Operational |

|

Legal Reference: |

N/A |