Extraordinary Meeting of Council

Open Agenda

|

Meeting Date:

|

Tuesday 9 February 2021

|

|

Time:

|

11.00am (Revenue & Finance Policy

Hearing)

|

|

Venue:

|

Large Exhibition Hall

Napier War Memorial Centre

Marine Parade

Napier

|

|

Council Members

|

Mayor Wise, Deputy Mayor Brosnan, Councillors Boag,

Browne, Chrystal, Crown, Mawson, McGrath, Price, Simpson, Tapine, Taylor,

Wright

|

|

Officer Responsible

|

Chief Executive

|

|

Administrator

|

Governance Advisor

|

|

|

Next Council Meeting

Thursday 11 March 2021

|

Extraordinary

Meeting of Council - 09 February 2021 - Open Agenda

ORDER OF BUSINESS

Apologies

Nil

Conflicts of interest

Public forum

Announcements by the Mayor including notification of minor

matters not on the agenda

Note: re minor matters only - refer LGOIMA s46A(7A) and

Standing Orders s9.13

A meeting may discuss

an item that is not on the agenda only if it is a minor matter relating to the

general business of the meeting and the Chairperson explains at the beginning

of the public part of the meeting that the item will be discussed. However, the

meeting may not make a resolution, decision or recommendation about the item,

except to refer it to a subsequent meeting for further discussion.

Announcements by

the management

Agenda items

1 Submissions

on the Statement of Proposal for the Revenue & Financing Policy, Rating

Policy, Rates Remisssion Policy & Rates Postponement Policy Document.......................................... 3

Extraordinary

Meeting of Council - 09 February 2021 - Open Agenda Item

1

Agenda Items

1. Submissions

on the Statement of Proposal for the Revenue & Financing Policy, Rating

Policy, Rates Remisssion Policy & Rates Postponement Policy Document

|

Type of Report:

|

Legal

|

|

Legal Reference:

|

Local Government Act 2002

|

|

Document ID:

|

1281821

|

|

Reporting Officer/s & Unit:

|

Garry Hrustinsky, Investment and Funding Manager

Emma Morgan, Team Leader Community Strategies

|

1.1 Purpose

of Report

To present the submissions received

on the Revenue & Financing Policy, Rating Policy, Rates Remission Policy

and Rates Postponement Policy Statement of Proposal for Council’s

consideration.

To present final recommendations to

Council following public submissions on the Statement of Proposal.

|

Officer’s Recommendation

That

Council:

a. Adopt the following officer recommendations, including any changes

and/or additional recommendations arising from the deliberations and

consideration of all submissions to the Statement of Proposal for the Revenue

& Financing Policy, Rating Policy, Rates Remission Policy and Rates

Postponement Policy.

Revenue & Financing Policy

i. Based

on community feedback, that Council reduce the rating categories for General

Rates from 6 down to 4 (compared to the original proposal of 3), creating a

Residential/Other, Commercial & Industrial, Semi-Rural and Rural

category.

ii. That

Council adopt the method of funding for all 36 Council activities as

proposed.

iii. That

Council adopt the Revenue & Financing Policy in this amended form.

Rating Policy

iv. That Council

introduce a Rating Policy.

v. Noting

item a, i (above), the following weights for General Rates be

applied:

· Residential/Other 100%

· Commercial & Industrial 250%

· Semi-Rural 92.5%

· Rural 85%

vi. That Council

increase the City Water Rate from 50% to 70% for Rating Units that are not

connected but within 100m of the system.

vii. That Council

increase the Sewerage Rate from 50% to 70% for Rating Units that are not

connected but within 30m of the system.

viii. That Council

continue to investigate the feasibility of a Wastewater Rate (pan charge) to

replace the current Sewerage Targeted Rate.

ix. That Council

introduce a targeted Stormwater Rate.

Rates Remission Policy

x. That

Council introduce a Remission for Farmland Under 5 Hectares.

xi. That Council

introduce a Remission of Refuse Collection and/or Kerbside Recycling Targeted

Rates.

xii. That Council

introduce a Remission for Residential Properties Used Solely as a Single

Residence.

xiii. That Council

remove the Remission for Land Subject to Special Preservation Conditions.

xiv. That Council remove

the Remission of Uniform Annual General Charges (UAGC) and Targeted Rates of

a Fixed Amount on Rating Units Owned by the Same Owner.

xv. That Council

approves the updated wording in Remission for Residential Land in Commercial

or Industrial Areas to bring it in line with changes to the Rating Valuation

Act 1998.

xvi. That Council

defines “a significant increase” to be 25% or more over the

current assessed rates for a single property.” for remissions to smooth

the effects of change in rates on individual or groups of properties

xvii. That Council adopt the

Rates Remission Policy as proposed.

Rates Postponement Policy

xviii. That Council remove the

Postponement for Farmland

xix. That Council adopt

the Rates Postponement Policy as proposed.

b. Direct

Officers to advise the submitters of Council’s decision in relation to

their submission.

|

|

|

1.2 Background

Summary

A Revenue and Financing Policy

must be adopted prior to the adoption of a Long term Plan, which must be

adopted every three years. Therefore, a local authority must review its

Revenue and Financing Policy at least every three years. These reviews

are either a first principles or a review to confirm the policy’s relevance

and appropriateness. The previous Council commenced a first principles

review having concluded that the then policy was no longer appropriate due to

the changes within the City since its last full review.

Work on the Revenue and Financing

Policy also impacts the rating function, and resulted in a review/consideration

of a Rating Policy, the Rates Remission Policy and Rates Postponement Policy.

As a full review had not occurred for many years, the Revenue & Financing

Policy did not properly reflect the Napier and Council as it stands today.

A series of 9 Council workshops

were conducted to review Council services on a first principles approach

assessing a number of factors (detailed in the Revenue & Financing Policy)

and how those services should be funded. The rating framework and possible

alternative approaches were discussed and analysed during these workshops.

Due to the pandemic, the process

was delayed as emergency measures were put in place by Council.

At a meeting of Council on 15

September 2020, a draft Revenue & Financing Policy, Rating Policy, Rates

Remission Policy and Rates Postponement Policy were approved for consultation.

These documents were adopted to proceed as part of a Statement of Proposal,

along with a Consultation Plan, for public consultation at a meeting of Council

on 8 October 2020.

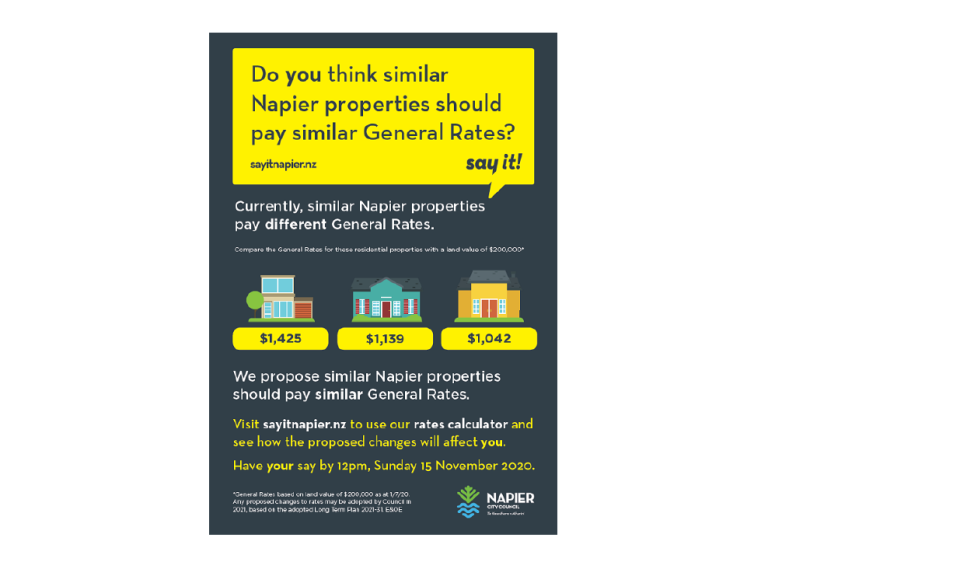

Public consultation commenced on

12 October and was extended out to 2 December. Media ads (print, social media,

radio and online) were placed, two rounds of letters, 6 public meetings and

promotion on the Council website were conducted to ensure high public awareness

and engagement. Hardcopy and softcopy versions of the proposal, summary and

submission forms were made available to the public and for anybody wishing to

provide feedback on the proposal.

The submission document was split

into four sections reflecting the four policies being consulted on. A total of

18 questions were posed over the submission with space for further comment. The

document also contained an option for people to check if they wished to present

their submission at the public hearing commencing 9 February 2021. 64 people

initially elected to speak.

Council is required to consider

all submissions to the proposal, respond to submissions, and provide

recommended changes to the proposal based on feedback.

To ensure that decision-makers

are well informed regarding feedback, the following approach has been used:

1. Council

officers and delegates have read and considered each response, and have written

a management response.

2. Summarised

the issues to ensure that decision-makers understand community views.

3. Individual

submissions have been put into a separate attachment (please refer to Attachments

A (section 15, Appendix) & B) so that decision-makers can read

through the collection of submissions.

4. For

each consultation topic (question), this report has the following sections:

- Summary of feedback – including statistics

of responses to closed questions, and responses to open-ended questions which

have been put into key themes.

- Officers’ information and comment – Officers’

consideration of feedback and any comments.

- Officers’ recommendation – outlines

whether the Officers’ recommendation remains the same or is different

from that proposed in the consultation document.

Overview of engagement and

community feedback

Letters were sent to all

negatively affected properties advising of the consultation, the proposed

impact on the rates, and community meeting dates. Following the decision to

extend the consultation, a letter was sent to all ratepayers.

Six community meetings were held

with a total of 298 attendees:

· Monday 19

October 2020 – Napier War Memorial Centre, 5:30pm – 15

attendees

· Tuesday 20

October 2020 – Napier War Memorial Centre, 11am – 22

attendees

· Tuesday 20

October 2020 – King George’s Hall (Bay View), 6pm –

108 attendees

· Wednesday 21

October 2020 – Taradale Town Hall, 6pm – 100 attendees

· Wednesday 18

November 2020 – McLean Park, 11am – 18 attendees

· Wednesday 18

November 2020 – McLean Park, 6pm – 35 attendees

Regarding digital advertising, 442,197 impressions served for this campaign which is the

number of times the digital advertising was displayed to Napier residents. This

generated 2,457 clicks through to the consultation web page. The average cost

per click was $0.52 and there was a click

through rate of 0.56%, which is average.

There were four advertisements

across Facebook and Instagram, reaching 22,889 residents and generating 782

clicks through to the consultation web page.

Along with the four

advertisements, the consultation was organically posted eight times, reaching

47,874 residents and generating 2,924 engagements; this includes reactions,

comments and clicks.

Traffic to the sayitnapier.nz

consultation website saw five significant spikes throughout the campaign. These

cannot be directly linked to any specific community session or social media

posts. There were a number of closed community groups sharing NCC content with

their members, specifically those negatively affected by the proposed change,

which could have resulted in spikes of traffic. The consultation received

11,493 page views.

Further details on consultation

can be found in the report – Revenue and Financing Statement of Proposal

Consultation Summary (Attachment C).

Overall, 540 submissions were

received. 474 submissions were submitted online and 66 were provided in

hardcopy form. Some duplicate submissions were received (same person or

address) which were aggregated into a single submission per household; this

results in a total 427 unique responses per rating unit. 64 submitters

requested to support their submission in person (oral submission) at the

Hearings. Final numbers were yet to be confirmed for the Hearings at the time

this report was written.

Other observations include:

· Around half

(52.6%) of participating ratepayers disagreed with proposed changes to fund

Council’s activities; 1-in-10 (10.6%) agreed, and a further 36.9% agreed

‘to some extent’.

· Those who

agreed ‘to some extent’ typically opposed reduction of rating

categories from 6 to 3 (61.7%). In terms of the proposed way to fund Council

activities (e.g. proportion of rates vs. user pays), one-quarter (23.4%)

agreed, 39.8% remained neutral, and 36.7% disagreed.

· The majority

of ratepayers (66.2%) disagreed with proposed changes to how General and

Targeted rates are assessed; 1-in-10 (11.7%) agreed, 22.1% agreed ‘to

some extent’.

· Half (50.0%)

of those who agreed ‘to some extent’ were opposed to General rate

percentage weights for Residential/other, Commercial/industrial, and Rural

properties.

· A more even

distribution of ‘Yes’ (28.1%), ‘No’ (35.8%) and

‘To some extent’ (36.1%) responses were recorded. Of those who

agreed ‘to some extent’, a greater percentage supported Remission

of Refuse Collection and/or Kerbside Recycling Targeted rates (55.8%) and

phased increases over time (44.4%).

· The majority

of ratepayers were ‘Neutral’ (55.2%) about the proposed removal of

amendments to the Rates Postponement Policy; similar proportions agreed (22.0%)

or disagreed (22.8%).

· In general,

ratepayers from Bay View, Awatoto, Eskdale and Jervoistown were more likely to

oppose changes to most policies.

· A large

volume of additional verbatim feedback was collected. Consistent with other

results, ratepayers’ specific responses generally opposed policy changes.

The main issues or themes highlighted included:

o Proposed rates increases

are high given fewer (or unchanged) infrastructure / amenities / services

received (67%) – respondents identified services such as sewerage,

stormwater, street lighting, kerbing, road/footpath development as services

they do not receive, perceiving their rates increases as poor value in this

context.

o Changes unfair for rural

/ semi-rural residents (48%) – in general, proposed changes were

considered unfair for rural/semi-rural residents, with a perception that their

properties were not similar to more urban properties in terms of value received

for rates charged, property rights (for land use, subdivision, etc.) permitted

(13%), or a perception that changes represented a ‘wealth tax’

(7%).

o Rural / semi-rural

residents already incur additional infrastructure/service costs (33%) –

related to the first point, residents felt increased rates/charges were unfair

given the increased costs they already incur (relative to urban properties) to

provide their own infrastructure and services not currently provided by the

Council.

o Proposed rates increases

are high given current economic situations / pressures (23%) – proposed

increases were considered poor timing given existing economic conditions (e.g.

in light of COVID- 19 pandemic), or for those on low/fixed incomes. Some ratepayers

(4%) called for increases to be phased in as a result.

· The greatest

number of submissions came from those areas most negatively impacted by the

proposed changes with the top four being Bay View (32%), followed by Poraiti

(14%), Meanee (10%) and Jervoistown (7%)

Please refer to Attachment A

for detailed analysis of the results.

Survey Responses

As noted above, the submission

document was split into four sections reflecting the four policies being

consulted on. A total of 18 questions were posed over the submission with space

for further comment. Submission results, responses and recommendations are as

follows:

Revenue and Financing

Policy

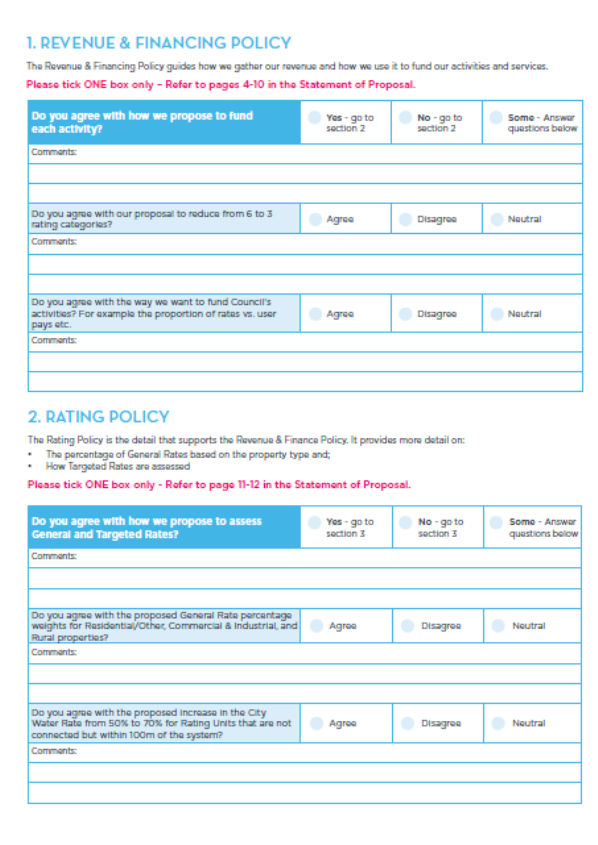

Q.1 – Do you agree with

how we propose to fund each activity?

|

Yes

|

10.6%

|

No

|

52.6%

|

To some extent

|

36.9%

|

|

Total Unique Responses

|

388

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

1

|

Rates should not increase as rural

services have decreased.

|

|

1

|

The General Rate should cover all common

good services. Water, sewerage, etc should be a Targeted Rate.

|

|

2

|

Rural properties have fewer services and

are not the same as urban properties. Rural property owners shouldn’t

pay as much.

|

|

1

|

Rural properties have additional costs in

providing their own infrastructure (e.g. sewerage).

|

Officers’ information

and comment

Targeted Rates are only applied

to specific services that properties receive (such as water or sewerage). Rural

properties that do not receive these services do not pay for these services.

General Rates pay for public good

services and facilities across the wider city (e.g. public toilets and the

roading network). It does not matter where the property is or where the service

is, as all properties contribute to these services. General Rates are not

charged based on what is immediately outside the gate of a property.

General Rates recover the costs

for services and facilities that in the Council’s view, the whole

community benefits (e.g. public toilets and the roading network). Therefore,

General rates (including the Uniform Annual General Charge) are considered a

tax. Legalisation[1]

requires that the General rate is recovered by a value based rate, either land

or capital. This is supported by case law[2].

Officers’

recommendation

It is recommended that Council

adopt the proposed activity funding model detailed in the draft Revenue &

Financing Policy.

Q.2 – Do you agree with

our proposal to reduce from 6 to 3 rating categories?

|

Agree

|

14.3%

|

Disagree

|

61.7%

|

Neutral

|

24.1%

|

|

Total Unique Responses

|

133

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

24

|

3 categories is too simplistic. Access to

certain services (e.g. street lighting and bus network) is not equal for all

areas. Residential properties in different areas are not the same.

|

|

9

|

The number of differentials should be

increased (and/or definitions broadened) to make it fairer: stop rural areas

being disadvantaged, include a split between Commercial and Industrial,

increase the number of Residential categories).

|

|

3

|

Condense into 3 differentials but

increase the number of sub-differentials to cover properties that don’t

quite fit into those 3.

|

|

1

|

Bay View and ex-county rural are

redundant.

|

|

2

|

Moving certain areas into 3 differentials

will create hardships for those residents.

|

|

2

|

Staging an increase in rates would help

buffer the shock.

|

|

4

|

Rural properties pay a number expenses

that urban properties don’t need to such as rural insurance,

animal/pest control.

|

|

1

|

COVID-19 has caused undue financial

stress.

|

|

3

|

Leave the system as it is / nothing has

changed to warrant a change in differentials.

|

|

4

|

Limitations around subdivision need to be

considered / align differentials with district planning.

|

|

1

|

Having a larger property does not mean

using more public services.

|

|

1

|

More services/utilities currently paid

for by General Rates should be turned into user-pays/Targeted Rates (e.g.

street lighting).

|

|

1

|

If Residential properties receive a small

gain from the proposal, stop the small gain and use the funds saved to

improve services in rural areas.

|

|

1

|

There is a disparity in rates. Increase

the UAGC.

|

Officers’ information

and comment

General Rates pay for public good

services and facilities across the wider city (e.g. public toilets and the

roading network). It does not matter where the property is or where the service

is, as all properties contribute to these services and all of these services

are available should ratepayers choose to use them or not. General Rates are

not charged based on what is immediately outside the gate of a property.

General Rates recover the costs

for services and facilities that in the Council’s view, the whole

community benefits (e.g. public toilets and the roading network). Therefore,

General rates (including the UAGC) are considered a tax. Legalisation requires

that the General rate is recovered by a value based rate, either land or

capital.

An increase in the number of

Targeted Rates has been considered within the Statement of Proposal through a

proposed Stormwater Rate – this would remove Stormwater from the General

Rate and apply it to properties that either directly or indirectly benefit from

the service.

It is recognised that certain

areas and properties within greater Napier do not receive, or are unable to

receive, targeted services currently provided to urban properties.

Under Schedule 2 of the Local

Government (Rating) Act 2002, nine factors are provided that may be used to

define categories (differentials) of rateable land including: usage/proposed

usage, limitations under a district plan, size, service provided to the land by

a local authority, location, annual/capital/land value of the land.

Excluding utility networks,

properties most negatively impacted by the change (differentials 4, 5 and 6)

make up over 30% of the total land area of Napier City, but less than 7% of

total Separately Used Inhabitable Portions (SUIPs). Defining characteristics of

this area is reduced access to targeted services (such as sewerage) and

generally are further from urban centres.

Officers’

recommendation

A fourth differential is

recommended (Semi-Rural) that provides a stage between Rural and Residential

differentials. Based on the targeted services provided to greater Napier, it is

recommended the fourth differential be classified as follows:

Any property that is not defined

as Commercial & Industrial, or Rural, and would otherwise be defined as

Residential/Other, but is not connected, and cannot reasonably be connected to

the City water and sewerage system is defined as Semi-Rural.

City water is considered

available where the Rating Unit is within 100 metres of such system.

City sewerage is considered

available where the Rating Unit is within 30 metres of such system.

Q.3 – Do you agree with

the way we want to fund Council’s activities? For example the proportion

of rates vs. user pays.

|

Agree

|

23.4%

|

Disagree

|

36.7%

|

Neutral

|

39.8%

|

|

Total Unique Responses

|

128

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

16

|

Activities are services that are

user-specific (e.g. stormwater) should not be funded through General Rates /

increase instance of user-pays in Council services.

|

|

2

|

Allocation of services costs should be

based on household or dwelling size / Land Value does not generate the cost.

|

|

1

|

Certain charges (e.g. library) should be

fixed per property.

|

|

1

|

Different areas do not get different

services.

|

|

2

|

All of Napier should have metered water.

|

|

1

|

All of Napier should have metered water.

|

|

1

|

A discount should be introduced to for

low water users.

|

|

1

|

Less emphasis on user-pays.

|

|

3

|

Uniform Annual General Charge (UAGC)

should be increased to improve equity.

|

|

1

|

Why should I pay for a rubbish bin when I

don’t want one.

|

|

2

|

Increasing rates means paying more money

for no water and sewerage / shouldn’t pay more for services we

don’t receive.

|

|

1

|

Disagree with “toilet pan

tax” as some houses have a large number of toilets and will be unfairly

charged.

|

|

1

|

Increase the General Rate,

|

Officers’ information

and comment

Outside of General Rates,

services funded through Targeted Rates (e.g. water) are only offered on the

basis that they are currently available to certain properties or areas. Please

refer to the District Plan for planned capital works projects.

UAGC benefits properties with a

higher Land Value to the detriment of smaller and lower Land Value properties

(such as flats or residential properties in lower socio-economic areas).

Increasing the fixed charge on properties means that more of the burden is

placed on smaller properties as the cost is fixed. For properties with a higher

Land Value, the fixed charge is proportionately lower and will benefit from

having a lower variable charge (through a reduced rating factor). Modelling has

been performed which demonstrates the impact of increasing the UAGC.

Under Schedule 3 of the Local

Government (Rating) Act 2002, twelve factors may be used to calculate the

liability for targeted rates. The application of certain factors in calculating

Targeted Rates, whilst more accurate, can be cost-prohibitive. A balance needs

to be established between applying rates and administering the system.

Affordability of

services/utilities provided and funded through a Targeted Rate remain so only

because Council employs a policy of charging where the service/utility is

available – the cost is spread across a greater number of properties. If

properties are able to opt-out of a particular service then greater financial

burden rests with the remaining users.

Water and sewerage are funded

through a Targeted Rate. Properties that aren’t able to be connected for

water or sewerage do not pay Targeted Rates for these services and will

continue not to. It is proposed that General Rates, which all properties have

access to, are rebalanced only.

The proposed pan charge is

conceptual only at this stage. Within the proposal it states that “Rating

Units used primarily as a residence for one household will be treated as having

one pan”. This is consistent with note 4 to clause 12 of Schedule 3 of

the Local Government (Rating) Act 2002 that states “…a rating unit

used primarily as a residence for 1 household must not be treated as having

more than 1 water closet or urinal.”

Officers’

recommendation

It is recommended that Council

adopt the proposed activity funding model detailed in the draft Revenue &

Financing Policy.

Rating Policy

Q.1 – Do you agree with

how we propose to assess General and Targeted Rates?

|

Yes

|

11.7

|

No

|

66.2%

|

To some extent

|

22.1%

|

|

Total Unique Responses

|

376

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

2

|

It is unfair.

|

|

1

|

Council does not provide service (e.g.

cleaning drains) near our property. Why should we pay more.

|

|

1

|

Water, sewerage, street maintenance, etc

should be covered only by those who use it.

|

|

1

|

Rural properties do not receive the same

services as urban properties.

|

Officers’ information

and comment

Water and sewerage are funded

through a Targeted Rate. Properties that aren’t able to be connected for

water or sewerage do not pay Targeted Rates for these services and will

continue not to. General Rates pay for public good services and facilities

across the wider city (e.g. public toilets and the roading network). It does

not matter where the property is or where the service is, as all properties

contribute to these services. General Rates are not charged based on what is

immediately outside the gate of a property.

General Rates recover the costs

for services and facilities that in the Council’s view, the whole

community benefits (e.g. public toilets and the roading network). Therefore,

General rates (including the UAGC) are considered a tax. Legalisation requires

that the General rate is recovered by a value based rate, either land or

capital.

Officers’

recommendation

Detailed in questions 2, 3 and 4

(below).

Q.2 – Do you agree with

the proposed General Rate percentage weights for Residential/Other, Commercial

& Industrial, and Rural properties?

|

Agree

|

13.8%

|

Disagree

|

50.0%

|

Neutral

|

36.3%

|

|

Total Unique Responses

|

80

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

4

|

The rates increase is too much / the

proposed increase should be spread over several years.

|

|

6

|

Rates for certain services should only be

charged where they are available.

|

|

5

|

Council does not provide a number of

services to our property / area. Why should we pay more.

|

|

1

|

Hastings rates on the other side of Hill

Road pay less than us.

|

|

2

|

Stormwater should not be charged if

properties have no adjoining stormwater reticulation.

|

|

3

|

Proximity to Council amenities should be

the basis for establishing differentials.

|

|

1

|

Industrial land should have a lower

differential rate than Commercial land.

|

|

1

|

Commercial properties should not

subsidise other property types.

|

|

3

|

No explanation has been provided on how

percentage weights (rates) have been derived. They cannot be arbitrary.

|

|

5

|

Rural rates shouldn’t change as

they have no access to water, sewerage or stormwater / other services.

|

|

1

|

Rural properties have a positive impact

on the city (e.g. attracting native birdlife) and should receive a rates

reductions.

|

|

2

|

Other councils have more differentials.

It is too simplistic to reduce Napier differentials down to three categories

/ my property doesn’t fit into the proposed differentials.

|

|

3

|

Retain the current differentials / retain

our current differential.

|

|

1

|

Land Values are outside of the control of

owners.

|

|

1

|

Owner-occupied properties should not be

penalised. Rented properties should contribute more.

|

Officers’ information

and comment

A targeted Stormwater Rate would

only apply to properties that either directly or indirectly benefit from the

service. General Rates pay for public good services and facilities across the

wider city (e.g. public toilets and the roading network). It does not matter

where the property is or where the service is, as all properties contribute to

these services. General Rates are not charged based on what is immediately

outside the gate of a property.

General Rates recover the costs

for services and facilities that in the Council’s view, the whole

community benefits (e.g. public toilets and the roading network). Therefore,

General rates (including the UAGC) are considered a tax. Legalisation requires

that the General rate is recovered by a value based rate, either land or

capital.

The percentages set for each

differential are based on complex rates modelling performed on rates across the

city. The modelling is based on data from the 2020/21 rating information and

was conducted prior to property revaluation that concluded in November 2020.

Analysis is conducted on a macroeconomic basis with individual properties being

reviewed to assess impact. Due to the range of properties involved, a

“best fit” approach was taken to ensure that affordability was

achieved for the greatest number of properties. As a change in rates for one

type or class of properties impacts all other properties, changes could not be

reviewed in isolation of one another.

Water and sewerage are funded

through a Targeted Rate. Properties that aren’t able to be connected for

water or sewerage do not pay Targeted Rates for these services and will

continue not to. General Rates pay for public good services and facilities

across the wider city (e.g. public toilets and the roading network). It does

not matter where the property is or where the service is, as all properties

contribute to these services. General Rates are not charged based on what is

immediately outside the gate of a property.

Hastings rates for properties

bordering Poraiti and Bay View recognise that those residents very likely

utilise the Napier network for services and amenities (i.e. roads, public

toilets, libraries, etc). Napier residents fund the use of many services and

amenities by non-ratepayers.

The size, geographic features,

demographic mix and mix of property types differ greatly from Council to

Council. The proposal to reduce differentials may not work for some Councils,

but was considered based on the factors noted above specifically for Napier.

Land Value is based on a number

of factors such as size, desirability, cost of upkeep/maintenance, access to

services/amenities, and restrictions on land use and ability to subdivide.

Properties further from urban centres that have fewer attached services are

valued at a lower rate per square metre than urban properties. Valuation per

square metre should not be confused with the absolute value of a property.

Ongoing affordability of property may be impacted by any number of factors (of

which rates are just one element), and is an assessment that lies with each property

owner.

Officers’

recommendation

With reference to the

recommendation for the introduction of a fourth differential (Semi-Rural), the

following percentage weights are recommended:

· Residential/Other

100%

· Commercial

& Industrial 250%

· Semi-Rural 92.5%

· Rural 85%

Although Semi-Rural properties do

not pay for services they do not have access to (e.g. water), a reduced

weighting recognises that these properties may have increased costs in

maintaining their own sewerage and water. Should Semi-Rural properties be

connected to both water and sewerage, the increase in weighting to 100% should

be offset by the savings made in not maintaining individual water and sewerage

services.

Q.3 – Do you agree with

the proposed increase in the City Water Rate from 50% to 70% for Rating Units

that are not connected but within 100m of the system?

|

Agree

|

15.2%

|

Disagree

|

43.0%

|

Neutral

|

41.8%

|

|

Total Unique Responses

|

79

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

8

|

Anyone who is unconnected or does not

want to be connected should not pay.

|

|

1

|

Napier should have metered water like Bay

View.

|

|

1

|

It is too high for no service.

|

|

5

|

Should be user-pays.

|

|

1

|

It does not promote self-sufficiency.

|

|

2

|

Water rates should be reduced due to poor

quality of water.

|

Officers’ information

and comment

Water is funded through a

Targeted Rate. Properties that aren’t able to be connected for water do

not pay Targeted Rates for that service and will continue not to. Affordability

of services/utilities provided and funded through a Targeted Rate remain so

only because Council employs a policy of charging where the service/utility is

available – the cost is spread across a greater number of properties. If

properties are able to opt-out of a particular service then greater financial

burden rests with the remaining users.

There is currently no project to

roll out water metres to all of Napier.

Further reform/change is expected

as part of the Government 3 Waters Programme.

Officers’

recommendation

It is recommended that Council

adopt the proposed increase in the City Water Rate from 50% to 70% for Rating

Units that are not connected but within 100m of the system.

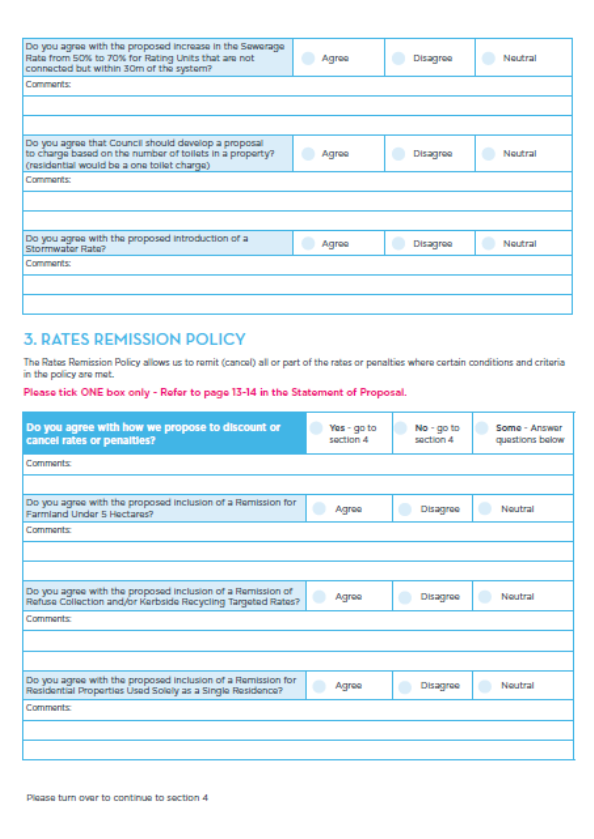

Q.4 - Do you agree with the

proposed increase in the Sewerage Rate from 50% to 70% for Rating Units that

are not connected but within 30m of the system?

|

Agree

|

15.6%

|

Disagree

|

45.5%

|

Neutral

|

39.0%

|

|

Total Unique Responses

|

77

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

5

|

Anyone who is unconnected or does not

want to be connected should not pay.

|

|

3

|

It is too high for no service.

|

|

8

|

Should be user-pays.

|

|

1

|

Should be based on the number of guest

rooms in hotels, motels, guest houses.

|

Officers’ information

and comment

Sewerage is funded through a

Targeted Rate. Properties that aren’t able to be connected for sewerage

do not pay Targeted Rates for that service and will continue not to.

Affordability of services/utilities provided and funded through a Targeted Rate

remain so only because Council employs a policy of charging where the

service/utility is available – the cost is spread across a greater number

of properties. If properties are able to opt-out of a particular service then

greater financial burden rests with the remaining users.

A targeted pan charge is being

considered to replace the current sewerage charge. A pan charge is conceptual

at this stage.

Officers’

recommendation

It is recommended that Council

adopt the proposed increase in the City Water Rate from 50% to 70% for Rating

Units that are not connected but within 30m of the system.

Q.5 – Do you agree that

Council should develop a proposal to charge based on the number of toilets in a

property? (residential would be a one toilet charge)

|

Agree

|

20.5%

|

Disagree

|

48.7%

|

Neutral

|

30.8%

|

|

Total Unique Responses

|

78

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

2

|

B&Bs should be treated like hotels,

not residential for pan charges.

|

|

1

|

Should be a uniform system (not based on

number of toilets).

|

|

2

|

Too complicated to administer and

monitor.

|

|

12

|

Doesn’t account for the number of

people living at an address/number of people using the system.

|

|

2

|

Commercial (e.g. hotels) should pay more.

|

|

3

|

There should be no charge if not

connected to sewerage.

|

|

4

|

Residential should only be counted as one

toilet.

|

|

1

|

Unfair as the number of toilets will be

dictated by building codes.

|

|

3

|

An effluent volumetric should be applied

instead.

|

|

1

|

Should be based on the area of a

property.

|

|

1

|

Would impact resthomes with an increased

charge.

|

|

1

|

Clubs and bars would effectively be

paying twice.

|

Officers’ information

and comment

The proposed pan charge is

conceptual at this stage. Within the proposal it states that “Rating

Units used primarily as a residence for one household will be treated as having

one pan”. This is consistent with note 4 to clause 12 of Schedule 3 of

the Local Government (Rating) Act 2002 that states “…a rating unit

used primarily as a residence for 1 household must not be treated as having

more than 1 water closet or urinal.”

Napier does not currently have

metering in place for all properties and is unable to measure usage on a

volumetric basis.

If implemented, additional

resources will be required at Council to monitor a pan system.

Officers’

recommendation

It is recommended that further

research is conducted to assess viability of a pan charge system and how it may

work.

Q.6 – Do you agree with

the proposed introduction of a Stormwater Rate?

|

Agree

|

30.8%

|

Disagree

|

35.9%

|

Neutral

|

33.3%

|

|

Total Unique Responses

|

78

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

4

|

I manage my own stormwater system.

|

|

10

|

I shouldn’t pay as there is no

stormwater system near my property.

|

|

6

|

Bay View is on shingle and doesn’t

have a stormwater system.

|

|

2

|

Large paved areas produce more stormwater

than large gardens.

|

|

2

|

I don’t understand.

|

|

9

|

Only charge properties connected to the

system / user pays.

|

|

1

|

Capital Value approach is not accurate /

use building size instead.

|

|

1

|

We would expect an upgrade to our system

first.

|

|

1

|

Keep in General Rates.

|

|

1

|

We are also charged by HBRC.

|

|

2

|

NCC don’t look after the public

drains, we do / we should not be charged.

|

Officers’ information

and comment

The proposed stormwater charge

would remove the cost from General Rates (which every property pays) to a

Targeted Rate based on theoretic demand. A targeted Stormwater Rate would only

apply to properties that either directly or indirectly benefit from the

service.

Council is able to base

stormwater on factors such as how much of the property is sealed, paved or

built on. Although a much more accurate approach to take, it would be costly in

terms of time and resources to manage.

Barring those areas that have no

stormwater network (e.g. Rural), it was considered logical to allocate this

cost by Capital Value. Capital Value includes the Land Value plus any

improvements to the property. If the stormwater rate was based on Land Value,

then a bare section and an office building with the same land area could, in

theory, pay the same amount.

When using Capital Value to apply

stormwater costs, properties that are semi-rural or residential, would likely

have more open land area which is porous. Commercial and industrial buildings

in town generally take up a large portion of the property (if not all) and

possibly have concrete or other non-porous surfaces around the buildings. When

it rains, the immediate demand on stormwater would likely come more from that

developed property than the less developed property. There are always

exceptions to the rule, but it is a workable approach in most instances.

Officers’

recommendation

It is recommended that Council

adopt the proposed introduction of a Stormwater Rate.

Rates Remission Policy

Q.1 – Do you agree with

how we propose to discount or cancel rates or penalties?

|

Yes

|

28.1%

|

No

|

35.8%

|

To some extent

|

36.1%

|

|

Total Unique Responses

|

363

|

Summary of submitters’

comments

|

No. of comments

|

Comment/Theme

|

|

0

|

No comments.

|

Officers’ information

and comment

Refer to specific proposals

(below) for information/comments.

Officers’

recommendation

Refer to specific provisions

below for recommendations.

Q.2 – Do you agree with

the proposed inclusion of a Remission for Farmland Under 5 Hectares?

|

Agree

|

38.6%

|

Disagree

|

13.2%

|

Neutral

|

48.2%

|

|

Total Unique Responses

|

114

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

3

|

It doesn’t cover lifestyle properties

that can’t earn a living from the land.

|

|

1

|

How do you establish the amount payable?

How do you establish the value of a property under 5 hectares?

|

|

1

|

It should be rated on land capital.

|

|

2

|

Rural properties have to provide their

own sewerage, water, stormwater, etc. It costs more to run than a residential

property.

|

|

1

|

A number of properties have been

subdivided into 4Ha blocks but are still used for agricultural purposes. They

need this remission.

|

|

1

|

Should be higher if no house on the

property.

|

|

1

|

Needs to be for rural properties, not

specifically farmland.

|

|

4

|

Rural should be redefined as greater than

1 Ha / should be set at a different size.

|

Officers’ information

and comment

The differential percentage and

land size were set based on the characteristics of economically viable

agricultural properties in NZ. It is understood that some smaller properties

may fit within this class – hence the proposed remission.

The remission is intended for properties

that are used for commercial agricultural purposes, but do not meet the 5

hectare threshold. For this reason, lifestyle properties are purposely excluded

as they are held for rural residential purposes.

The amount payable is based on a

factor applied to Land Value. Land Value is determined on a triennial basis. A

differential percentage is applied to the assess General Rate depending on the

differential category the property is classed as.

Targeted Rates are only applied

to specific services that properties receive (such as water or sewerage). Rural

properties that do not receive these services do not pay for these services.

General Rates pay for public good

services and facilities across the wider city (e.g. public toilets and the

roading network). It does not matter where the property is or where the service

is, as all properties contribute to these services. General Rates are not

charged based on what is immediately outside the gate of a property.

General Rates recover the costs

for services and facilities that in the Council’s view, the whole

community benefits (e.g. public toilets and the roading network). Therefore,

General rates (including the UAGC) are considered a tax. Legalisation requires

that the General rate is recovered by a value based rate, either land or

capital.

Officers’

recommendation

It is recommended that Council

adopt the proposed introduction of a Remission for Farmland Under 5 Hectares.

Q.3 – Do you agree with

the proposed inclusion of a Remission of Refuse Collection and/or Kerbside

Recycling Targeted Rates?

|

Agree

|

55.8%

|

Disagree

|

15.0%

|

Neutral

|

29.2%

|

|

Total Unique Responses

|

113

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

3

|

I don’t recycle at curbside so I

shouldn’t get charged for a service I don’t use.

|

|

4

|

We should be charged per pick up. If no

tubs are out then no charge.

|

|

1

|

Agree only if the remission can be

enforced.

|

|

1

|

There should be a different cost for bare

sections, not a remission.

|

|

1

|

The refuse service is still in place

whether it is used or not. A remission would likely be abused and would be

expensive to administer. We should all share in this cost.

|

|

1

|

It is pointless. It shouldn’t

matter whether a bin is half-full or full.

|

|

1

|

I don’t understand.

|

|

1

|

Recycling processes need to improve so

that less waste ends up in landfill.

|

Officers’ information

and comment

Refuse and recycling is funded

through a Targeted Rate. Properties that aren’t able to be serviced for

recycling do not pay Targeted Rates for that service and will continue not to.

Affordability of services/utilities provided and funded through a Targeted Rate

remain so only because Council employs a policy of charging where the

service/utility is available – the cost is spread across a greater number

of properties. If properties are able to opt-out of a particular service then

greater financial burden rests with the remaining users.

There are a number of fixed costs

associated with refuse and recycling. Regardless of whether tubs and bins are

put out or not, the truck will still need to drive past the property. Where

there is potentially a high degree of variance in the number of tubs or bins to

be emptied, the allocation of cost would then fall to only those that use it in

a particular week. If there were a relatively low number of tubs or bins put

out for refuse or recycling in a single week, the cost to those households

would potentially become prohibitive. Costs would be further increased with the

additional administration required to allocate charges on a weekly basis.

Bins and recycling tubs are

barcoded, and can be scanned to see if properties are meeting the requirements

to receive a remission. The proposed remission can be tracked for an individual

property and is easy to administer from a ratings perspective.

Council is actively promoting a

reduction in the generation of rubbish. This remission further encourages that

ongoing goal.

The standard of recycling is a

fine balance. Recycling systems could be improved at a cost to the public. As

the cost of recycling increases, the amount of illegally dumped rubbish

increases (as certain people attempt to avoid those costs). This further

increases the cost of rubbish and recycling services for ratepayers.

Officers’

recommendation

It is recommended that Council

adopt the proposed introduction of a Remission of Refuse Collection and/or

Kerbside Recycling Targeted Rates.

Q.4 – D you agree with

the proposed inclusion of a Remission for Residential Properties Used Solely as

a Single Residence?

|

Agree

|

46.0%

|

Disagree

|

9.7%

|

Neutral

|

44.2%

|

|

Total Unique Responses

|

113

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

3

|

The opposite should happen. The more

people living at a property the higher rates they should pay / the fewer

people the less they should pay.

|

|

1

|

The definition is too limiting to be fair

to all parties.

|

|

1

|

It is no different from a shop charged a

SUIP. If they choose not to rent it out they should not benefit from it.

|

|

3

|

Not enough information provided /

don’t understand.

|

|

1

|

AirBnB’s are a problem with regards

to policing.

|

|

1

|

There should be an allowance for

properties that receive no Council services.

|

Officers’ information

and comment

The proposed remission simplifies

and expands the current remission for multiple SUIPs that are used as a single

residence. Further simplification will erode the meaning of the remission.

At this stage no Councils in NZ

have found an effective way to police AirBnB properties. This is an ongoing

issue.

A number of Council services are

funded through Targeted Rate. Properties that aren’t able to receive

those services do not pay Targeted Rates for those service and will continue

not to. Services and amenities that are available to the public at large are

funded through a number of avenues including General Rates. No properties in

the greater Napier area are excluded from accessing those public services and

amenities.

Officers’

recommendation

It is recommended that Council

adopt the proposed introduction of a Remission for Residential Properties Used

Solely as a Single Residence.

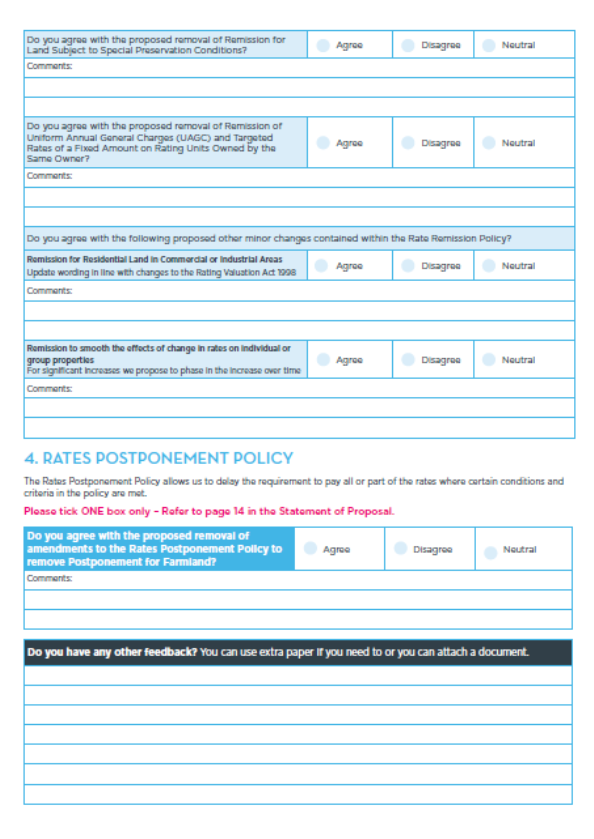

Q.5 – Do you agree with

the proposed removal of Remission for Land Subject to Special Preservation

Conditions?

|

Agree

|

17.3%

|

Disagree

|

16.4%

|

Neutral

|

66.4%

|

|

Total Unique Responses

|

110

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

2

|

Couldn’t find it.

|

|

1

|

I don’t understand.

|

|

2

|

Our property currently uses this

remission / our property could use this remission.

|

|

2

|

If it helps the community it should

remain.

|

|

1

|

Some of these special preservation areas

create an increased fire risk.

|

|

1

|

Properties should be reviewed on a

case-by-case basis.

|

Officers’ information

and comment

This remission is currently

available (removal is a proposal at this stage) and can be found within the

current Rates Remission Policy.

Protection for properties that

currently utilise this remission is found in Schedule 1, Parts 1 and 2 of the

Local Government (Rating) Act 2002. The current remission contains outdated

legal references and is effectively redundant. Further, Council policy cannot

take precedent or countermand legislation.

Officers’

recommendation

It is recommended that Council

adopt the proposed removal of Remission for Land Subject to Special

Preservation Conditions.

Q.6 – Do you agree with

the proposed removal of Remission of Uniform Annual General Charges (UAGC) and

Targeted Rates of a Fixed Amount of Rating Units Owned by the Same Owner?

|

Agree

|

22.9%

|

Disagree

|

15.6%

|

Neutral

|

61.5%

|

|

Total Unique Responses

|

109

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

1

|

Hard to agree when the monetary value is

unknown.

|

|

1

|

We receive no Council services, why

should our rates go up.

|

|

2

|

I don’t understand.

|

|

1

|

One owner, one Rating Unit per title (not

double for converting an existing shed).

|

|

1

|

It depends on the service being provided

to each Rating Unit. If the services being provided to two Rating Units is

the same as one Rating Unit, then the cost should be based on just one Rating

Unit.

|

|

1

|

A remission should be available for clubs

as the members already pay their own rates.

|

|

1

|

Only if the land is rented.

|

|

1

|

This remission is for sub-divided land

and makes the 224 process easier. To remove this, the administration would

increase substantially with sub-dividers only issuing separate titles on

sale.

|

Officers’ information

and comment

It is intended that this

remission is replaced with Remission for Residential Properties Used Solely as

a Single Residence. As it would be a straight swap, the financial impact should

be close to neutral. This type of remission is provided where a single family

group occupies multiple contiguous SUIPs.

With the inclusion of a Remission

for Residential Properties Used Solely as a Single Residence, sub-division and

creation of titles can still occur without penalty. The purchase of the

sub-divided property by a non-family member would trigger removal of the

remission.

For a number of rates, Napier

City Council uses Separately Used or Inhabited Parts of a Rating Unit to

determine the number of services to rate (rather than the number of Rating

Units). This allows for freestanding structures that can be separately occupied

to be appropriately rated.

Details around why rates may

increase for some properties was discussed in the Statement of Proposal. Copies

are still available if requested.

Officers’ recommendation

It is recommended that Council

adopt the proposed removal of Remission of Uniform Annual General Charges

(UAGC) and Targeted Rates of a Fixed Amount of Rating Unites Owned by the Same

Owner.

Q.7 – Remission for

Residential Land in Commercial Industrial Areas: update wording in line with

changes to the Rating Valuation Act 1998

|

Agree

|

31.5%

|

Disagree

|

14.8%

|

Neutral

|

53.7%

|

|

Total Unique Responses

|

108

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

0

|

No comments.

|

Officers’ information

and comment

No comment.

Officers’

recommendation

It is recommended that Council

adopt the proposed updated wording for Remission for Residential Land in

Commercial Industrial Areas in line with changes to the Rating Valuation Act

1998

Q.8 – Remission to smooth

the effect of change in rates on individual or group properties: for

significant increases we propose to phase in the increase over time.

|

Agree

|

44.4%

|

Disagree

|

17.6%

|

Neutral

|

38.0%

|

|

Total Unique Responses

|

108

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

3

|

At 25% more than 3 years is required.

|

|

6

|

Any rates increases (particularly for the

worst impacted areas) should be staggered.

|

|

2

|

We share a water toby but both pay for

full water / limited services but proposed rates increase.

|

|

1

|

I don’t understand.

|

|

2

|

Rates should only increase as services

are introduced.

|

|

5

|

The proposed rates increase is too much /

should not increase.

|

|

1

|

What does “significant” mean?

|

Officers’ information

and comment

Details around why rates may

increase for some properties was discussed in the Statement of Proposal. Copies

are still available if requested.

Issues regarding water tobys are

outside the scope of this proposal.

This remission is intended to

provide Council with a mechanism to stage/stagger rates increases.

Targeted Rates are only applied

to specific services that properties receive (such as water or sewerage). Rural

properties that do not receive these services do not pay for these services.

General Rates pay for public good

services and facilities across the wider city (e.g. public toilets and the

roading network). It does not matter where the property is or where the service

is, as all properties contribute to these services. General Rates are not

charged based on what is immediately outside the gate of a property.

General Rates recover the costs

for services and facilities that in the Council’s view, the whole

community benefits (e.g. public toilets and the roading network). Therefore,

General rates (including the UAGC) are considered a tax. Legalisation requires

that the General rate is recovered by a value based rate, either land or

capital.

It is proposed that

“significant” is quantified as “…25% or more over the

current assessed rates for a single property” to prove clarity on this

definition.

Officers’

recommendation

It is recommended that Council

adopt the proposed updated wording for Remission to smooth the effect of change

in rates on individual or group properties.

Rates Postponement Policy

Q.1 – Do you agree with

the proposed removal of amendments to the Rates Postponement Policy to remove

Postponement for Farmland?

|

Agree

|

22.0%

|

Disagree

|

22.8%

|

Neutral

|

55.2%

|

|

Total Unique Responses

|

346

|

Summary of

submitters’ comments

|

No. of comments

|

Comment/Theme

|

|

1

|

Explanation not provided.

|

|

1

|

It would seem practical at this time.

|

Officers’ information

and comment

The proposal is to remove the

postponement from the Rates Postponement Policy. This postponement is currently

available and further information can be found in the Rates Postponement

Policy.

This postponement is only used by

several properties.

Officers’

recommendation

It is recommended that Council

adopt the proposed amendments to the Rates Postponement Policy by removing

Postponement for Farmland.

1.3 Issues

The role of affordability is challenge

for any local authority as local authorities do not have the ability to set

rates purely on affordability (rates are set on the value of the property).

Councils have no access to, or the ability to, assess household or business

income on which rates could be set

Affordability remains a concern

both for Council and for ratepayers. Some property owners may see a significant

increase as a result of the proposed changes. Staging transition to the new

General Rate differential percentage weights over 3 years would assist property

owners in adjusting to the new rates. Council has provision to do this under

the Rates Remission Policy – remission to smooth the effects of change in

rates on individual or groups of properties.

Property revaluations completed

in late 2020 will impact on the rates liability for each property, and may

increase or decrease the amount originally modelled depending on whether

property land value increases by more or less than the city average of 44.5%.

Until the Council funding requirements

for 2021/22 are set (as part of the 2021-31 Long Term Plan), the rates

liability for each property is yet to be determined.

1.4 Significance

and Engagement

The proposed changes impact all

ratepayers in the Napier City Council catchment.

As detailed in section 1.2

(Background Summary) above, and also in Revenue and Financing Statement of

Proposal Consultation Summary (Attachment C) a relatively high level of

engagement was achieved with the public. Additional engagement was conducted

for ratepayers identified as most negatively impacted through targeted letters

and community meetings in, or near, those most impacted areas.

1.5 Implications

Financial

Rates affordability is a theme that

has come out of the consultation from the community. Council has also

identified areas that may be significantly negatively impacted by the proposal.

Council recognises that providing

affordable and sustainable services to Napier residents

is a key challenge. A number of

respondents have asked for improved services, but these do come at a cost.

Council does note that in comparison

to other councils, Napier’s rates remain in the top third of lowest rates

in New Zealand.

As noted in section 1.3,

individual ratepayers will be further impacted by property revaluations and any

rates increases that arise from the 2021-31 Long Term Plan.

Social &

Policy

The proposed changes impact the

following policies:

· Revenue and

Financing Policy

· Rating

Policy

· Rates

Remission Policy

· Rates

Postponement Policy

Risk

Risks, where possible, have been

mitigated/minimised through following the process required for a Special

Consultative Procedure (Part 6, Local Government Act 2002). Legal review of

documentation produced and relevant policies was also conducted.

Delays, such as the pandemic and

an extension to the consultation period created a risk for delivery of the

2021-31 Long Term Plan. Further delays to the Revenue & Finance Project

will impact on key tasks in the Long Term Plan that need to be completed by

mid-to-late February 2021. This would have a cascading effect should it occur

and is considered a significant risk.

Delaying adoption of the Revenue

& Finance Policy would result in Council being in breach of review

requirements contained within the Revenue & Financing Policy. The policy as

it stands contains references that are outdated and no longer complies with

s.102(1) and s.103(1) of the Local Government Act 2002.

1.6 Options

The options available to Council

are as follows:

a. Consider

the submissions and adopt the officer’s recommendations

b. Consider

the submissions and adopt an amended resolution.

1.7 Development

of Preferred Option

The preferred option has been

developed over many months and is based on modelling of rates data, feedback

from Councillors and officers, and feedback from the public.

A robust process has been undertaken

by Council in accordance with s.101 of the Local Government Act (2002).

1.8 Attachments

a Consultation

Report (and Feedback) (Under Separate Cover) ⇨

b Written

Submissions (Standalone) (Under Separate Cover) ⇨

c Revenue and

Financing Statement of Proposal Consultation Summary ⇩

d Revenue and

Financing Policy (Proposed) ⇩

e Rating Policy

(Proposed) ⇩

f Rates

Remission Policy (Proposed) ⇩

g Rates

Postponement Policy (Proposed) ⇩

|

Extraordinary Meeting of

Council - 9 February 2021 - Attachments

|

Item 1 - Attachment

c

|

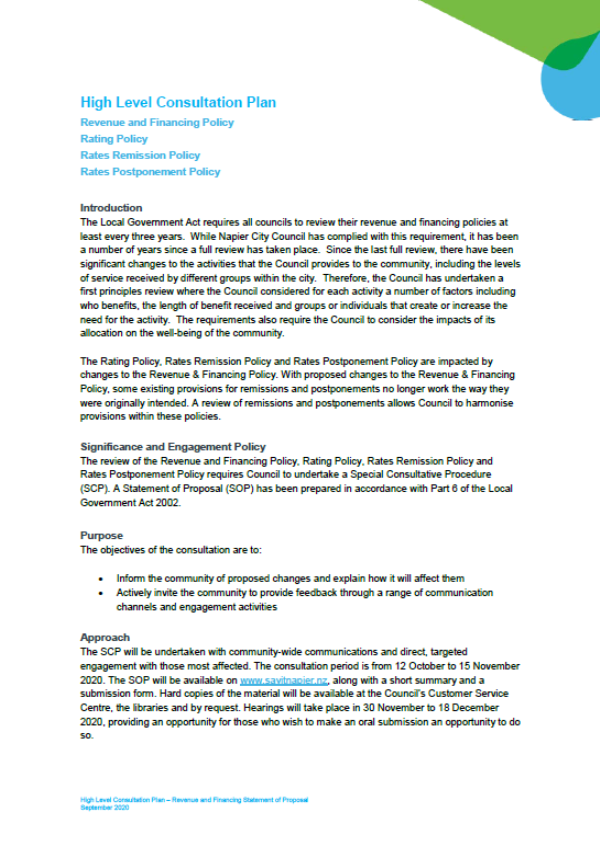

REVENUE AND FINANCING STATEMENT OF PROPOSAL

CONSULTATION SUMMARY

Introduction

The purpose of

the Revenue and Financing Statement of Proposal consultation process was to

seek feedback from the community on the Revenue and Financing, Rating, Rates

Remission and Rates Postponement policies. Consultation began on 12 October

2020 and was initially open until 15 November, but due to strong community

interest, the consultation period was extended to 2 December 2020.

The community

was asked for general feedback on all the policies and for their views on

specific proposed changes including:

· Revenue and Financing

Policy

o How we fund each activity

o Changes to the rating

categories

· Rating Policy

o Changes to General Rate

percentage weights

o Changes to Wastewater

charges

o Removing Stormwater from

General Rates and introducing a Targeted Rate for Stormwater

o Changes to the Rates

Remission and Rates Postponement policies’

Consultation approach

A Special

Consultative Procedure (SCP) was undertaken and a Statement of Proposal (SOP)

was prepared in accordance with Part 6 of the Local Government Act 2002.

There was

community-wide communications and direct, targeted engagement with those most

affected.

Access to the

SOP and opportunity to provide feedback was primarily online, with hard copies provided at

the Customer Services Centre, Libraries, the community meetings and by

request. Assistance and access to the online material was provided at the

Libraries and Customer Service Centre.

Consultation Process

Consultation

was originally open for five weeks from 12 October 2020 to 15 November 2020,

but was then extended to 2 December 2020 due to high community interest.

A range of

engagement and promotional tools were created to support the

consultation.

Engagement

Letters were

sent to all negatively affected properties advising of the consultation, the

proposed impact on the rates, and community meeting dates. Following the

decision to extend the consultation, a letter was sent to all ratepayers.

Six community

meetings were held with a total of 298 attendees:

· Monday 19 October 2020

–War Memorial Centre, 5:30pm – 15 attendees

· Tuesday 20 October 2020

–War Memorial Centre, 11am – 22 attendees

· Tuesday 20 October 2020

– King George’s Hall (Bay View), 6pm – 108 attendees

· Wednesday 21 October

2020 – Taradale Town Hall, 6pm – 100 attendees

· Wednesday 18 November

2020 – McLean Park, 11am – 18 attendees

· Wednesday 18 November

2020 – McLean Park, 6pm – 35 attendees

Mayor Kirsten

Wise and staff provided background and an overview of the proposed policies

before the community were invited to ask questions.

The majority

of the community feedback and questions opposed the policy changes. The main

issues and themes were:

· The changes were

considered unfair to the rural and semi-rural residents as those;

o properties have access to

less services (i.e. footpaths, lighting) within close proximity than other

residential properties; and

o residents already incur

additional infrastructure and service costs (as they are not currently provided

by Council).

· There’s a disconnect

with the District Plan as not all properties categorised as Residential for

rating purposes get the same subdivision rights as Residential properties in

the District Plan.

· Rates are increasing, but

services are not.

· Questioned the reasons for

making the changes.

· Questioned the timing of

changes due to the December 2020 property revaluations.

Promotion

Content was

developed in such a way that it could be used across all digital platforms with

supporting print advertising using the same look and feel. The say it! branding

was used as a theme to encourage people to provide feedback on the say it!

website. The aim of all of the material was to be clear and accessible.

Frequently Asked Questions were uploaded to the say it! page and updated as

community feedback was received. Key messages were also adapted at the request

of elected members as the campaign progressed.

Revenue and

Financing Statement of Proposal consultation was promoted widely using the

following tools:

· Media – advisories

and releases

· Advertising – radio,

digital and newspaper

· Direct distribution

– email and letter

· Council channels –

website, digiscreen, email signature, regular publications and social media

· Community meetings

See Appendix

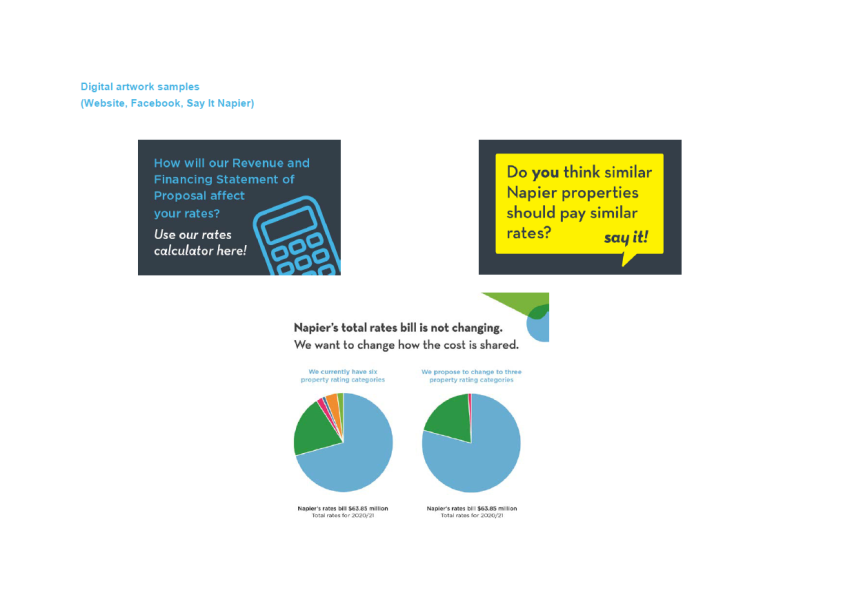

3 for samples of promotional material.

Response

Overall, 540

submissions were received. 474 submissions were submitted online and 66 were

provided in hardcopy form. Some duplicate submissions were received (same

person or address) which were aggregated into a single submission per

household; this results in a total 427 unique responses per rating unit. 64

submitters requested to support their submission in person (oral submission) at

the Hearings.

Digital / Social Media

Digital

advertising

442,197

impressions served for this campaign which is the number of times the digital

advertising was displayed to Napier residents; this is high. This generated

2,457 clicks through to the consultation web page.

The average

cost per click was $0.52 and there was a click through rate of .56%, which is

average.

Social

media

There were four adverts

across Facebook and Instagram, reaching 22,889 residents and generating 782

clicks through to the consultation web page.

Along with the four

adverts, the consultation was organically posted eight times, reaching 47,874

residents and generating 2,924 engagements; this includes reactions, comments

and clicks.

Website

– sayitnapier.nz

Traffic to the

consultation saw five significant spikes throughout the campaign. These cannot

be directly linked to any specific community session or social media posts.